Data Snapshot is a regular AFN feature in which we analyze agrifoodtech market investment data provided by our parent company, AgFunder.

Click here for more research from AgFunder and sign up to our newsletters to receive alerts about new research reports.

The 2022 Africa AgriFoodTech Investment Report by AgFunder in collaboration with the Dutch Entrepreneurial Development Bank, FMO and British International Investment was just released yesterday.

The year 2021 was huge for African agrifoodtech startups as they secured $482.3 million in investment, a 250% jump from $185 million they raised in 2020.

But where did most of the money go?

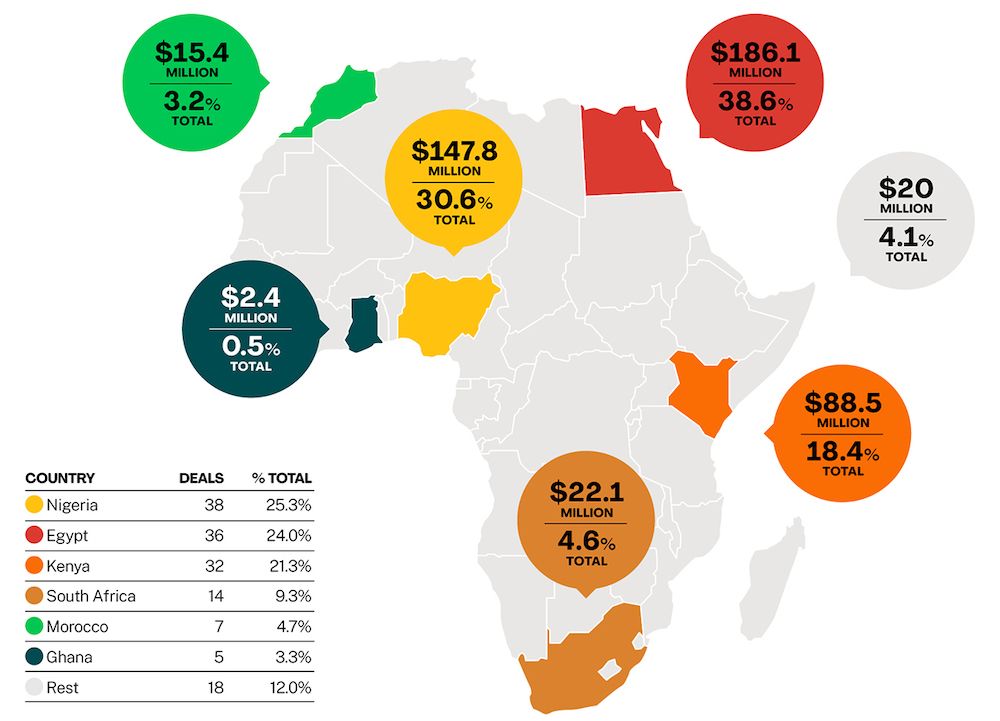

While various technologies dictated the flow of financing, the vast majority of venture capital went to the three main startup hubs on the continent: Nigeria, Egypt, and Kenya.

Collectively, startups from the three countries secured 87.6% of total African agrifoodtech investment in 2021.

Overall, there were 150 investment deals, which were snagged by Nigeria, Egypt and Kenya-based startups across 38, 36, and 32 deals respectively.

This is not just a trend in the agrifoodtech sector but a common theme across venture capital investment on the continent, which tends to flow into these main hubs across categories including fintech, healthtech, and e-commerce, according to various data sources.

While South Africa was the fourth largest market for agrifoodtech investment, it brought in just 9.3% of overall funding. That bucks the typical trend for it to join Nigeria, Egypt and Kenya as one of the leaders.

Those four economies have higher startup concentrations, higher populations with bigger economies and are also home to over 80% of the continent’s incubators and accelerators, according to an African Development Bank report.

Deal count is not reflective of deal value

Even though Nigeria led in deal count, it came second in deal value to Egyptian startups which raised $186.1 million.

This could be due to the fact that apart from having a thriving startup ecosystem, Egyptian startups have the advantage of securing investments from active local and MENA (Middle East and North Africa) focused investors.

Aside from private sector investment, the Egyptian government has also over the years been very supportive of the ecosystem, rolling out policies and financing in support of the local tech ecosystem. This could perhaps be the other contributor to Egypt’s increasing appeal to investors.

Earlier this year, the government launched a $50 million VC programme with the aid of the World Bank to finance new and existing investment funds. In 2022, the government also scrapped the need to physically register startups. Entrepreneurs, through the new initiative, can digitally register their ventures helping them save time and money.

In 2021, the National Bank of Egypt received a $100 million loan from the European Bank for Reconstruction and Development to support agriculture, industry and commerce SMEs. The move was to help them become more resource efficient and support their efforts in climate change mitigation.

Egypt’s Ministry of Internal Cooperation also partnered with the private sector to launch Egypt Ventures, which disbursed around $4.7 million ( EGP 92 million) to support local startups.

Other notable efforts by African governments to support their startup ecosystems have been in Tunisia and Senegal where the governments passed startup acts in 2018 and 2019 respectively. Kenya is also on the same path with a startup bill in 2020 and Rwanda is reportedly edging closer to passing its startup act.