Editors note: Vonnie Estes is an executive with over 20 years of experience in leadership roles commercializing biotechnologies. This article originally appeared in BioFuels Digest.

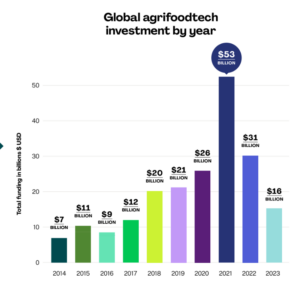

Having spent more than twenty years commercializing technology in the agricultural sector, I’m excited by the growing interest and investment in Agricultural Technology (“AgTech”). AgTech did not receive much attention from venture capital prior to 2012. Investment in 2012 was around $150M – and then it exploded to $1.8 B in 2014. Investment momentum is continuing into 2015. Much of this investment is in the same technology that has investors fired up in Silicon Valley – software, drone technology, IOT, big data, life sciences, and mobility. All of these technologies can be applied to agriculture to inform decision-making – creating a new market for these technologies and returns for investors.

Agricultural production must increase by 60% by 2050 if we are to meet the needs of the world’s growing population. We’ll need to feed 10 billion people while trying to eliminate the negative global environmental impacts of crop production by reducing chemical and water inputs and land requirements. We’ll also need to figure out sustainable crop production for energy, chemicals, and fiber.

We need major innovation to improve agriculture’s efficiency and productivity. Innovation requires continuous investment – and AgTech is a smart investment. In this article I will examine what early investors should consider, current areas of growth and interest in AgTech, and who is putting up the money. There is tremendous societal and environmental value in moving capital into Agricultural Technology innovation, and there is value for the investor in return. I would like to see capital directed to technologies, companies, and collaborations with a high likelihood of commercialization to give agriculture its best chance of improving in a sustainable way while making money for investors.

So You Want to be in AgTech

My first questions would be Why? and What are your expectations?

AgTech has had very few big liquidity events. The Climate Corporation, acquired by Monsanto in 2013 for $1 billion, is the major exception. Historically, strategic investors have quietly picked up most AgTech companies for 2-3.5X returns at best. Or companies have struggled with multiple rounds (some down rounds) to make it on their own. Investors should not expect 30X returns. I’m hoping this will change, but investors should be prepared for it not to.

The ag sector faces challenges most industries don’t and that many investors don’t understand. Bad weather can wipe out a field trial, necessitating the repeat of a year’s data collection. Companies often have only one shot per year to prove a technology or system. Biology doesn’t always act in predictable ways. EPA, USDA, and FDA impose regulations on those who change food systems whose registration requirements can take up to 10 years to meet. Money must be patient – not a quality present in most venture capitalists.

Channel, Channel, Channel

There may be some opportunities for Uber- or Airbnb-type disruptions. I hope so. However, most products will go through current channels. Many of the start-ups I’ve worked for in the past have said, “If we can just get 1% of the corn acreage . . .” Well, we couldn’t and we failed. Infrastructure and supply chains are well established, and switching cost is high. Any technology that involves a seed will have to go through established seed distribution systems to get widespread market adoption. Any sensor, drone, or robot that gathers data will need that data integrated and delivered to the farmer in a way that will allow for better decisions. Do not ask anyone to do things differently in the supply chain. If the product will go through the normal distribution channels, it needs to be able to withstand sitting in a truck in Iowa at 100 degrees or being stored in a warehouse for a year.

Listen, Learn, Integrate

Highly educated people from Silicon Valley have much to offer farming systems in the way of technology and business models. The magic will be in integrating that knowledge and experience with that of farmers. Farmers understand farming economics. They know how to get product from the field and understand biological systems. Do not expect farmers to “take your word for it” and spend capital with someone they don’t know. They come from tight community ecosystems and you are from the outside. Many farmers use consultants or ag extension agents, and you will get farthest if you can be recommended by one of them. If you are fortunate enough to get time with a farmer, turn off your phone, take a deep breath, and listen.

Hot Areas of Current Investment

Digital

This is the area creating the most buzz in Silicon Valley, and the one with the biggest potential to be disruptive. It encompasses many technologies and crosses numerous steps in the value chain such as genetic engineering, information technology, drones, sensors, and smart machinery. Data and analytical systems can inform decision-making and make more sustainable and profitable use of land. It is also an area getting quickly saturated.

- Analytics engine at core The biggest challenge and most value-add will be to take all that data generated from multiple sources and turn it into information that a farmer can use to make informed decisions through real-time data coalition, analytics, and decision support tools. The nonaggregated data is noise. The power (and returns) will be with those who have the analytics engine. Monsanto is certainly moving in that direction with Climate Corp. The other majors are doing the same. The aggregator must have access to growing systems, farms, infrastructure, and channel, and understand how they work.

- Technologies that feed into the analytics engine

Many start-ups are developing supporting technology for the analytics engine – drones, sensors, software, machinery, hardware. Many of these technologies will end up being commoditized in the future but they need investment now. There are good returns to be made in their development.

Biologics

Microbial solutions are currently a $2.3B market and growing. Derived from naturally occurring microorganisms such as bacteria and fungi, microbials can protect crops from pests and diseases and enhance plant productivity and fertility. The aim is to deliver microorganisms, mostly through seed coating, to improve crop growth and health, producing higher yields with less input. Monsanto and Novozymes created the BioAg Alliance, putting in $300M for R&D, and number of other companies are popping up with strong investors: Agbiome (with the Who’s Who of investors) has raised $17.5M, Bioconsortia has raised $15M from Khosla Ventures and Otter, and Symbiota (with the Who’s Who in ag boards), a Flagship Ventures company, has raised $7.5M, to name just a few. These technologies are seeing 10–20% plus yield improvement in greenhouse and field trials. An area of needed innovation is in application and channel of microbial products. Remember that truck in 100 degrees in Iowa? These products will have to withstand heat and long storage times to be sold through current distribution networks. Technology supporting application, seed coating, and shelf life needs development. These are solvable problems, but will take money and likely more time than investors expect.

New crops

Creating a new crop that will reap big returns is no easy task. It takes good science, capital, time, willing farmers, seed scale-up time, and a market. For VC investment purposes, there could be some blockbuster crops for food, fiber, energy, and chemicals. Each possibility should be evaluated on its commercial merits, keeping in mind the long testing and production cycles. Some of the top companies working in energy crops for biofuel and power production are NexSteppe, Chromatin, Ceres, and Genera Energy. New entrepreneurs and investors should learn from their accomplishments and struggles. There will be a boutique market for non-soy protein, gluten-free grain, and quinoa-type crops but it is unlikely they will reach production agriculture status within 10 years.

Food and agricultural residue converted to fuels and chemicals

Due to the low price of oil, highly visible failures, high cap-ex, and eroding government support, VCs do not want to hear the word “biofuels.” However, using food and crop residues to produce higher value chemicals addresses two societal problems: getting rid of waste and displacing petroleum products, thereby decreasing greenhouse gases. A number of companies are at various stages of funding and success: Earth Energy Renewables, Genomatica, Green Biologics, and Zeachem. Innovation in this space is certainly needed. Oil will go back up, and second-generation fuels will be back at some point. Technologies developed for chemicals can be translated to fuels at the right time.

Ag Biotech

The big companies (Monsanto, DuPont, Syngenta, Bayer) have currently saturated the seed trait market. The biggest markets are herbicide resistance and insect and disease control in soy, corn, and cotton. A large portion of the technology held by these big companies will start coming off patent in 2021. Until that time, IP will be an issue in this field. Athenix is an exception. They developed herbicide tolerance and insect control traits for corn and soybeans and got picked up by Bayer for $450M. Even if free of IP issues, the technology will need to go through one of the large companies for a route to market. The exit will likely be to a strategic. There are opportunities in seed trait development – but keep an eye on IP, route to market, long timelines, and lower exit values to strategics.

Urban Ag

Companies will make money growing high-value crops/protein in urban environments. This is the 21st century version of “gentleman farming.” Companies are growing crops and fish in city locales to satisfy consumers willing to pay high prices for product consistency and year-round availability. There may be some later application of these technologies to desert or overpopulated areas with land shortages. For now, I would leave development to hobbyists or friends and family funding. Let’s use big venture money to feed the world in a sustainable way.

Who is Investing

A number of different models are emerging to meld VCs, strategics, big data analytics, farmers, and entrepreneurs together in a winning combination. Most groups discuss creating an ecosystem similar to Silicon Valley in which these new companies could thrive. Geography is a hurdle but can be overcome. Many groups are setting up regional AgTech centers in agricultural communities in the Midwest and Southeast.

A few of the models:

- Accelerators / incubators. Everyone in this group has a different model. They are all trying to set up an ecosystem for entrepreneurs that would increase access to resources, customers, and partners. Some will pick four to six companies and fund and mentor them; others are more connectors. This allows companies to spend less money on building infrastructure and potentially lower the amount of money required to be raised. The more active current groups in this category are:

- Alexandria – Raleigh Durham, NC. Accelerator with strategics and VCs

- Yield Labs – St Louis, MO. Accelerator investing in start-ups

- AgTech Innovation Fund – Davis, CA. VC fund investing in early-stage

- RoyseLaw AgTech Incubator – Palo Alto, CA. Incubates 12 start-ups in 5-month program

- Steinbeck Innovation Cluster – Salinas, CA. Connector

- Farm 2050 – Palo Alto, CA. Connector

- AgFunder- San Francisco, CA. Connector

- Venture capital firms: A number of more traditional VC firms have been investing in ag for years along with some that have moved over from Clean Tech. Many are starting new ag-based funds or incorporating ag investments into current funds. A small sample of this investor class:

- Kleiner Perkins Caufield & Byers’ Green Growth Fund

- Cultivian Ventures, LLP

- Flagship Ventures

- Harris and Harris

- Paine and Partners

- Finistere Ventures

- Corporate venture funds: Most large companies have had venture funds for years, but seeing them now as a potential innovation engine, have recently changed how they manage them. They are bringing in managers with professional investment backgrounds. Strategics get more value from technology over time than VCs, and are more patient money. They have a huge influence on what technologies will get to market due to added funding, understanding of business, and route to market. Examples of these are:

- Monsanto

- DuPont

- Syngenta

- Bayer

- Dow

- BASF

- DSM

- Andersons (Maumee Ventures)

Summary

There is a bright future for investors in bringing the funding and data analytics of Silicon Valley to the real problems faced by farmers. The industry will deal with challenges around biology of timing and weather cycles; the regulatory timelines of government; and the business challenges of value capture and sharing, formulation, and distribution. With innovative farmers and smart money, I believe these can all be overcome. Through innovations along the value chain we can boost productivity and efficiency of farming to meet the needs of our growing population in a sustainable way.

To contact the author responsible for this story email Vonnie Estes at [email protected]

Sponsored

International Fresh Produce Association launches year 3 of its produce accelerator