Editor’s Note: Barclay Rogers is head of business development at Ceres Imaging, a remote sensing startup using multi-spectral imaging from airplanes to provide farmers with insights about their crops including disease prediction, and irrigation and pesticide recommendations. Rogers has written a two-part, in-depth analysis on the development of the agtech market against a backdrop of low commodity prices and industry consolidation.

It’s been a long, dark period in the agriculture industry since corn prices tumbled almost five years ago. We still are not out of the woods as the threat of a trade war has suppressed commodity prices. Nevertheless, over the past five years, something magical has occurred: agricultural technology (agtech) has emerged as the dominant theme in a rapidly reshaping agricultural economy.

This is a two-part series explaining how agtech is transforming the agricultural sector and forecasting what is likely to be next in agtech. This first article of the two-part series provides a quick assessment of the current state of the agricultural economy, and highlights the rise of the agtech, especially as it relates to farm management platforms.

The second article will illustrate some of the core themes in agtech adoption to date, and predict the next phase in agtech development.

Agricultural Economy Continues to Struggle

Commodity prices reached record-highs from 2010 to 2013 based largely upon increased demand associated with ethanol production. However, as supply increased to meet — and eventually exceed — this demand, prices plummeted. With the price of other inputs, especially seed and land, remaining high despite the fall in commodity prices, farmers faced a period of tough years.

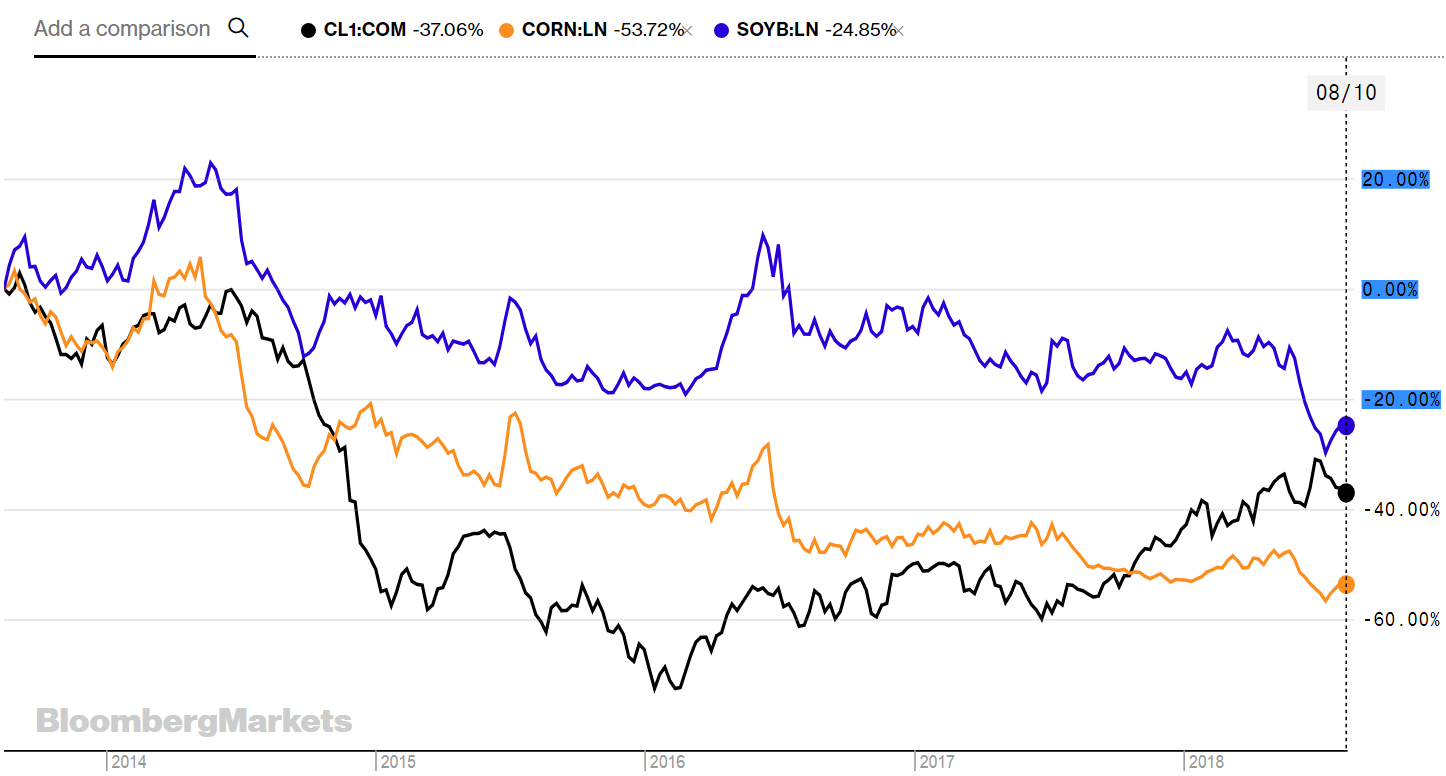

Corn and soybean prices had begun to rebound earlier this year alongside other commodities (e.g., oil) before taking a dive in May owing to tariff threats. The Trump Administration stepped in with $12 billion in relief funds for farmers to help offset the burden associated with tariffs. Congress also continues to work on a farm bill that may bring additional relief to the farm sector.

Soybean, Corn, and Oil Prices (2014-2018)

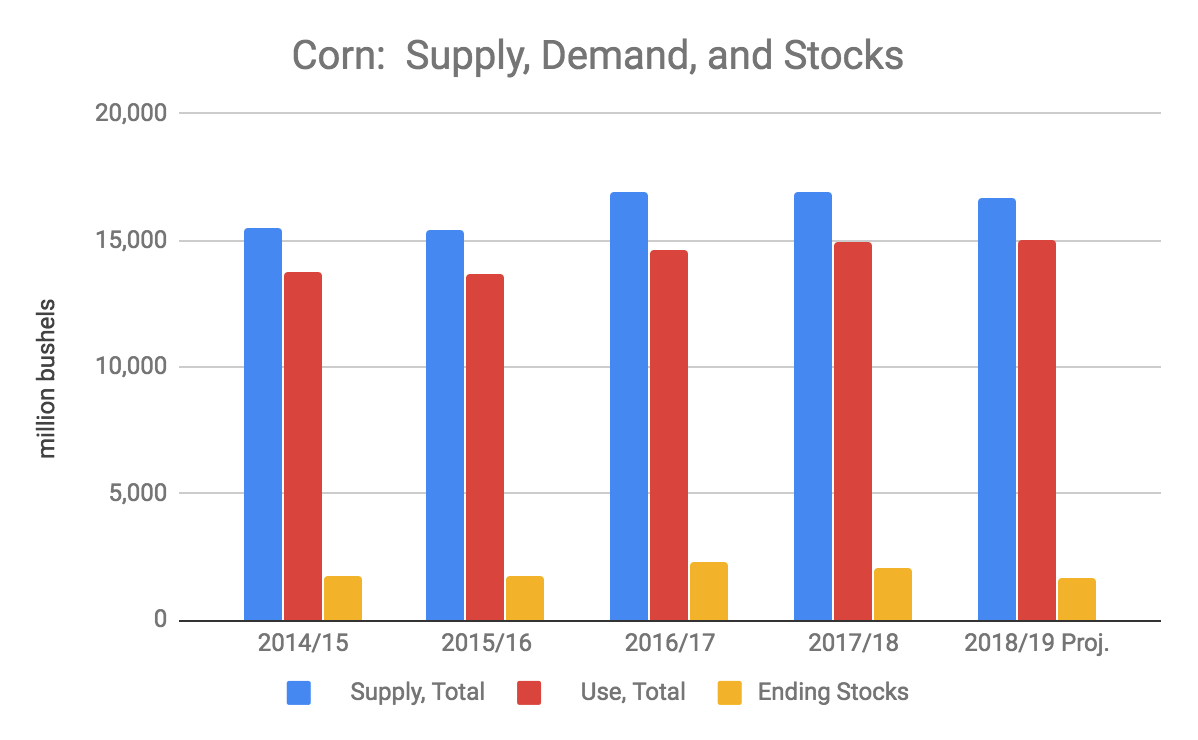

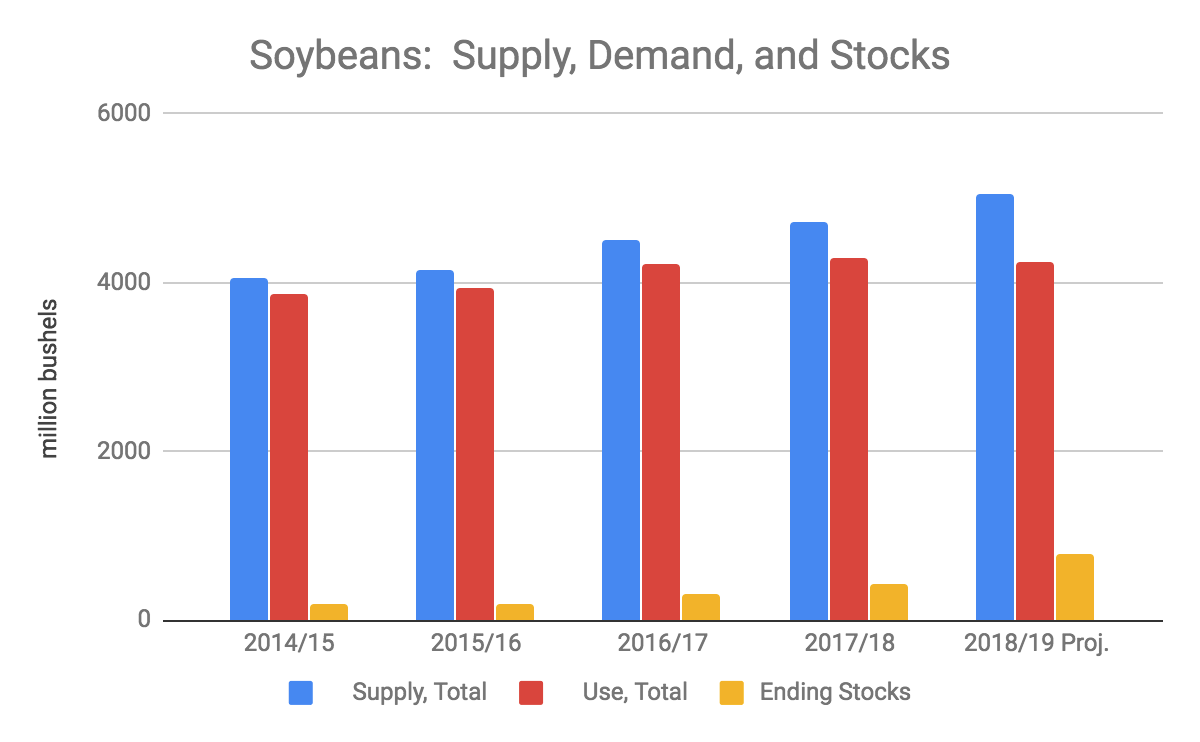

Economic conditions remain highly uncertain at the farm level. The USDA is projecting a good crop in corn and soybeans again this year. Under current projections, we’ll end up with ending stocks (a measure of year-to-year reserve that equates to annual supply less annual demand) in corn that are within the normal range; however, it looks likely that we will have above average ending stocks in soybeans, which suggests oversupply. Until we have a fundamental rebalancing of supply and demand — which is less likely if we start losing export markets — we may be in for an extended period of low farm commodity prices.

Agricultural Landscape is Changing

Notwithstanding the sluggish agricultural economy, the landscape is changing in two fundamental ways:

- Major consolidation at all levels

- Increased reliance on data to guide on-farm decision-making

Input Providers

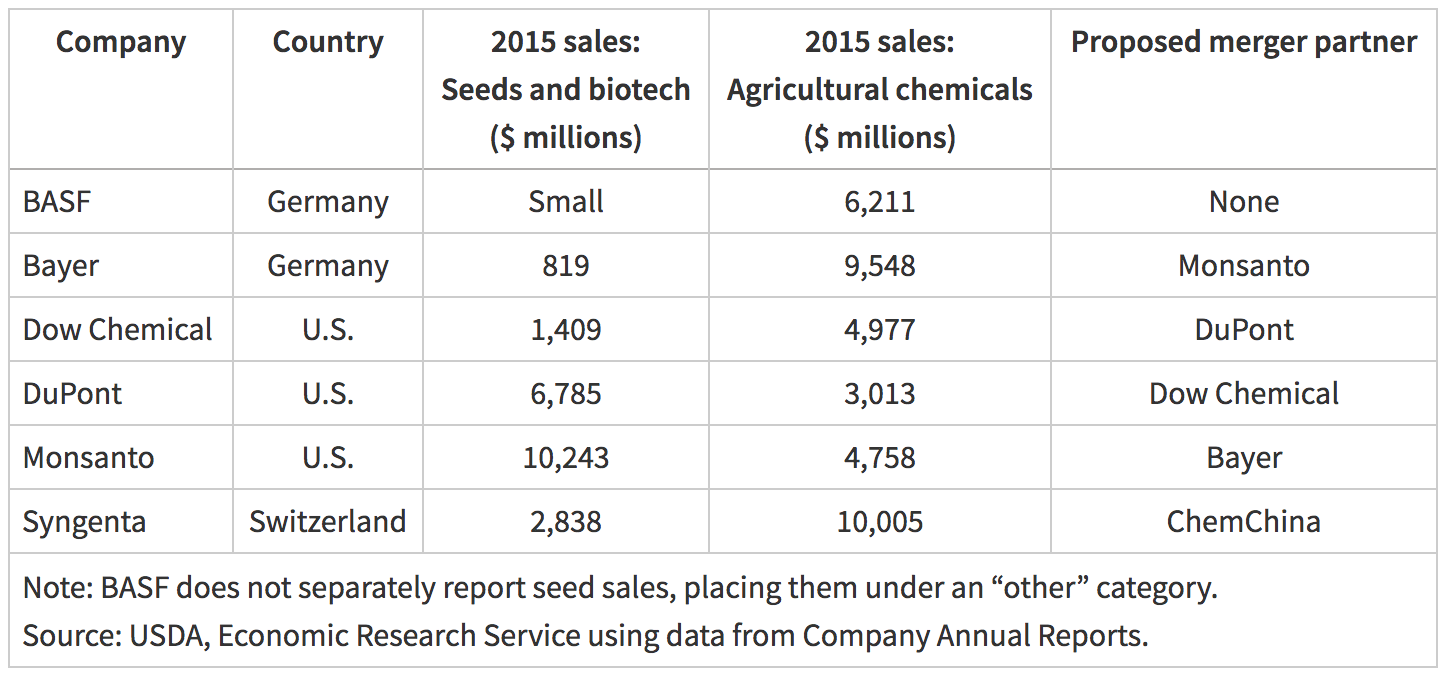

According to the USDA, “the ‘Big Six’ agribusinesses (Monsanto, Bayer, DuPont, Dow, BASF, and Syngenta) emerged in the 1990s and early 2000s as a result of mergers among large chemical, pharmaceutical, and seed companies, as well as acquisitions of many smaller seed and biotechnology companies.”

The World’s “Big Six” Agricultural Chemical Companies

The Dow DuPont merger was approved in September 2017, and the Monsanto-Bayer merger closed just last week. ChemChina acquired Syngenta in May 2017. The Big 6 is now the Big 4 and are more global than ever.

Data-driven farming platforms appear central to the future of agriculture. Monsanto’s acquisition of The Climate Corporation in 2013 — a digital software tool for farmers that took the lead in advancing data-driven farming — was a key component of the acquisition and, as Bayer explained in a release, digital tools are central to the company’s strategy going forward:

“We believe the agriculture market is expected to see an extension in the business model and new ways to interact with farmers at farm and field level. A combined Monsanto and Bayer will be well positioned to create a leading platform in the Digital Farming industry and advance the development of new technologies in this space.

“We expect that the combined business will greatly contribute to superior offerings being available to farmers in the years to come. In specific by offering:

- A leading digital platform with direct grower access;

- Best in class data analytics and reporting;

- Complementary agronomic knowledge and advanced modeling; and

- Broad scientific and commercial partnering network.”

Dow DuPont likewise is advancing its data-driven farming platform. In August 2017, Dow Dupont acquired Granular, a digital ERP platform for farmers, in order to “accelerate Granular’s business growth and help us deliver more value to growers around the world.”

Not to be left out, ChemChina has developed a Global Digital Agriculture program. In February 2018, ChemChina, via Syngenta, acquired FarmShots to incorporate satellite imagery and associated insights into “into Syngenta’s AgriEdge Excelsior whole-farm management system in the US.” Following the acquisition, Dan Burdett, global head of digital agriculture at Syngenta, told AgFunderNews that the major agricultural input providers are in a “race to have the digital relationship with the grower.”

BASF is also getting in on the farm data management game. In March 2016, BASF launched Maglis in an effort to connect “data, technology and people in a smarter way, so that farmers can grow, market and live smarter.” BASF has continued to invest in digital agriculture through its acquisition of ZedX in April 2017, partnerships with other ag data and analytic companies like Proagrica, and the acquisition of Bayer’s digital assets as part of the Department of Justice’s requirements in Bayer’s acquisition of Monsanto.

The data game is being played by others in the ag input space outside the major seed and chemical players. For example, John Deere, the largest farm machinery manufacturer, has developed its Operations Center to “collect data more easily, access it more readily, and analyze it more effectively.” Yara, a major fertilizer company, acquired Adapt-N in 2017 to “provide farmers with detailed fertilizer prescriptions, to avoid overuse and wastage. Valmont Industries, the leading center pivot irrigation manufacturer, acquired AgSense in 2014 to provide “growers with a more complete view of their entire farming operation by tying irrigation decision making to field, crop and weather conditions.”

Retail Channel

The retail channel is undergoing a similar transformation with increased consolidation and rapid development of data-driven platforms.

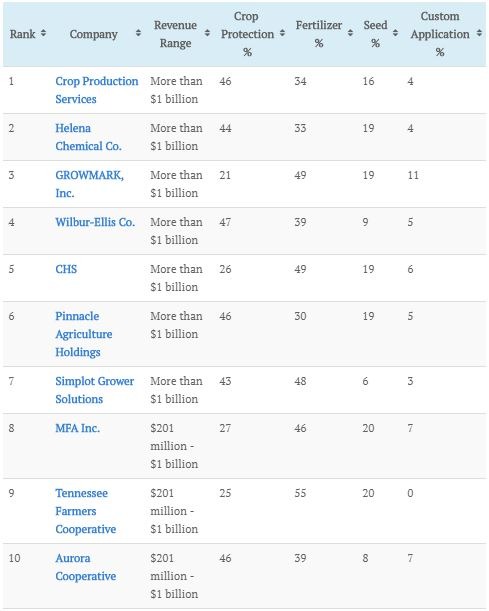

Crop Life identifies the leading agricultural retail companies each year in its Top 100 listing, with the current top 10 as follows:

Top 10 Ag Retailers

Concentration is a major theme in the agricultural retail space with the following companies growing aggressively over the past few years:

- Pinnacle Agriculture Holdings acquired Jimmy Sanders in 2012 and has continued to grow through acquisitions

- CHS has grown into an international giant primarily through acquisitions

- Many small ag coops have begun consolidating to form powerful retail and grain marketing entities (e.g., Landus, Aurora, and Frontier)

Data-driven farming platforms are becoming central to the ag retail space as well. According to Daren Coppock, CEO of the Agricultural Retailers Association, “Precision ag is definitely growing into the future, with the key to the precision ag puzzle being who can be first to make sense of overlapping spatial data for yield, fertility, soil characteristics, weed pressure, topography, weather, etc. stretching over multiple years — and extract from it meaningful conclusions for planning forward.

SST has long been a leader precision agriculture software and is used by many agricultural retailers. Agrian is becoming a dominant player, building customized data platforms for (among others):

As we have seen in Part 1, notwithstanding the fact that the ag economy remains in the doldrums, the ag input and retail sectors are rapidly integrating data-driven farming platforms into their core business. In Part 2, we explore the agtech adoption trends to date and explore what is likely to come in the next wave of agtech innovation.

*Keep an eye out for Part 2 coming out next week, September 4, 2018*