- California-based venture capital firm Acre Venture Partners has closed a $140 million fund (Fund III) to invest in agrifoodtech startups.

- Fund III will invest from pre-seed stage up to series B, with money reserved for follow on investments.

- To date, Fund III has invested in six startups: Bonsai Robotics and farm-ng (ag robotics), Highlight (in-home product testing platform), People Science (clinical research platform), Arado (agribusiness marketplace), and Switch Bioworks (ag biologicals/biofertilizer).

- Lynda Deakin (from design & innovation co IDEO) and Chef David Chang have taken on operating partner roles.

‘We’re a climate fund using food and agriculture as our mode of action’

Fund III is backed by new and returning investors, “with one existing investor becoming much larger,” managing partner Lucas Mann tells AgFunderNews.

“It’s clear that this is a difficult moment to raise money for both companies and funds, but we’re almost 10 years old, and so I think that has given us the opportunity to understand mini-cycles or patterns and not make the mistakes that new entrants to the space may make. I’m not saying we haven’t made mistakes in the past, but we’ve learned from them.”

As for areas of focus, he says, Acre Venture Partners is “a climate fund using food and agriculture as our mode of action. For Fund III, we’re not taking anything off the table; we’re only putting new areas on. So quite a bit of our pipeline has moved into the more traditional climate space. And that means that investors we work with might see things that are maybe outside of food and ag, but we’re willing to play with that to understand [their potential impact] on agricultural systems.”

One area he is “very excited about” is “large data systems, and the capabilities of both machine learning and artificial intelligence on those data systems to inform incumbent companies,” says Mann.

“So on the food side, [Acre portco] Highlight is a SaaS company that does consumer testing for large CPG companies. We’re working with them to understand how consumers look at climate so they can use that to help big companies integrate climate smart foods and ag into their portfolios.”

On the ag side, he says, “We’ve seen companies like [gene editing startup and Acre portco] Inari really become reliant on machine learning.”

Ag robotics now within the remit

As a fund Acre Venture Partners has “always taken the stance that there are certain technologies that we don’t want to invest in because of where we sit in the capital stack or their development over time or whatever it may be,” says Mann, who has invested in everything from ag biologicals to firms developing probiotics for infants. “But we’re also willing to change our thesis.”

One example of this is ag robotics, an area which the firm has historically avoided but is now looking at closely through investments in firms such as Bonsai Robotics and farm-ng, he says.

“Product capability in this space has caught up to what we know about the cost curve. Both companies [Bonsai and fam-ng] use AI SLAM [artificial intelligence simultaneous location and mapping]. That technology, which has come so far in recent years, has allowed an opportunity for the retrofitting of existing machines to make them autonomous, so you don’t have to use all this capital to build a machine.

“But we’ve been patient in this space, as we have been on alternative protein [Acre only has one investment in this space, fungi-fueled startup Meati]. We didn’t get involved in alternative protein in the first or even the second wave.”

Meanwhile, Acre has not invested in cultivated meat, says Mann, although he hasn’t written it off. “I think eventually companies will figure out [how to scale the tech cost-effectively]. It’ll get faster, less expensive and more delightful, but we aren’t going to participate in those early innings.”

Navigating the funding winter

As for the evolving funding environment, he says, “It’s time to focus on kinetic [as opposed to potential] energy as quickly as possible, especially as relates to attracting high quality investors in the follow on rounds. That has become something startups really need to look at. How are they going to appeal to later stage investors? We now have 10 years of experience with a whole range of follow-on investors.”

On exits, he says, “I think it’s fair to say that in agriculture, there have been relatively few exits. I think a lot of that relates to the nature of the businesses and how much time it takes to get a product to market. Inari is a great example of that, but that doesn’t mean we’re not excited about the opportunity.”

In general, he says, “there have been more exits on the food side, certainly in the consumer space, although we don’t take a lot of bets there [one exception is gut health brand Supergut].

“The macro environment will obviously have an impact on what the exits look like, and we’re not in control of that. Some are better candidates for an IPO; some are better candidates for M&A.”

‘We’ve been able to find some really high margin businesses’

But is agrifoodtech a good fit for venture capital, which is not the most patient kind of money? The ‘tech’ part notwithstanding, food isn’t software, startups are dealing with unpredictable biological systems, they may need need costly physical infrastructure and distribution systems, and they’re operating in a complex and sometimes frustrating regulatory environment, acknowledges Mann.

“I think it’s always been hard, but we’ve been successful because we’ve had a real perspective on what qualifies as a venture investment and what doesn’t. And you have to really understand the system in order to do so, which is why new entrants struggle and why some of the generalists have left the sector.

“But we’ve been able to find some really high margin businesses. For example [Saas startup] Source, which is one of our companies, uses artificial intelligence to control greenhouses, and it is doing incredibly well. [In-home product testing platform] Highlight is a software business and People Science is a true SaaS business, so I think you can find those opportunities if you’re patient and if you understand the [needs of] incumbents in agriculture.”

‘The pain will continue for a while’

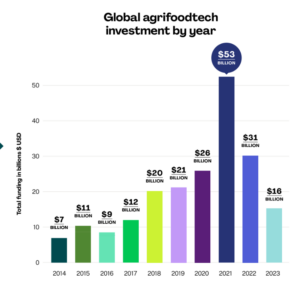

Despite the continued decline in agrifoodtech investment (down 49.2% in 2023 vs 2022 according to AgFunder data), says Mann, “I’m still super bullish about this space and the quality and quantity [of dealflow] continues to increase. I think a lot of the pain we’ve seen in these last months is the result of the mispricing of deals during that 2021 window [where valuations went through the roof].

“I hear people say the sky is falling in and funding is down and yes, I think the pain will continue for a while as deals that aren’t performing are price corrected. As for the generalists, many of them will steer clear until opportunities reemerge. The onus is on the sector to prove that companies are of value and that will happen in the coming years. But this is a time to navigate carefully.”

To boost its team, Acre Venture Partners has brought in former IDEO partner Lynda Deakin and Chef David Chang as operating partners, says Mann.

“Lynda is not a typical hire for a venture fund of our size. She is spectacular, she embeds inside companies and does all the things that IDEO does so she’s an incredible asset. And this year we have her full time.

“David Chang is best-known as a chef at [he founded high-end restaurant chain Momofuku], but he also has a very successful CPG brand doing big numbers, so he’s a really great asset for our founders.”

“Since joining Acre, I have collaborated closely with our portfolio companies, helping them develop innovative products, establishing and honing their strategic brand foundations, gathering deep consumer and customer insights, and sharpening their sales and marketing strategies.” Lynda Deakin, operating partner, Acre Venture Partners