Come rain, shine, or coronavirus, there’s just no halting the AgFunder research mothership. From a safe social distance this Thursday, AgFunder remotely unfurled its new 2020 Farmtech Investment Report — a data-driven snapshot of global investment in startups building technologies for the farm. [Disclosure: AgFunder is AFN‘s parent company.]

AgFunder’s flagship Agrifoodtech Funding Report, released in February, is broad in its scope, covering the whole food supply chain from farm-to-fork. And while we believe supply chains are getting shorter — and the increasing uptake of our term ‘agrifoodtech’ in the industry shows you all agree too — there are distinct trends, and sometimes capital sources, for technologies focused on farmers. So we extracted those deals from our broader dataset to give you this deeper dive.

$4.7 billion for farm tech in 2019

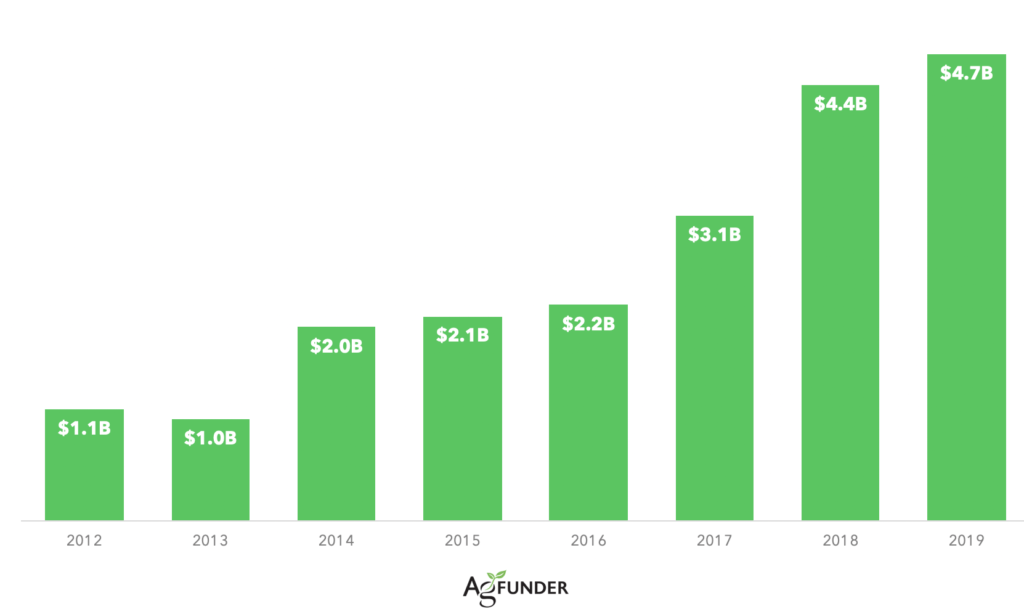

Farm tech startup investment bucked global venture capital markets across sectors by increasing 6.8% year-over-year to $4.7 billion in 2019; some 370% more than in 2013. Farm Tech startups raised that sum across 695 deals with 940 unique investors.

Given the social and economic fallout from the Covid-19 pandemic, the wider slowdown in VC funding could become a freefall. So similar growth levels are clearly not on the table this year, writes Louisa Burwood-Taylor, who heads up Agfunder’s research team.

“The economic fallout from the Covid-19 pandemic will no doubt impact the consistent growth in farm tech investment – indications for Q1-2020 investment levels are around $550m, which is far below the ~$1 billion raised in the first quarter of the past two years, and several hundred thousand less than Q1-2017,” she writes in the report. “While we believe investment in farmtech, and throughout the supply chain, is imperative to help the world’s food system recover from the impact of Covid-19, a fundamental drop in investment appetite is unlikely to buck this trend, albeit providing great opportunities for those of us still investing.”

With the benefit of 2020 hindsight, some 2019 deals look foolhardy while others look prescient as the pandemic squeezes supply chains, locks down consumers, spooks investors, and sparks a sudden rise of food nationalism.

One category that many investors may revisit with new vigor in light of Covid-19 is what the report calls Farm-to-Consumer eGrocery. These online platforms for farmers to sell and deliver their produce direct to consumers are more relevant today than ever before as consumers look to local food systems to secure food without needing to visit a local grocery store. Prior to this, they’ve represented a relatively small portion of the farm tech landscape – raising $202 million in 2019. But today we’re hearing about increasing numbers of farmers building their own e-commerce channels that could no doubt benefit from teaming up with some of the existing startups such as Barn2Door, which offers a plug-and-play e-commerce solutions for farmers who don’t want to build a website in-house.

Steward, an online investment platform for sustainable farms, is offering farmers a digital bridge to new retail markets with a new suite of software tools to make pivoting to a consumer market possible.

Similarly, the biggest deal of 2019, for those who see size as the bellwether for success, is also well placed to weather the Covid-19 storm. It was closed by the agri-marketplace ProducePay, which secured a $205 million debt financing to fund upfront payments to farmers selling their produce on its platform. That deal edged out another whopper that could gain from heightened calls for hyper-local supply chains; an unannounced $175 million insider round into Plenty, the plant factory startups based in California.

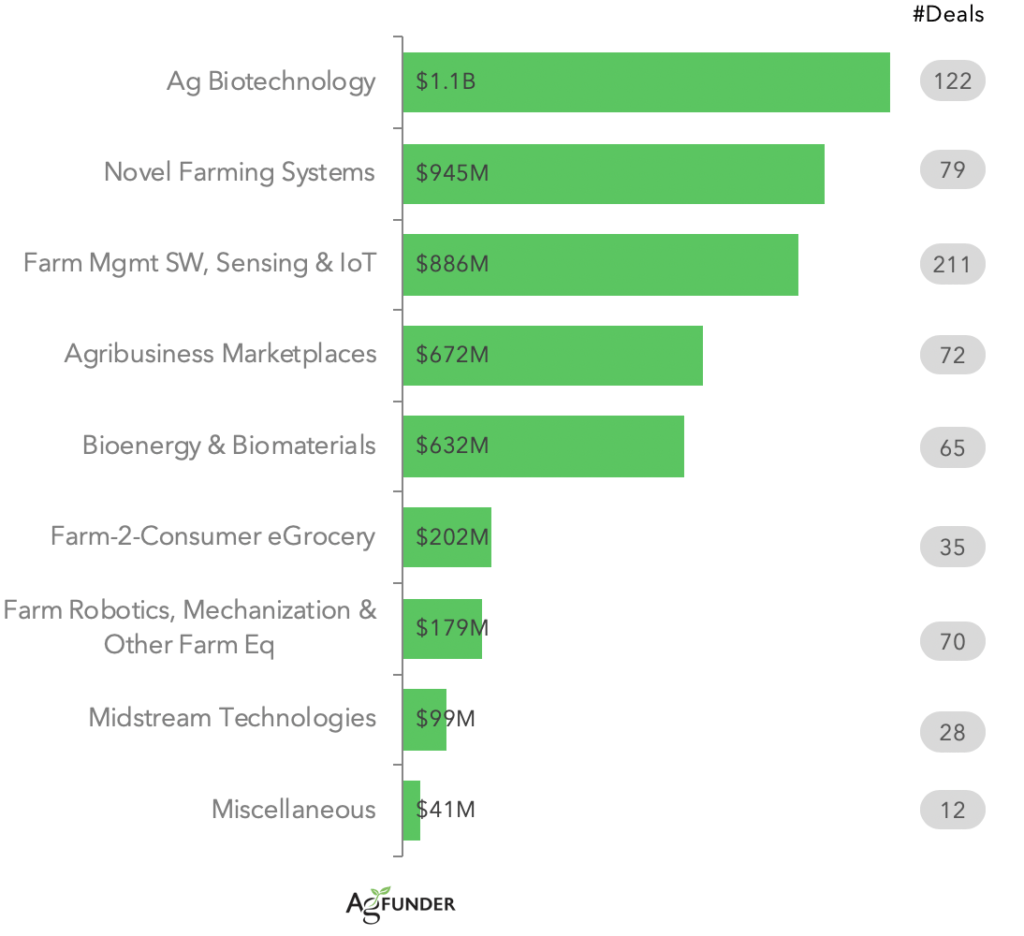

Elsewhere, the report uncovers that Farm Management Software, Sensing & IoT remained the most active category in farm tech by number of deals closed in 2019. Arguably this category propelled agtech into the venture capital spotlight in the first place; The Climate Corporation, which Monsanto bought for $1 billion in 2013, fit into this category! Geographically, this whole area used to be US-led; but 2019 saw that as sensor-based technology proliferates globally, other countries are catching up – for example, some 28% of deals in the category took place in Asia, most of them at seed stage.

Less impressively, Ag Biotech had a lean year in 2019. AgFunder research shows deal activity dropped 22% year-over-year while dollar investment declined 33%. Of those that still went ahead, gene editing remained at the forefront of excitement, despite a tricky regulatory environment to navigate.

Robo-social distance

Where there could be an upward trend in investments — a boom against the gloom, if you will — is agri-robotics. Investment in Robotic, Mechanization & Equipment startups is still surprisingly low, with many investors offering the excuse that hardware is hard. At $179 million over 70 deals, the category saw a 46% drop in funding across eight fewer deals in 2019 compared to 2018. We’re hopeful this could change, especially as robotics startups are receiving renewed interest from labor-challenged farmers today in the wake of the Covid-19 pandemic.

The report, of course, looks at a few more experimental roboticised farming systems and charts a pretty good year for insect farming. Ynsect’s robotized mealworm farming tech broke records with a Series C led by UK-based impact fund Astanor. It was the largest farmtech deal outside the US at the time and should keep Ynsect buzzing for a while, as long as the next pandemic does not mutate from a mealworm wet market.

The gains of a company like Ynsect were part of wider positive signs for farmtech in Europe. AgFunder data show a 23% rise in the total value of farm tech investments last year in Europe. And leading the charge on the continent was France, where the amount of capital flowing into farm tech startups more than doubled compared to 2018, to $346 million from $149 million. Other French farm tech startups that closed significant rounds last year include M2I Life Sciences, DNA Script, and Afyren – all of which were among 2019’s top 15 ex-US deals by dollar value.

Download the full report here.

What were your takeaways from the report? Send a critique to [email protected]