Agrifood corporates must take more action faster to advance alternative protein portfolios and reduce their supply chain emissions, according to investment network FAIRR.

FAIRR’s latest engagement found that nearly half of the companies it works with are “maintaining, rather than accelerating” when it comes to alt protein.

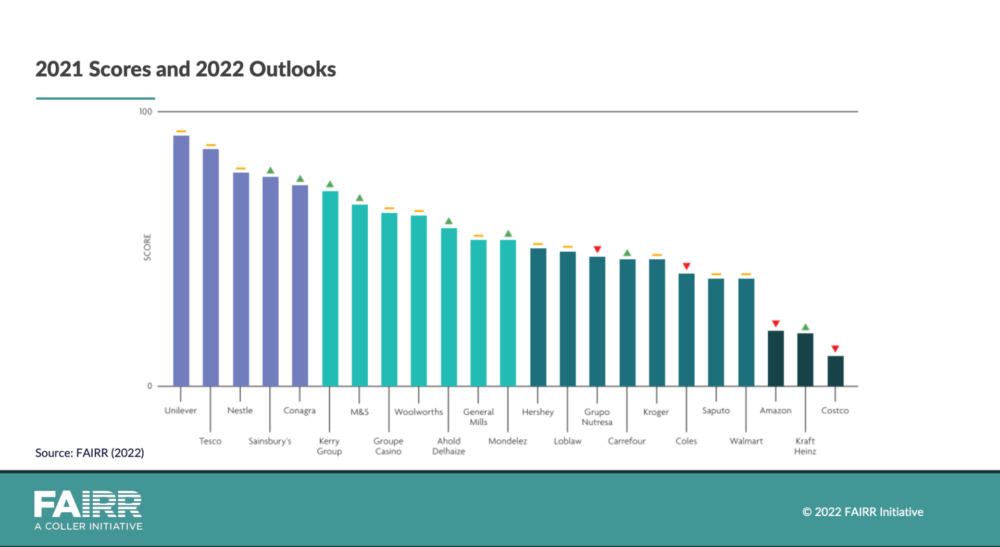

Unilever, Nestlé, Kroger, Amazon and Kraft Heinz are among the 23 major food corporates FAIRR collaborates with for the annual engagement, which measures progress in alternative proteins. Overall, 48% of these companies have a neutral outlook, while 35% of have a positive outlook. Another 17% have a negative outlook.

These companies must tackle price parity, product diversification and consumer engagement strategies in order to accelerate adoption and meet net zero targets.

How can they do that? AFN recently spoke to Sofia De La Parra Saravia (SDLP), a senior ESG analyst at FAIRR who focuses on the alternative protein engagement. Below are her insights on the engagement findings and what companies must do today to enact change for the near-term future.

AFN: How does FAIRR go about choosing the companies for the engagement?

SDLP: Since FAIRR is an investor network, we think on a systems approach. So we look through the entire supply chain. We engage with companies from agri-chemical, providing feed or pharmaceuticals for livestock, all the way up to restaurant chains.

The State of Proteins [engagement] we’ve been running for six years now (the longest running one), targets some of the largest food retailers and manufacturers around the world. The criteria we use is around marketshare in the markets that they operate in. Also the share and the ownership from their members. That’s a key one. Given that [the engagement] is something we’re facilitating on behalf of the investors, it was really important to have investors that are actually holding the companies participating in this dialogue.

Also market cap and a little bit of geographical diversification. I’m very much aware that we’re still kind of based in the US and Europe, but we did try to consider that.

We started with 16 companies. We went up to 25. And then from last year to this year, we dropped two, ICA Gruppen and Morrison’s, because they became private companies.

AFN: One of the engagement’s major findings is that companies are maintaining rather than accelerating progress with alt-protein. Why is that?

SDLP: Almost half of the companies are on track to stay where they’re at without really accelerating their project progress.

What we need to achieve the systemic change required for 1.5 by 2030, and by 2050, is quicker action. I think it’s the same kind of takeaway from COP27 — more action is needed.

On the Net Zero commitments, there’s definitely been a big improvement from the last three years. Then we had 8% of the companies that had some sort of net zero commitment. Now we have 70% of the companies.

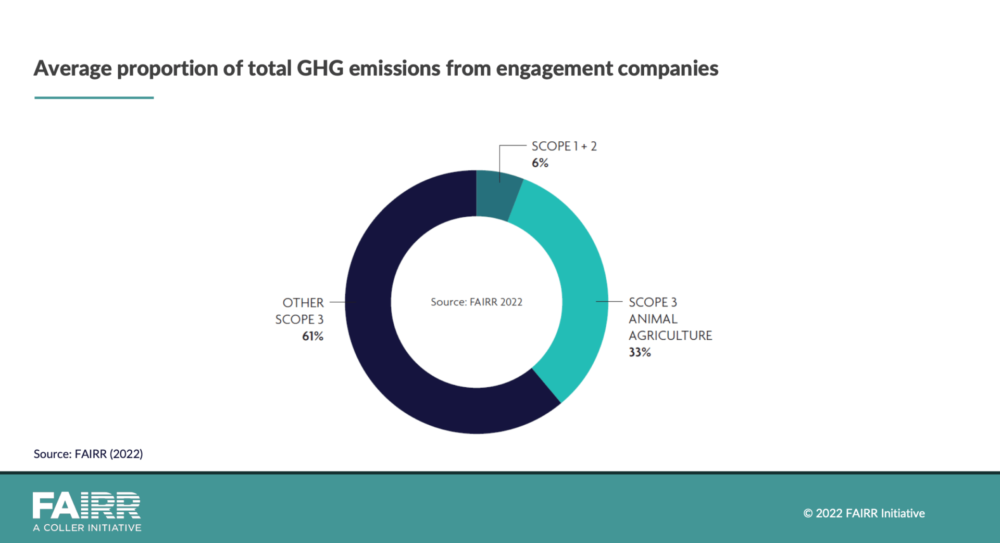

But when we look at this target and we look at the quality of these targets, we see that there’s still a lot of room for improvement, given that 50% of these targets actually don’t cover the supply chain. This is a problem because for these companies specifically, 94% of their total emissions lie in their supply chain. And if you take a deep dive there, on average, 33% is linked to animal agriculture.

Inevitably, getting to your long term goal means looking at that 33%. How do you tackle that? Well, there’s a lot of opportunity. There’s a lot of talk about regenerative agriculture, but that also has a limit of how much you can just source more sustainably.

We insist on diversification because that’s where we see there’s an effective and real opportunity to tackle those scope 3 emissions. There’s still a lot of untapped abatement potential from exploiting alternative proteins in this portfolios.

AFN: So, for example, a burger chain can’t simply source more sustainable beef? It would have to also diversify its menu with more alt-protein?

SDLP: Absolutely. Because it’s so difficult to measure the actual potential that regenerative agriculture would have. There’s still a lot of nuances and question marks around the actual maximum [of regenerative ag]. So you don’t want to put all your eggs in one basket. We need to address the fact that we need to change our behavior and diversify.

AFN: On that note, let’s talk about cultivated meat. What does Upside Foods’ recent milestone suggest for the industry?

SDLP: They [Upside Foods] still need to get approval from the USDA. But this is definitely the furthest that a company in the US has made it, the US being second after Singapore, which approved [cultivated meat] two years ago with Eat Just. I understand more than 100 companies are waiting to get approval.

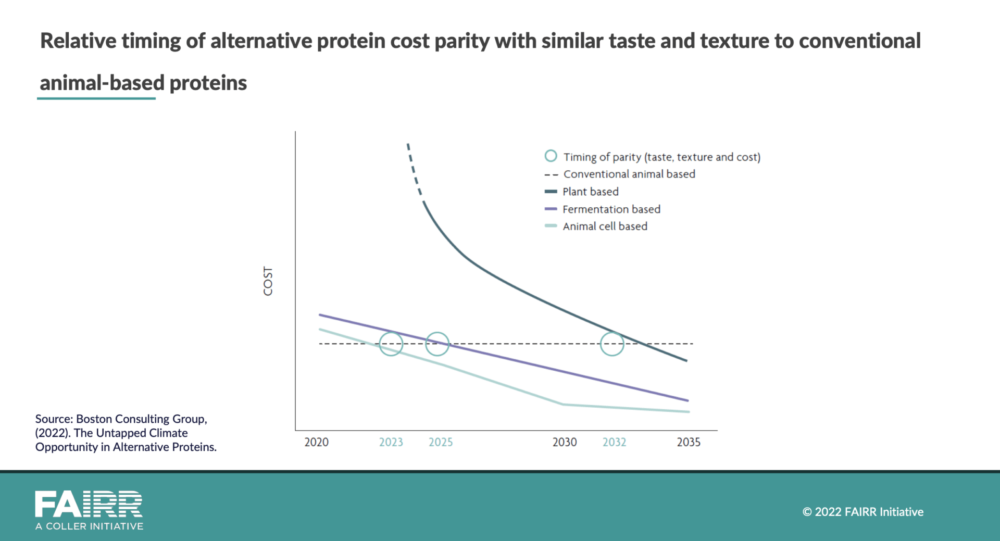

We we had a table in our report around other countries or regions that we saw were also in the medium term: the European Union with the Netherlands. They’ve already approved private tastings. Also Israel and Qatar.

AFN: What are the big challenges for alternative protein right now?

SDLP: One of the key challenges is to really be able to tackle the affordability, convenience, taste and nutrition profile that some of the animal derived products have. So definitely using technology and thinking outside of the box. Where things get very interesting is in hybrid products.

There are challenges around policy and regulation. Obviously, approval is key here. But there’s been so much lobbying around like labeling constraints, the whole ISO issue as well.

We also need much more coherence from a policy perspective on using blended finance, using public money to de-risk the sector. In the report, we say around $120 million has been invested in this sector. It’s something, but it’s not a game changer. If you think about EVs, for example, that was so much more money governments have put into decarbonizing electric vehicles. We’re going on the positive direction, we just need more robust and coherent strategies are needed.

AFN: What about the health factor of alternative proteins? I’m thinking of plant-based meat in particular.

SDLP: I do think that we sometimes forget whole-food plant-based proteins legumes, beans and and other things that don’t need to be processed and are already cheaper.

Part of the equation is to not just do a swap one for one. Especially when we start putting more complexities to the system about health and nutrition, the fact that you just swap one for one, the sausage or the beef patty or the nugget is not really solving the issue. We don’t want to solve one problem by creating another one.

AFN: Do corporates need to play a bigger role in shifting consumer habits to alternative proteins?

SDLP: We see supermarkets and food manufacturers actually spending quite a lot of resources into R&D, developing these products, and developing their own brands.

But there’s that lack of actually engaging with the consumers to to support them in that transition [to alt-protein]. As of now, it’s been very driven by the consumer demand. Now there’s also a lot of people are concerned about costs going up. So just laying back and still expecting consumers to be the drivers I think is something that is a challenge.

Companies need to play much stronger role in pushing these products. They have so many tools that they can use in terms of marketing spending, where they place the product, how they’re packaging it, how they’re commercializing it. The fringe consumer is not going to jump on the boat if you’re talking about environment, but if you talk about, say, animal welfare, they will.

Nudging consumer behavior is a big area for for improvement for all of the companies that we engage with. So I think those strategies need to be actual strategies with budgets, and I know they always like say that they cannot tell people what to buy, but they do, actually.

There’s a lot of media around things like the Beyond Meat case or McDonald’s McPlant not performing as expected. I think it’s very important to draw a broader view. Those specific examples are not a diagnosis for the for the sector. There’s still quite a lot of opportunity, and it’s very exciting that in the longer term, it still makes a lot of sense — from the companies’ perspective and from the investors’ perspective.

![]()

Sign up for our weekly newsletter.