It may come as a surprise to you that the world’s agriculture industry – the multi-trillion dollar industry that feeds us – operates on a very informal basis in most of the world. From large-scale growers in the Global North to smallholder subsistence farmers in the Global South, a huge amount of business is done face-to-face with advisors and retailers who are often personal connections.

The dawn of the internet, which rapidly pushed consumer commerce online, had little effect on the industry in the early years, with poor rural connectivity, financing issues, and trust concerns a few of many contributing factors.

This has left many farmers globally lacking access to markets that could benefit their businesses and livelihoods, including high-quality inputs and seeds, a wide range of buyers for their produce, and finance to help them weather the highly cyclical nature of the industry, which can often mean just one or two paydays per year after each crop is harvested.

“Farmers bear a lot of the upfront risk in agriculture, meaning they can potentially lose a season’s worth of income due to diseases, weather or pests,” says Ryan Lee, associate at AgFunder and part of the selection committee for AgFunder’s GROW accelerator program. “The inconsistency in payment periods makes it very hard for farmers to accurately manage their finances.” [Disclosure: AgFunder is AFN’s parent company.]

But as smartphones have proliferated and technological advancements have enabled more transparency around agricultural products and pricing, farmers are gaining more trust in online tools as a means to do business.

In fact, investment in startups in what AgFunder calls the Agribusiness Marketplaces & Fintech category has steadily increased in recent years reaching a peak of $1.8 billion in 2021, with a modest 5% dip to $1.7 billion in 2022 (versus 30%+ in most venture capital sectors.)

These startups all aim to bring farmers online, providing them with access to better inputs at better costs, as well as better markets for their produce at better prices, and better access to finance.

There is a wealth of approaches being taken, often with elements specific to the target farmer base and location. At AgFunder, one of our best-performing investments is in Dehaat, an Indian online marketplace giving Indian farmers access to better inputs and markets.

AgFunder has recently invested in three more companies in this category via its Singapore-based accelerator program GROW. From over 600 applications, 10 companies were chosen to join the fourth cohort including the following three Ag Marketplaces & Fintech companies working on farmer financial inclusion.

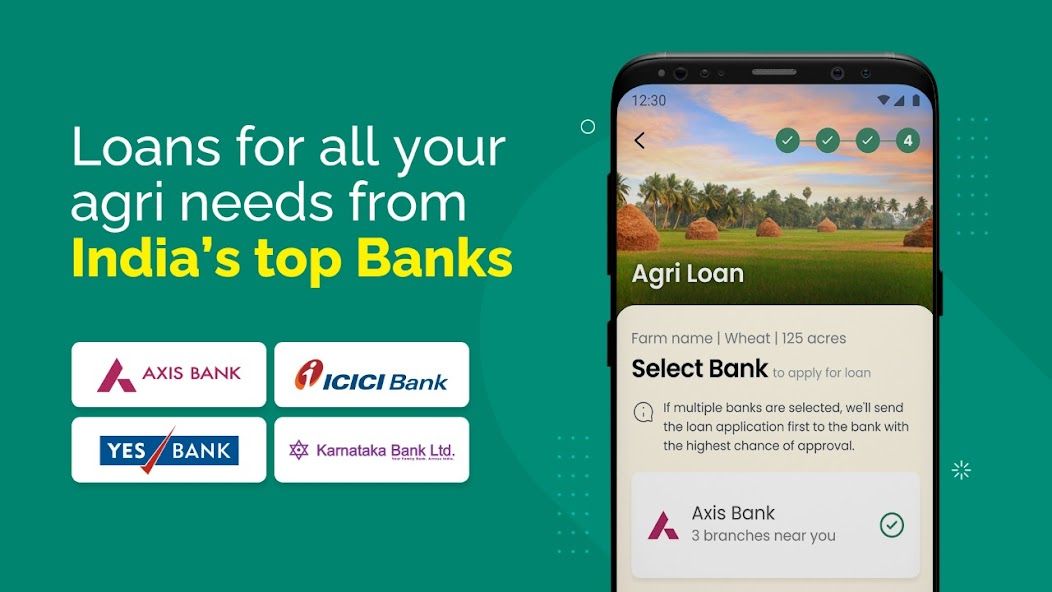

- AgriFi from India is a digital credit platform that helps Indian farmers get access to loans, buy inputs and seeds and have a daily record of their transactions. It also helps banks reduce their lending risk.

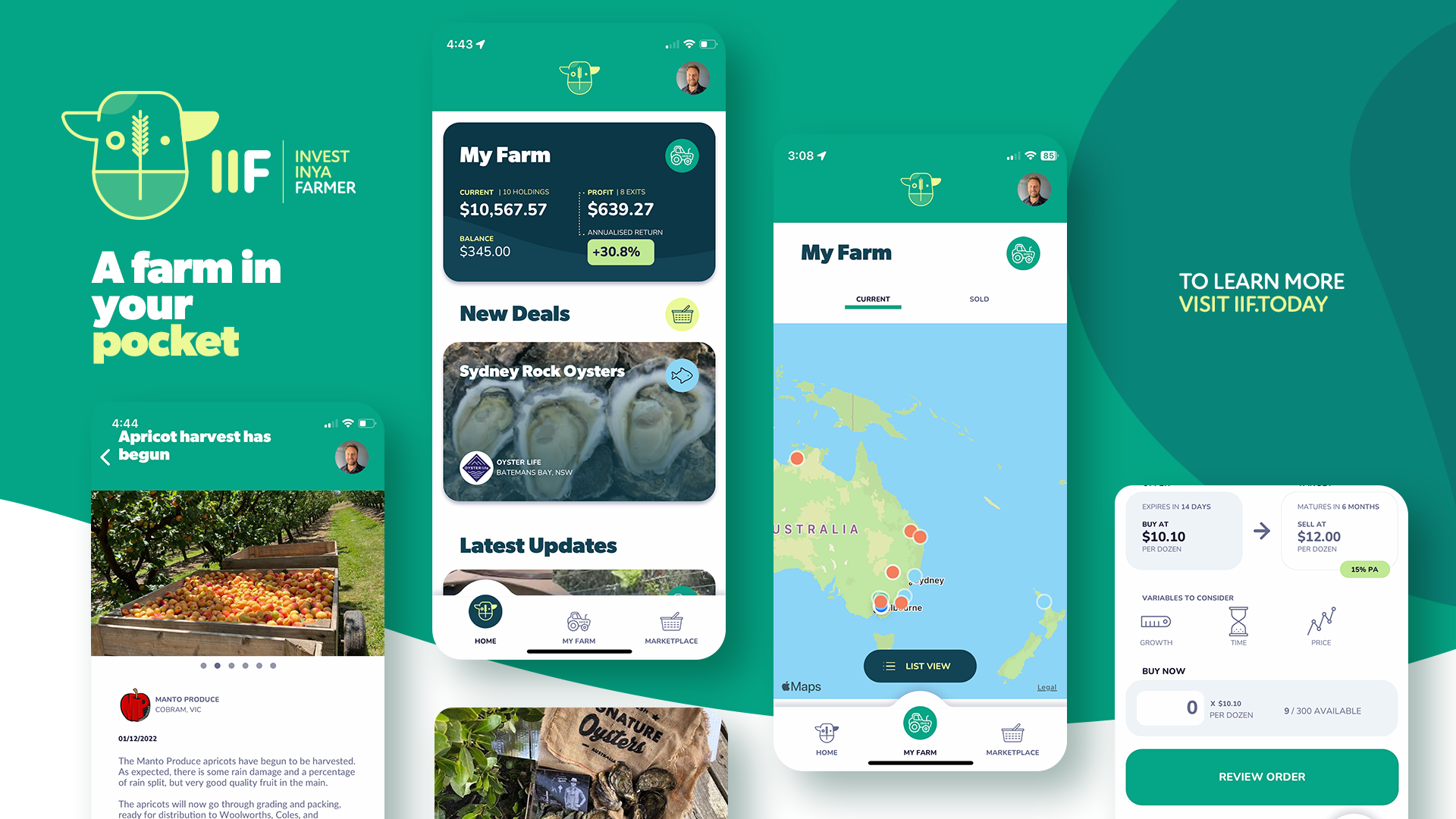

- Invest Inya Farmer (IIF) from Australia is providing a different type of finance access to farmers with its investment platform that enables everyday folks to invest in agriculture without owning a farm.

- DHF Platforms, from Vietnam, partners with smallholder farmers to transform fresh produce into value-added goods, getting products to market six times faster and fresher than alternatives at half the price. They further provide transparency and traceability for buyers all through integrating tech solutions into their supply chain.

Helping banks score Indian farmers for formal loans

With limited paydays each year, debt is a key tool for farmers to run their businesses and make ends meet before harvest. But for 80% of India’s farmers, who typically run smallholdings of just a few acres each, only informal loans and credit are available to them as banks deem them too risky to engage with. These informal arrangements often come in the provision of seeds and other inputs on credit by agriculture retailers, or the traders who later purchase their produce. But this type of credit typically comes with a very high interest rate of as much as 50%, according to Abhilash Thirupathy, founder and CEO of AgriFi.

“Because of this farmers are forced to buy sub-standard seeds and inputs and also sell their produce and sub optimal prices,” he tells AgFunderNews.

“By working closely with banks for 18 months, and conducting pilots across the farmer value chain, we understood banks lack the tools to underwrite those farmers who deal in cash and that comprises more than 85% of all farmers in India,” he adds.

What the banks needed – and were open to – was a unique credit scoring system for the farming ecosystem. AgriFi started to build that 12 months ago starting off with three basic parameters and then enhancing it to about 10 unique parameters to make the score more relevant and contextualized, says Thirupathy who has already engaged with three of the largest private sector lenders in India and has facilitated numerous loans across the value chain and the country.

“The impact of of AgriFi score is that a farmer who does not have a credit score is able to apply and get loan at 10% interest from a formal institution such as a bank. This helps them build a credit score and in the future, apply for larger loans and access to other products such as farm equipment loans, farm development loans and thereby build better financial outcomes for their families.”

The company is in the process of a nationwide rollout and recently updated its scoring engine with the expectation of a 10% to 15% growth rate month-over-month.

But scaling is not without its challenges: “Working with banks in a highly regulated space means that change is slow and bound to be affected by policy changes. This is one of the biggest challenges in this space. The next challenge is loan waivers [whereby a farmer’s debt is written off by the government], which is a political subject that ends up messing farmer credit scores [and has been described as a double edged sword]. The last challenge is climate risk, which affects yield and consequently the ability of a farmer to repay loans.

What if you could invest in farm production rather than farmland?

Nathan MacPhee, founder and CEO of IIF, is taking a very different approach to getting more cash into farmers’ pockets, after a 20-year career in financial services in Australia. After moving to the country about five years ago with his wife who comes from a farming background, MacPhee says he wanted to become a farmer but immediately faced the challenge of not owning a farm. “And unless I won the lotto, I probably never would,” he tells AgFunderNews.

“It got me thinking: What if you could invest in farm production rather than farmland? Buy the cow but not the farm? And what if that capital – sourced directly from consumers – could help farmers transform their business in ways that wouldn’t otherwise be possible?”

Fast forward a few years and IIF is now partnering with farmers within livestock (cattle, sheep, bees, chickens), aquaculture (oysters), horticulture (melons, pineapples, ginger, vegetables, wine grapes, apricots), and cropping (wheat, oats, rice), and taking investments of as little as A$100 to A$100,000.

“There are similarities with crowdfunding, but we are more like crowd farming or digital share farming,” adds MacPhee. “Crowdfunding usually involves investments in shares in a company, which have low liquidity. We don’t invest in the farm or the company.”

“Instead, we own the cow in the paddock, the oysters in the river, fruit growing on the tree or wheat growing in the field. We own it, the farmer grows it, harvests, and sells it. If it sells for a profit we pay the farmer extra. If it sells for less than we paid, the investor wears the loss.

This provides risk-free capital to farmers, sourced from consumers and builds a mutually rewarding bond.”

So far, IIF’s expansion has primarily relied upon word of mouth or warm introductions to farmers. The reception from farmers has been very positive and most encouraging has been the diversity of farmers, both in industry and size, MacPhee tells AgFunderNews.

“In a short space of time, we have now worked with farmers in every state in Australia and NZ.”

How IIF works

Here are some examples from MacPhee.

Livestock: “We buy a cow for $700 (current value) but we may actually pay $1,000 to cover the $300 estimated costs to feed and care for the animal for a year. So the farmer get $1000 now and if the heavier cow sells for $1300 in a year, we split the $300 profit. The farmer gets paid a year ahead and still gets upside.”

Oysters: “We might buy a dozen oysters in winter for $10 per dozen and in summer they are in better condition and with higher demand they may sell for $12. That $2 profit is split and the investor would make $0.80. Doesn’t sound like much but that would be an 8% return in 6 months or 16% annualised. Farmer is happy as they get money early when their cashflow is low.”

Fruit: “We don’t own the tree. We own the fruit being grown in the season. We pay the costs (pruning, fertilising, picking, packing etc) and our return is the value of the actual fruit harvested and sold. This means the farmer doesn’t carry production risk on our fruit and can still make a good profit.”

Crops: “We would pay the input costs, plus a margin at the time it is sown. For instance, if it costs $500 per hectare to grow a wheat crop and the estimated yield is 2 tonnes per hectare and $500 per tonne, we may pay the farmer $700 upfront. They have covered their costs and if it yields $1000, then we split the $300 profit. If the crop spoils then the investor loses $700. The farmer can’t lose.”

Promoting farmer financial inclusion with value-added foods

DHF Platforms is improving farmer inclusion with its integrated farm-to-fork supply chain for value-added fresh produce from Vietnam. DHF is the first company to produce value-added ready-to-eat salads in Vietnam and it has built the business by working with smallholder farmers to grow novel crop varieties, providing detailed traceability for its overseas customers in other Asian countries.

“Vietnam is one of the largest horticulture/agriculture growers in Southeast Asia,” says Angela Tay, senior associate at AgFunder and one of the selection committee for the GROW accelerator. “We believe that the economics of buying higher value vegetables from Vietnam to sell to developed regional markets like Singapore and Hong Kong makes more sense than them importing from further markets like Australia, Europe, and the US; the carbon footprint is reduced, and the produce is cheaper and fresher.”

To ensure a sufficient supply for a customer base made up of B2B supermarkets, convenience stores, and HORECA customers, DHF contracts with a growing number of smallholder farmers and supports them in the transition to growing new, higher value crop varieties, which bring in higher incomes on less than 30-day payment terms, securing their cash flow.

“There is an extensive educational challenge associated with cultivating new crops like our baby leaf salad because smallholder farmers tend to have limited experience with novel seed variants, ” says Huyen Tran, founder and CEO of DHF.

In response and through its contract farming model, DHF provides “essential resources such as high-quality inputs (ie. seeds and nurseries), and guidance and advisory services for Good Agricultural Practices (GAP), and we will be expanding our efforts via demonstration farms,” she tells AgFunderNews.

“Moreover, we are actively establishing cooperatives and engaging in partnerships with NGOs and corporates to deliver training and oversight.”

To date, DHF’s technology platform has focused on operations and logistics, but the company is “about to release an update for farmers to input their farm diaries directly onto the platform for enhanced traceability and to capture valuable farm supply chain data in real-time” says Tran.

“In regard to our B2B customers, our interaction has yielded positive results. This is attributed to the uniqueness of our offering, which provides exceptional quality while significantly undercutting the costs associated with imports from far-off places.”