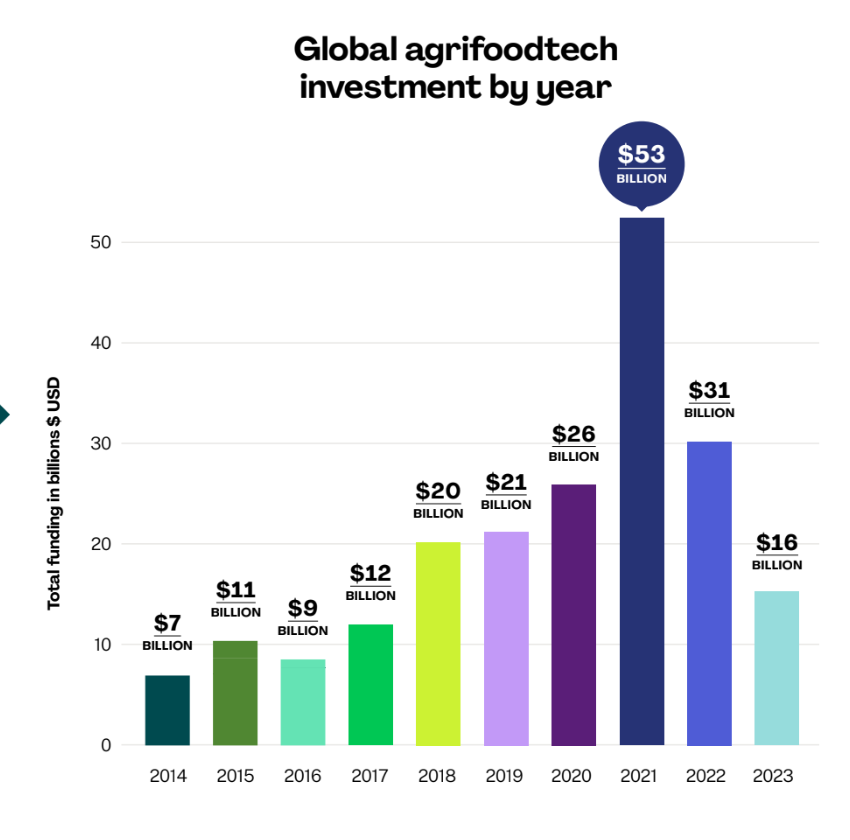

There’s no way to sugarcoat this: investment in agrifoodtech startups is at its lowest point in six years. Not only is it lower than those pre/early-Covid, crazy-VC-inflated-valuations years between 2018 and 2021 but it also declined as an overall portion of the global venture capital landscape.

In 2023, agrifoodtech represented just 5.5% of all venture capital sector dollars, down from 6.7% in 2022 and 7.6% in 2021, according to our just-released AgFunder AgriFoodTech Investment Report 2024.

While some deals have been down rounds, dramatically shrinking startup valuations, deal averages and medians, there’s also been a halt to dealmaking in many instances at the early stages.

This is in part down to some founders’ refusals to lower their company valuation expectations, but in some cases, the correction has gone too far. Beleaguered plant-based company Beyond Meat has been trading on the Nasdaq stock exchange at a valuation of just 1x revenues; that’s far below the 3x-5x multiples you typically see with an acquisition or among publicly-listed CPG companies, let alone the 8-10x you might expect to see for tech companies.

Given that VCs typically use the revenues and earnings multiples of publicly listed companies to model out an “if everything goes right” scenario when pricing early-stage rounds, “now, even a $15 million valuation for a well-performing Seed/Series A startup can look rich,” Rob Leclerc, our founding partner, wrote to investors recently. “Some areas like foodtech and alternative protein are seeing almost no investor interest no matter how attractive the opportunity.”

Of course, we know this category and a few others got out of control valuation-wise but that was not unique to those categories and was certainly the case elsewhere in tech.

Furthermore, those were the main categories drawing in generalist investors to our industry, investors who are now fleeing the industry altogether in the wake of downrounds and failures. We’re also seeing some of the first agrifoodtech venture capital firms disappear as they fail to raise follow-on funds.

2024… a painful year for many, but a good time to invest?

This might read as depressing news, and it should. You’ll no doubt find more closure stories on AgFunderNews in the coming months; 2024 is going to be a painful year for many, especially the more mature agrifoodtech companies. But it will also be an incredible year to invest in new companies that have been forced to rethink their business models and take a leaner approach; that’s healthy for the market and for valuations.

For our parent company AgFunder, it’s been a promising year culminating in the closing of our largest fund to date, oversubscribed, and with more investor interest than we’ve seen before.

But, that agrifoodtech is just 5.5% of global venture capital investment is at odds with food and agriculture’s contribution to the global economy and livelihoods; the industries contribute at least 15% to global GDP, hire over half the workforce, and contribute to one-third of greenhouse gas emissions.

Underinvestment is somewhat understandable given the relative lack of decent venture capital exits, which the industry desperately needs in 2024.

What do you think? Has the correction gone too far? Why aren’t more investors coming into agri-food? Email me: [email protected]

![]()

Sign up for our weekly newsletter.