[Disclosure: AgFunderNews’ parent company AgFunder is an investor in IIF.]

After leaving a career in finance, Nathan MacPhee entertained the notion of becoming a farmer — and quickly realized how unfeasible commercial farming would actually be for him.

“I didn’t have enough land and I wouldn’t have enough land to be able to farm in a commercial way,” he tells AgFunderNews. “And so I thought to myself, ‘If I can’t buy a farm, could buy a cow?'”

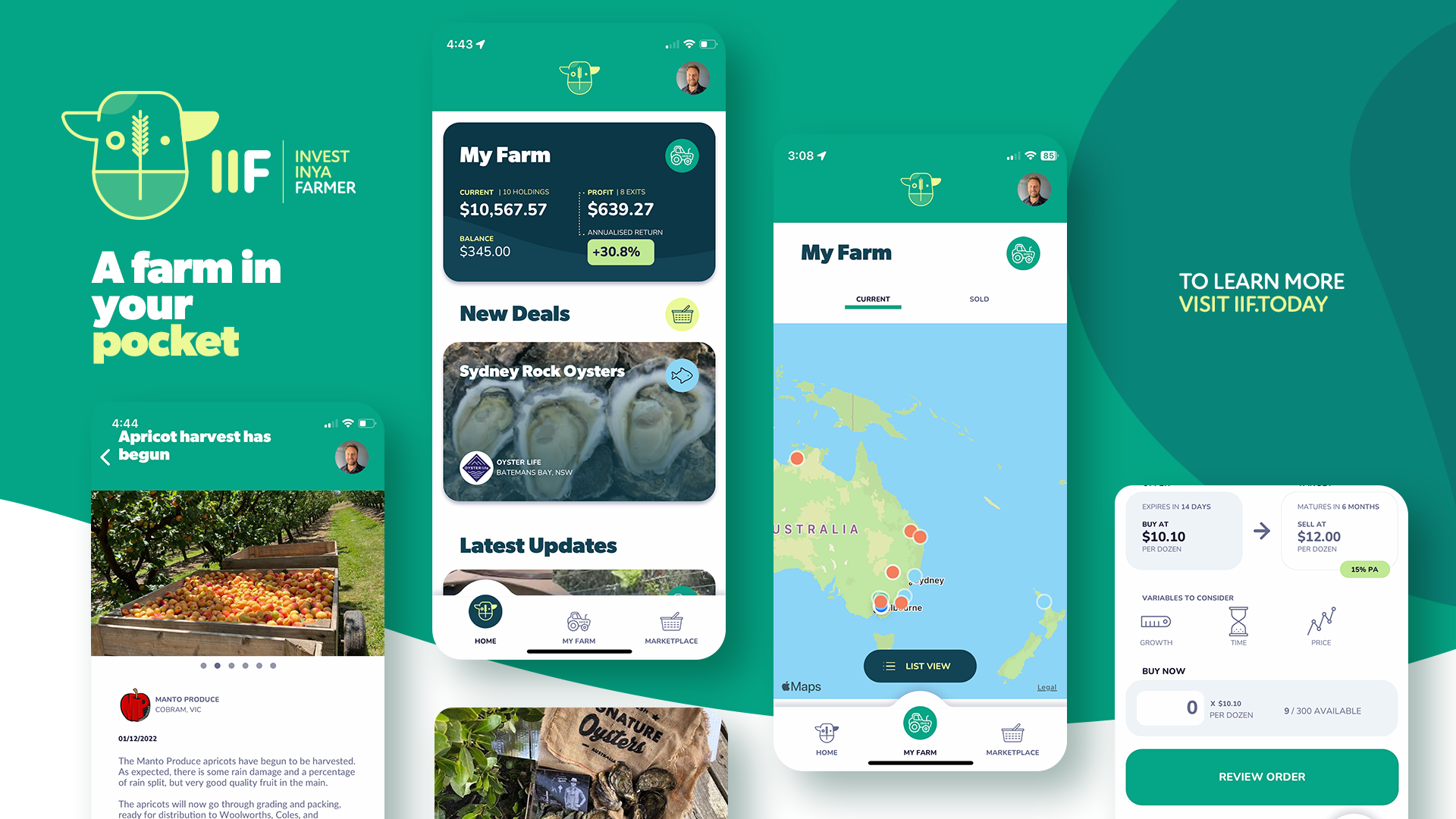

That question eventually led to the IIF (Invest Inya Farmer) cooperative, an investment platform that lets the average person invest in agricultural assets like crops and livestock and get a percentage of the profits upon sale of such products.

Via the IIF smartphone app, users can view investible assets — from beehives or single cows to a basket of oysters or an acre of tomatoes — and track the status of their investments throughout the season.

For farmers, the IIF platform shifts some of the risk from their shoulders to those of their investors.

“As an investor, you’re investing in what the farmers already doing and what they’re already good at doing. But in doing so, you’re providing liquidity and risk management to the farmer and building a connection with community.” says MacPhee.

“IIF stands out as one of the few bringing true innovation to address a structural problem in our sector: the misalignment of cash flows between growers and buyers in agriculture,” notes Jasper van Halder, CEO of New Zealand’s Agnition Ventures, which has invested in IIF.

Van Halder says Agition backed IIF because of “the uniqueness of IIF’s solution, the potential global market size, and the expertise within the founding team.”

“As part of a farmer-owned cooperative, we intimately understand the financial struggles farmers and growers face in the current climate—negative cash flows at the start of the season, uncertain post-harvest earnings, and significant loan repayments that must be paid monthly,” notes Van Halder. “IIF’s innovative equity ownership model helps farmers access capital from everyday investors, directly benefiting our farmers. Additionally, we believe their compelling solution will attract both urban and rural investors, bridging the gap between farmers and ‘townies.’”

AgFunderNews recently caught up with MacPhee to learn more about the IIF platform and it can benefit the farming community in Australia and beyond.

AgFunderNews (AFN): How did you go from working in finance to running an agtech startup?

Nathan MacPhee (NM): I worked in investments in quite senior positions in Australia and abroad for over 20 years. About six years ago, I moved from Sydney to regional Victoria for a lifestyle change. I simply decided I’d had enough of finance and decided to take some time out. Then COVID hit, and I actually spent the better part of the year at home doing not much but homeschooling the kids.

I was coming to the realization that I needed to go back to work and I thought, “Do I go back to finance?’ We live in a rural area, so we have farming to the left of us, farming to the back of us. I thought I wouldn’t mind becoming a farmer. Then I realized very quickly that I didn’t have enough land, and I wouldn’t have enough land to be able to farm in a commercial way. And so I thought to myself, “If I can’t buy a farm, could buy a cow?”

The cow is an appreciating asset. You buy a small one, then hopefully a year later you sell it at a higher price. I thought if I could invest in cattle, maybe I could build a portfolio of livestock at other farms.

The reason I thought there could be potential there was because my wife grew up on a farm and when times got tough, they often sold cows. A farmer doesn’t get paid until they harvest and sell. So whether they’re raising cattle or growing crops, it’s the farmer that has to carry all of the cost and all of the risk, and they don’t get paid until the end.

I thought, well what if they could get paid earlier?

Uniquely we don’t invest in farms; we invest what farms grow. It’s the production side we invest into. The first investments we ever made were into oysters. I met an oyster farmer and was explaining the concept of us investing into cattle, and he said you could do this with oysters. They take nearly two years to grow and [oyster farmers] don’t get paid until the end.

AFN: Walk us through how the investing process works.

NM: We present what are effectively share-farming options to our investors, who are investing at the start of the growing season. They’re buying a real cow, or they’re investing into a wheat crop that’s just been sown, or they might invest into fruit before it’s grown.

So there are real assets at the end of [the process] and the investor is in at the start, covering the farmer for all of their growing costs.

If the farmer is growing a row crop, investors cover the costs for the sowing, the growing and the harvest from day one.

For example, I [as an investor] can buy one acre of a lupin crop for $400. That is going to cover the cost of the farmer to grow [the crop]. Our target is that in eight to nine months, the lupin will be harvested and sold.

We’re expecting about one ton per acre at $500/ton. YIf it hits $500, you split the profit with the farmer and you would make 13% return on that investment.

Farmers keep investors up to date along the way [through the app].

Farmer obligation to repay is totally based on how that season goes. If, for example, cattle prices plummet, which they did in Australia, the investor wears the loss. If the crop is wiped out, the investor wears the loss.

So it gives farmers risk-free capital, and, importantly, investors can spread their risk.

For example, say I’m an investor with 28 holdings worth $26,000. I just bought into a lupin crop, I’ve got an Angus steer, some watermelons, dairy heifers, tomatoes, oysters, potatoes — a whole range of assets. Importantly, I’m incredibly geographically diversified, and so I’ve spread my risk.

AFN: What do you believe is unique about the IIF platform?

NM: Every investor invests in whatever they want. You build your own farm, the farmer keeps you up to date, and things come and go off the platform because we’re dealing in real-life agricultural assets.

As an investor, you’re investing in what the farmers already doing and what they’re already good at doing. But in doing so, you’re providing liquidity and risk management to the farmer and building a connection with community.

In a way, it is community-supported agriculture — it’s just that the community is the whole country and you don’t actually get the [food] product at the end.

AFN: How much does it cost the user upfront?

NM: Our model in Australia is quite unique in that we execute it through a cooperative, which is what we use to hold the assets. [Users] have to be a member of the coop (there’s a small fee for that).

Otherwise, the product itself dictates how much it costs. You have to buy a whole of something, but we have a number of offers on [the platform] that are less than $100. A dozen oysters might cost you $10. And you could buy one dozen or 33 dozen, we don’t really care. [On the higher end], one one steer will cost you $1,200. And you can’t buy half a steer.

AFN: Is getting paid earlier the biggest benefit to the farmer?

NM: It is, but we also recognize it’s not always about the money for the farmers. Good farmers often don’t need the money. And if they do, certainly in Australia, they’re too proud to ask for it.

What we provide is a form of smart capital. Good farmers are normally good business people, and they recognize that what we provide is risk-free capital.

If you go get a loan from the bank and the season turns against you — which happens all the time in agriculture — the loan doesn’t disappear, the debt doesn’t disappear.

So farmers are riding a “thriving years and surviving years” cycle, and we just want to give them a smoother ride.

Even outside of that, a number of our farmers us our platform to connect with consumers, so it’s a really good branding exercise. If someone’s invested in your pineapples, they’re more likely to buy them in a supermarket.

AFN: What types tend to invest via IIF?

NM: Our investors come from all walks of life. They’re 20-year-olds looking for something fun to do. They’re middle-aged women building up an investment portfolio. There’s other people chasing returns, but it’s not one dimensional for farmers, it’s very much access to capital to do more mitigating risk and connecting with consumers.

![]()

Sign up for our weekly newsletter.