Editor’s note: Seana Day and Brita Rosenheim are partners at Culterra Capital and venture partners at Better Food Ventures. Based in the US, they each have 20-plus years of investment, M&A, and strategy experience in agrifoodtech. Their analyses on the sector are regularly used by participants in the space to understand the continuously evolving landscape.

The views expressed in this guest article are the authors’ own and do not necessarily represent those of AFN.

Agrifoodtech is undoubtedly having a moment in the sun. According to AgFunder and AFN, $30.5 billion of fresh investment capital flowed into the sector in 2020, representing a 35% increase over 2019.

Yet the bulk of value creation and investment to date have been consolidated at the end-points of food and ag – either within supply (eg, at the farm) or demand (consumer, retail, restaurants, etc.)

Now, with the perfect storm of Covid-related disruptions, intensifying food safety regulations, and a proliferation of new business models — such as direct-to-consumer (D2C) — we are reaching a unique inflection point to create new tech-driven market value within the food supply chain.

Market winds favor the bold (and the committed)

As discussed in our previous article outlining our food supply chain predictions for 2021, these recent supply chain dislocations have spurred an unprecedented push to update a sector that hasn’t been significantly modernized since the last century – yet one that represents around 15% of global GDP.

With an ageing food supply chain infrastructure, dated record keeping and reporting, and historical tech investment of less than 1.5% of revenue according to LocalGlobe, woeful underinvestment is amplifying risk and disruption.

It’s clear that stakeholders can no longer put off investment into supply chain tech. But where do they start?

Whether for internal digital transformation projects or external private capital investors, it’s challenging to align the timing of investments and the maturity of technologies or platforms that are potential investment targets. Often, it’s a choice between tech that is market-proven or at commercial scale, versus tech which is long on promise, but still short on results.

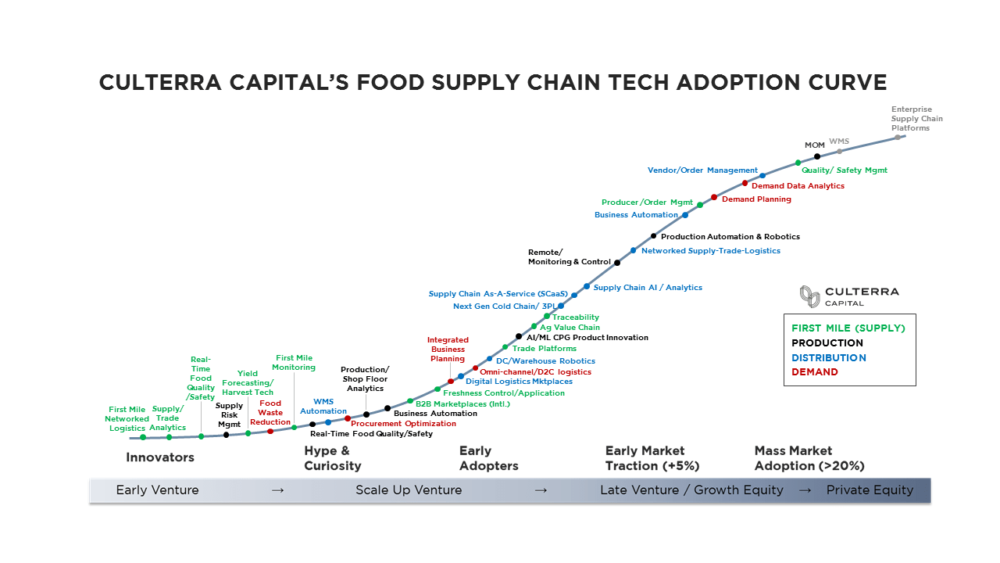

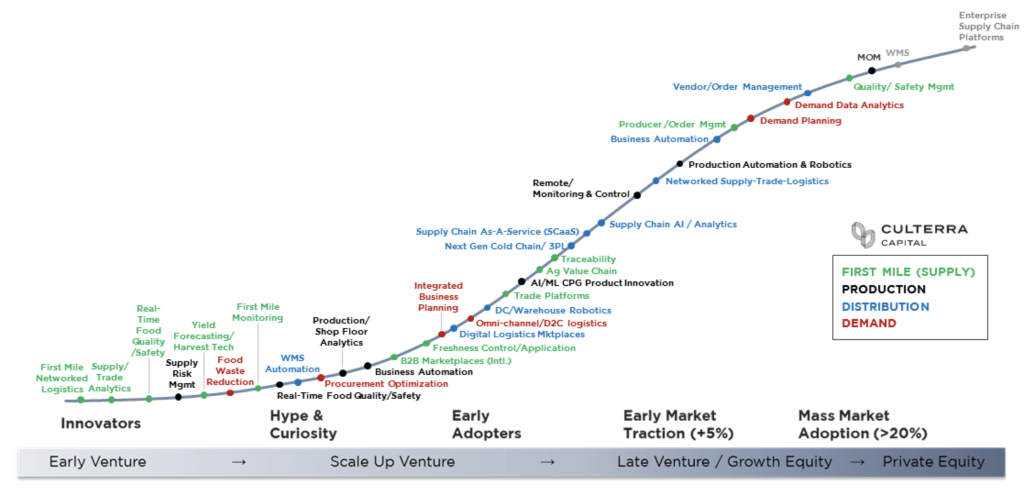

In sharing our perspective through the Food Supply Chain Tech Adoption Curve, we hope to spark additional conversation and strategic interest around scaling tech companies that solve real challenges between the farm gate and consumer-facing service providers.

The Food Supply Chain Tech Adoption Curve

For the past decade we’ve tracked tech across the food system with our ag, food, and most recently, supply chain tech landscapes. While they’re helpful for discovering new companies and understanding the scope of alternatives, these landscapes stop short of helping investors and stakeholders to understand the alignment between maturity, adoption, and investment time horizons.

For this purpose, we have found various forms of the Gartner Hype Cycle useful, like the fantastic Agtech Hype Curve created by the former Monsanto Growth team for commodity row crops back in 2016.

We’ve often used this approach internally to map various systems in agrifoodtech and glean valuable insights in order to filter deal flow. Given the particular complexity of the systems and value streams within the food supply chain, this adoption curve has been especially useful in helping us visualize areas of opportunity.

We are the first to say that this is a subjective exercise, and a sub-sector’s placement relative to another can be more art than science, but in general our extensive research revealed clear market traction and adoption trends, especially relative to capital placement.

Please note that, in keeping with the four key pillars and sub-sectors of our Food Supply Chain Tech Landscape, we plotted relative adoption and maturity in the first mile (supply side); production and food processing; distribution and logistics; and demand side.

If you’re hungry, there are small, medium, and large-sized bites in this market

Investing into the food vertical — particularly closer to agriculture, production, and processing — means investing in the long game. It’s regulated, complex, and historically slow to adopt. If that’s not enough, here is what else we like about it:

- Few dedicated specialists: There has been a flurry of activity from corporate VCs, ESG and impact investors, and other new funds – but most are still primarily focused on investments at the end points (ie, consumers and ag inputs.)

- Underinvestment in modern tech: Food supply chains are still dominated by legacy specialized, or highly customized, horizontal enterprise solutions. As tech demand and spend increase, there is a strong need for platforms with food and ag-specific datasets and capabilities.

- Early-stage plays: We see venture opportunities to develop vertical plays in strategy and analytics, robotics and automation, and specialized logistics.

- Roll-up plays: Later-stage investors preferring de-risked technologies and proven customer traction can find returns with well-executed add-ons that focus on tight integration, interoperability, and investment in technical debt upgrades.

Early-stage innovators can be best-served by working hand-in-hand with internal R&D teams and others who have the right mindset for pilots and rapid feedback loops. Market-proven tech, on the other hand, is generally the domain of later-stage investors and internally-focused procurement, supply chain, and finance decision makers.

The bottom line is that all are an important part of the innovation process, but it is critical to understand where companies are on that maturity curve.

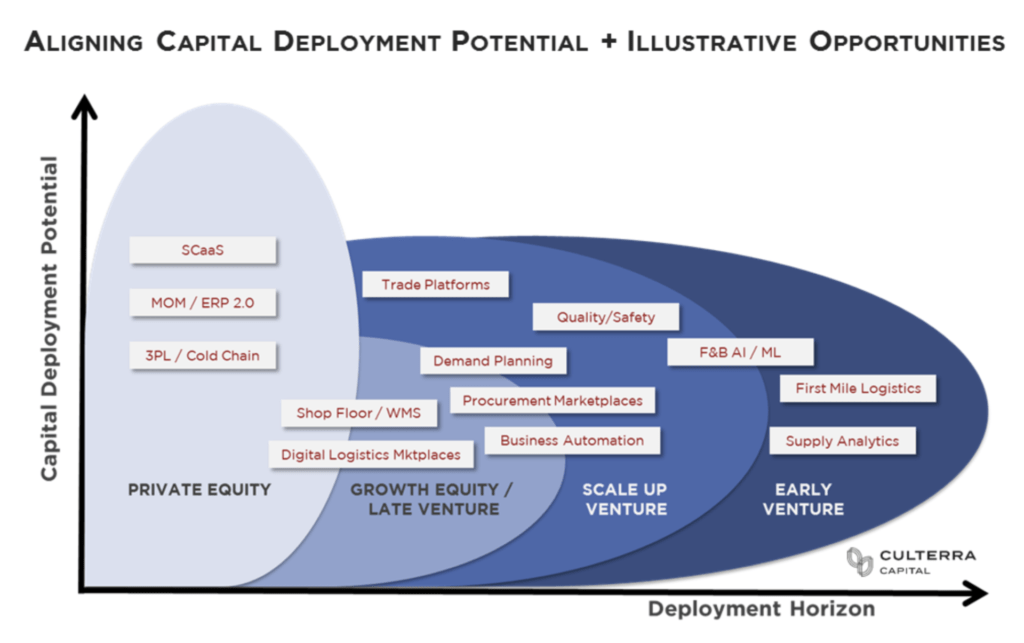

To illustrate what we mean by opportunities across the capital stack, we’ve highlighted a handful of target subsectors from our market analysis, overlaid with the predominant stage of equity investment given the maturity of those sub-sectors.

Supply chain has a long trajectory of value creation ahead

Let us leave you with a few data points which illustrate why we think the prize makes navigating the complexity worth it.

- Digital transformation will unlock and create entirely new market value across the $15 trillion food and ag global ecosystem, which represents around 15% of global GDP.

- There are over 400,000 global food processing facilities and 8,000 global food and beverage companies with $100 million-plus of revenue – so there’s a clear opportunity to capture significant IT spend as digital strategies grow.

- Tech sector investing is not slowing down. In 2020, US-based VC investing activity was at $124 billion and tech private equity investment was $134 billion. For comparison, US-based agrifoodtech companies raised about $15.5 billion in 2020, or 6% of that total.

- Food supply chain investment is still comparatively small and concentrated among a handful of mega-deals.

By our estimates, the global market for food supply chain tech is sized at $150 billion and growing. When you start to unpack subsectors like AI spend in food and beverage — which is expected to reach a market size of $30 billion by 2026 at compound annual growth of over 45% — the potential to transform this part of our ageing critical infrastructure is hard to overlook.

Given the scale, urgency, and near-term catalysts, we see the food supply chain as a goldmine of opportunity for building a tech-driven advantage. The next generation of leaders will need to be bold and committed to future-proof our food supply chain, and we look forward to the journey ahead.