Editor’s Note: AgFunder is AFN’s parent company.

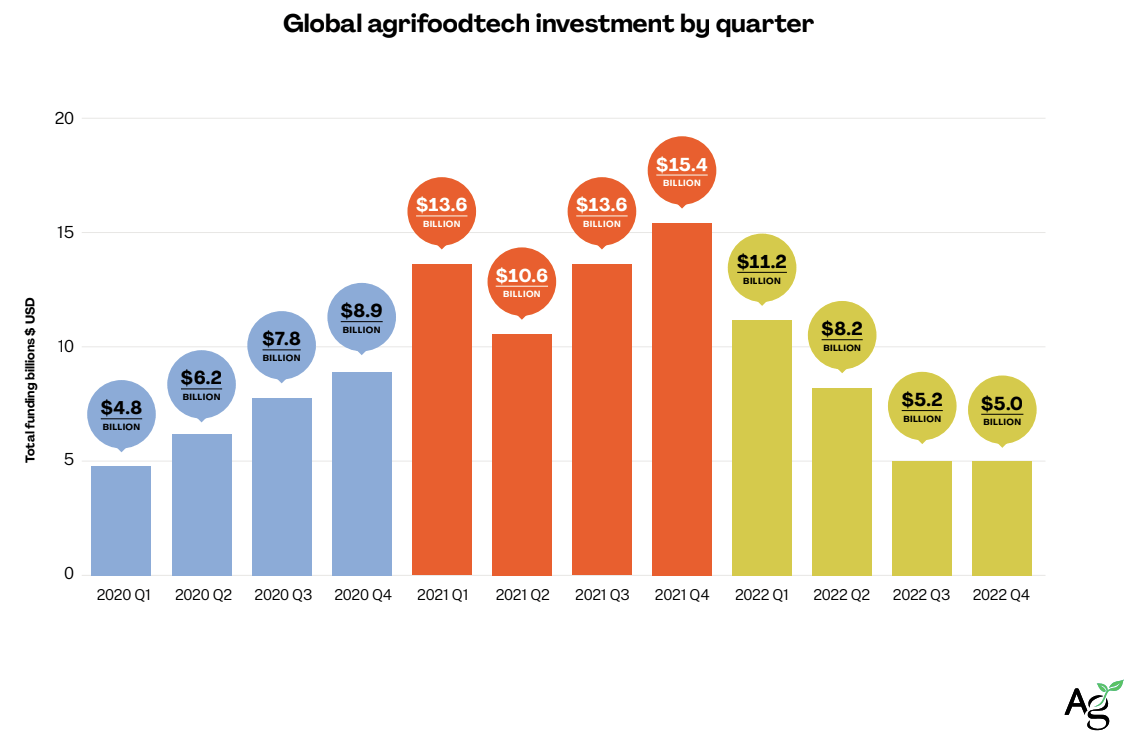

There’s no denying the second half of 2022 was terrible for venture capital, and agrifoodtech was no exception.

Funding to foodtech and agtech (agrifoodtech) startups reached $29.6 billion in 2022, down 44% year-over-year (YoY), according to a new report from food, agriculture, and climate-tech venture capital firm AgFunder, in collaboration with global ecosystem partner Temasek.

But the sector posted gains in climate tech categories such as indoor agriculture, bioenergy & biomaterials and precision agriculture.

Cheap money and increasingly outlandish tech valuations drove 2021’s record-breaking $51.7 billion in agrifoodtech funding. Then, in the wake of war, inflation, and continued supply chain disruptions, the market came crashing down in

2022.

A glance at the below chart shows just how wild the ride has been over the past two years. But many of the world’s current macro challenges – from soaring inflation to food insecurity to labor shortages – are driving more interest in agrifoodtech as a solution, particularly in its climate-tech-related categories.

Agrifoodtech as climate tech

In a new feature for this year’s report, a survey of agrifoodtech VC investors revealed that while they don’t expect valuations to improve much in 2023, they were buoyed that the sector is also increasingly recognized in the climate tech conversation and it showed in the data.

Four categories related to climate tech and efficiency experienced an increase in funding:

- Bioenergy & Biomaterials funding increased to $2.3bn, up 15% from 2021. This highlights the growing momentum for novel alternatives to plastics and animal-based materials as well as clean energy sources.

- Ag Biotech funding increased to $2.7bn versus $2.5bn in 2021 and was almost flat by number of deals, down just six to 216 (meaning it was not outlier driven).

- Novel Farming Systems funding increased 21% YoY to $2.85bn with the number of deals remaining flat year-over-year with significant deals across both insect and crop-based systems.

- Farm Management Software, Sensing & IoT funding increased $430m to $1.7 billion, albeit with a decline in deal activity, hinting at some large deals.

Downstream, consumer-facing categories did not fare so well. Funding to eGrocery declined 73% year-over-year to $5.1 billion, Cloud Retail Infrastructure dropped 68% to $1.5 billion, and Innovative Food, which includes alternative protein, raised $3. billion, nearly 40% less than in 2021.

No mega deals

One of the major drivers for the big declines downstream was the lack of mega deals.

There has been at least one deal of over $1 billion every year since 2016, except in 2020. In 2021 there were four — one of which was a whopping $3 billion round for eGrocery startup Furong Xingsheng as Chinese investors backed delivery startups with gusto as they tried to reach — and capitalize on — continually locked down consumers. The almost overnight drop in funding to food delivery startups in China contributed to a massive $5.5 billion drop in investment in China agrifoodtech in 2022 versus 2021.

By comparison, the biggest deal in 2022 was a $768 million Series E for Turkey’s rapid food delivery giant Getir, and the second was a $500 million late-stage deal for now-publicly listed carbon capture company LanzaTech.

The decline in the number of deals closed was, therefore, less pronounced than the dollar drop; some 2,797 deals closed in 2022, down 22% from the 3,445 we recorded in 2021. Furthermore, we generally expect the number of deals in 2022 to increase as more deals come to light.

A few other key insights from the report include:

- Farm tech investment declined just 6% year-over-year, with startups raising $10.2bn across 848 deals. Of particular note was China’s increasing focus on farmtech innovations.

- Funding to African agrifoodtech startups increased 22% to over $600m. Some large deals helped inflate this but that’s a positive trend in itself.

- Funding declined more than 35% to the following categories: meal delivery, eGrocery, alternative protein, cloud retail, and midstream technologies.

This report was produced in collaboration with global ecosystem partner Temasek and partners Foodbytes and AgriFutures Australia. It includes spotlights on startups eFishery, Loam Bio, Umaro, Propagate, Eion, CommonGround, Tevel, Klim and Unreal Milk.

Download the full, FREE 90-page report here to get the full story.

You can also receive our weekly data snapshot feature articles, which offer more granular insights from our database, by signing up for the newsletter here.