What do the following agrifoodtech categories have in common?

- Plant-based ingredients

- Pollination and bee-tech

- Methane reduction tools

They’re all strengths of the European agrifoodtech ecosystem, according to new research from AgFunder and Foodbytes.

As the masses descend on London this week for the Rethink World Agri-Tech and Future Food-Tech conferences, AgFunder and Foodbytes dug into their respective datasets to find new insights on the state of agrifoodtech in Europe.

Foodbytes, the online connection hub for startups, corporates, and investors pioneering sustainable food and agriculture solutions, delved into its database of over 1,500 startups to reveal the findings, while AgFunder cross-referenced Foodbytes’ findings with its related investment data dating back to 2012.

Here – and in the infographics – are the three key takeaways.

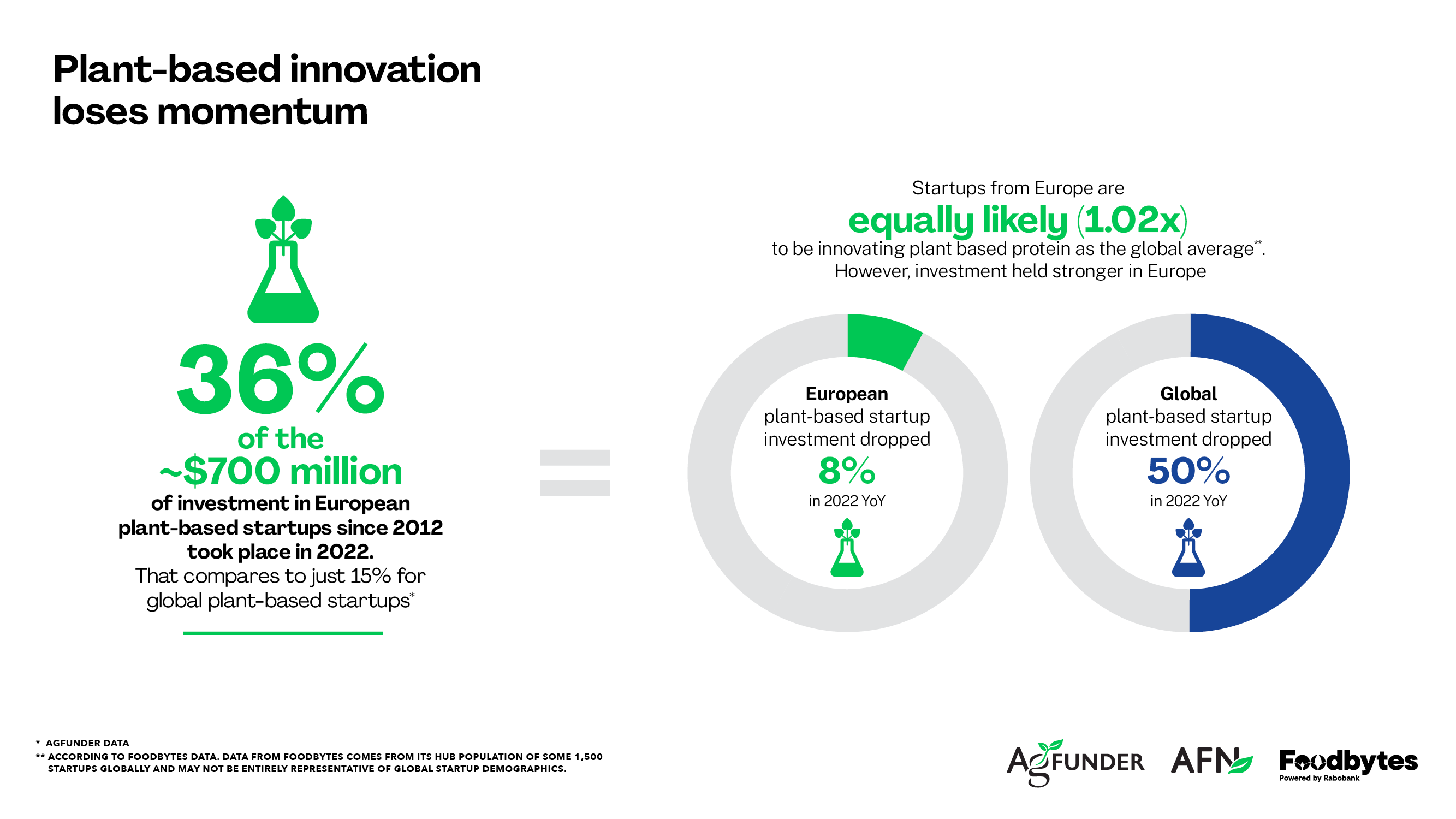

1 – Investment in plant-based startups was more resilient in Europe than globally in 2022

It’s no secret that investor interest in plant-based products has dwindled over the past year or so resulting in startup closures and valuation down rounds across the segment. Much of this is on the back of consumer data showing a decline in consumer interest in plant-based products, which are failing to live up to their hype in taste and nutrition. It’s also a result of an overall pullback in investment across venture capital as markets cool and sky high valuations normalize.

While investment in startups touting “plant-based” solutions halved in 2022 compared to the record-breaking highs of 2021, the European investment in the space appeared to fare slightly better, maintaining momentum, dropping just 8% year-over-year.

Interestingly, 36% of the roughly $700 million of investment in European plant-based startups since 2012 still took place in 2022. That compares to just 15% for plant-based startups across the globe, according to AgFunder data.

According to Foodbytes, 17% of its 650-strong European startup database is in the plant-based category, making it the second most popular category for the region behind farm management software*. One of AgFunder’s most successful plant-based startups is from Europe; Juicy Marbles out of Slovenia.

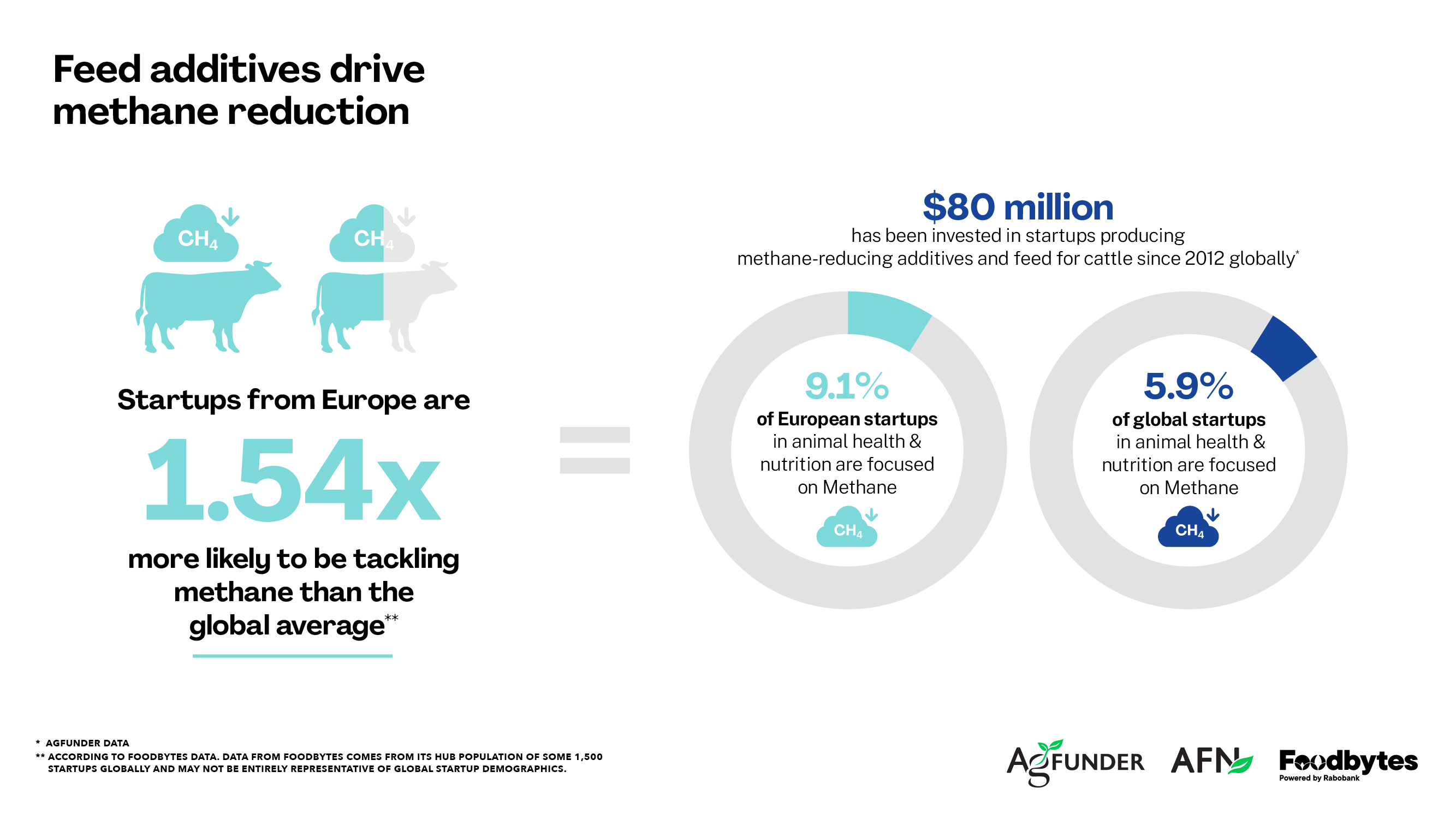

2. Startups from Europe are more likely to be tackling methane emissions from livestock than elsewhere globally

Methane is a potent greenhouse gas that’s responsible for around 30% of the current rise in global temperatures and emissions are “proliferating faster than at any other time since record-keeping began in the 1980s,” according to the United Nations Environment Program (UNEP). Over 40% of methane emissions are estimated to come from the agriculture industry: 32% from animal farming and 8% from rice farming, according to UNEP.

A small but emerging category of agrifoodtech startups is finding ways to reduce the methane emissions of livestock with feed and additives, often using seaweed-based sources that are understood to limit the amount of methane emitted during digestion – typically in the form of burps. And while there are startups globally in this category – including AgFunder portfolio company CH4 Global from Australia as well as ProAgni also from Australia – Foodbytes’ data point to a heavier weighting of startups in Europe.

Agrifoodtech startups from Europe are 1.54 times more likely to be tackling methane emissions in the livestock sector than globally, with Foodbytes identifying 13 European startups out of 41 global startups in this category in its database*.

Startups in this category are still a small piece of the agrifoodtech investment pie, however, taking in just $80 million of investment since 2012.

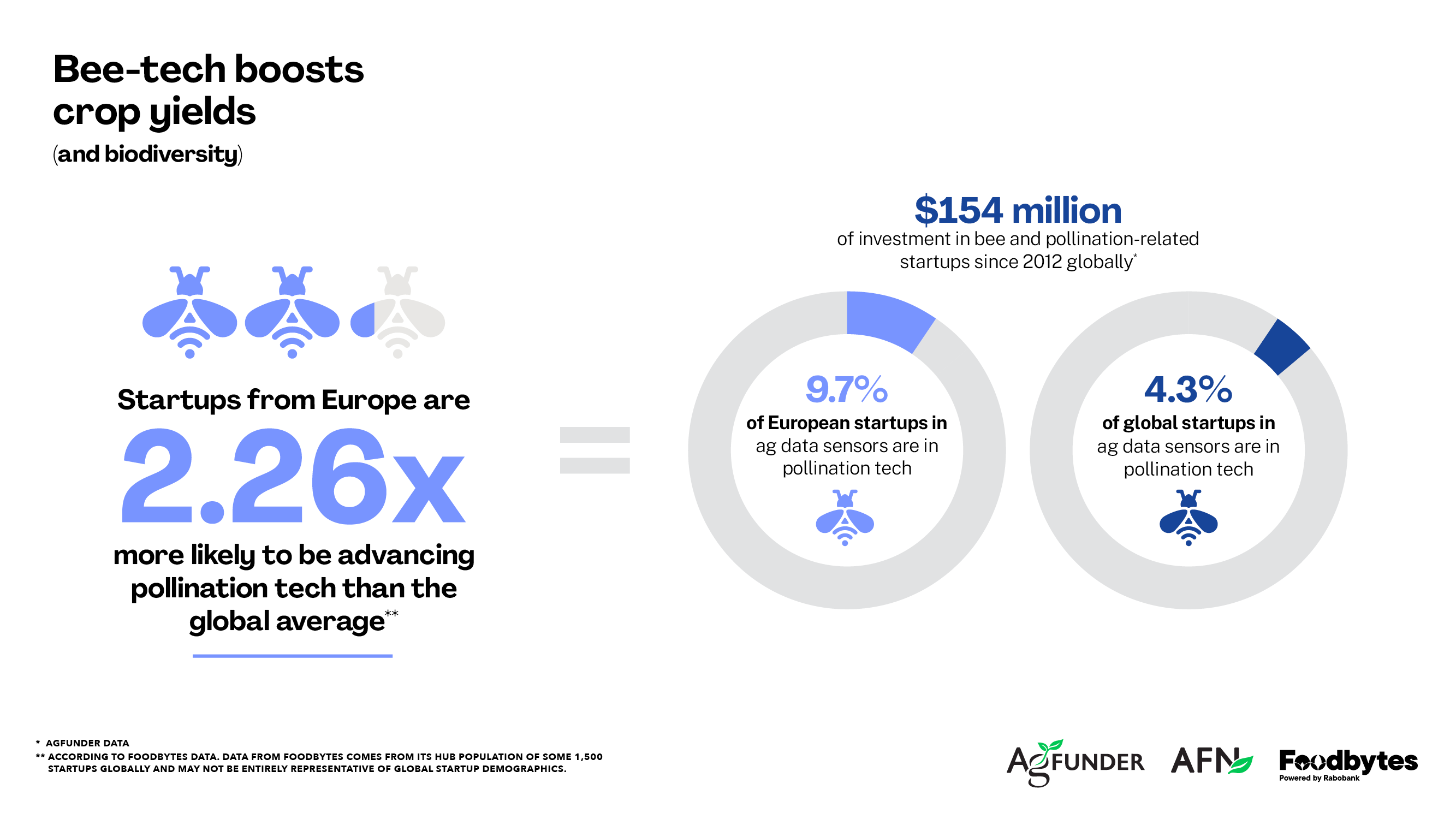

3. European startups are more likely to be advancing pollination and bee-related technologies than globally

Bees and pollinators are an essential part of the crop cycle but modern farming practices, particularly the use of chemical inputs, are negatively impacting their populations. This is not just bad news for growing crops but for biodiversity more broadly.

A range of startups are taking on this challenge with software, sensing and IoT tools to help monitor bee hives and activities to help improve their sustainability, such as BeeHero, or even artificially pollinate crops without bees.

According to Foodbytes data, startups from Europe are 2.26 times more likely to be advancing technologies in this area than the global average. The hub has identified 9 European startups out of 22 in the space globally*.

That said, startups in this category globally have only raised just over $150 million in funding since 2012, so it’s still a nascent category.

*Data from Foodbytes comes from its hub population of more than 1,500 startups globally and may not be entirely representative of global startup demographics.

Make sure your data are counted! Join the Foodbytes hub here and submit your funding deals to be included in AgFunder’s industry-leading investment reports!