Larger fermentation vessels and the resulting economies of scale will drive down the cost of precision fermentation. But technical advances that improve titer, productivity, and yield will be “more powerful levers” to unlocking the potential of the bioeconomy, says a new report from Synonym, a financing and development platform for biomanufacturing infrastructure.

In its latest report into global fermentation capacity based on data from its online ‘Capacitor’ database, Synonym stresses that when it comes to biomanufacturing, size matters.

For example, data from Scaler, Synonym’s techno-economic analysis (TEA) tool enabling startups to project their COGS at commercial scale, shows that for every 2x increase in scale, there is a 1.4x decrease in COGS (cost of goods sold).

However, a 2x increase in titer (the amount of an expressed target molecule relative to the volume of liquid) results in an even bigger (2x) decrease in COGS, notes the report.

“For companies that are still working towards price parity [with animal- or petroleum-derived products], scale alone is not the full answer. Companies at all stages should continue to prioritize activities such as strain improvement and facility and equipment optimization that can ultimately have an outsized impact on cost.”

Continuous processing (enabling smaller, smarter bioreactors with lower capex costs) and higher downstream recovery rates will also be critical to making the numbers add up, added Synonym (high titers aren’t much use if your recovery rates are lousy, for example).

According to Synonym:

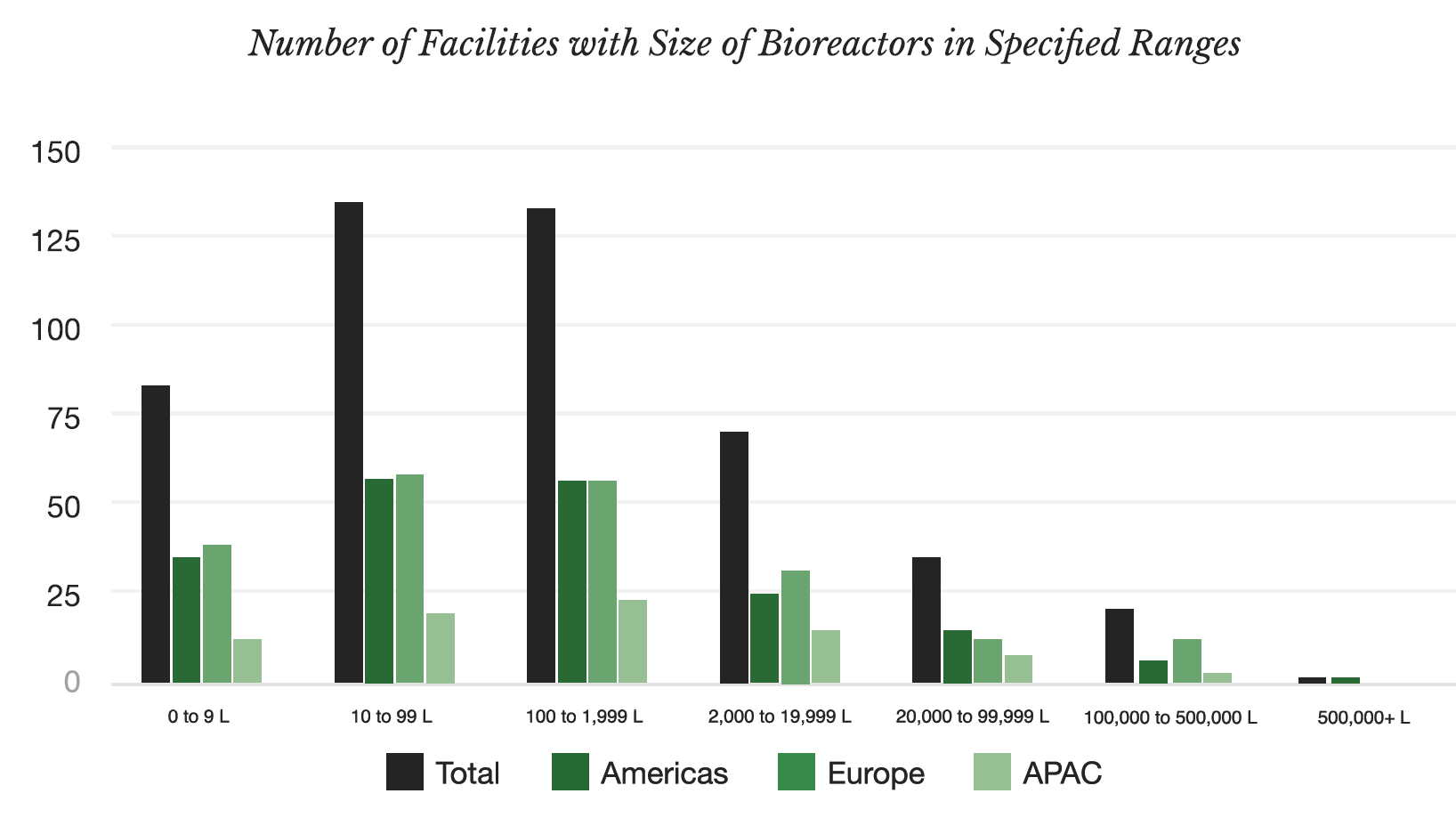

- The Capacitor database now features 246 fermentation facilities in 40+ countries.

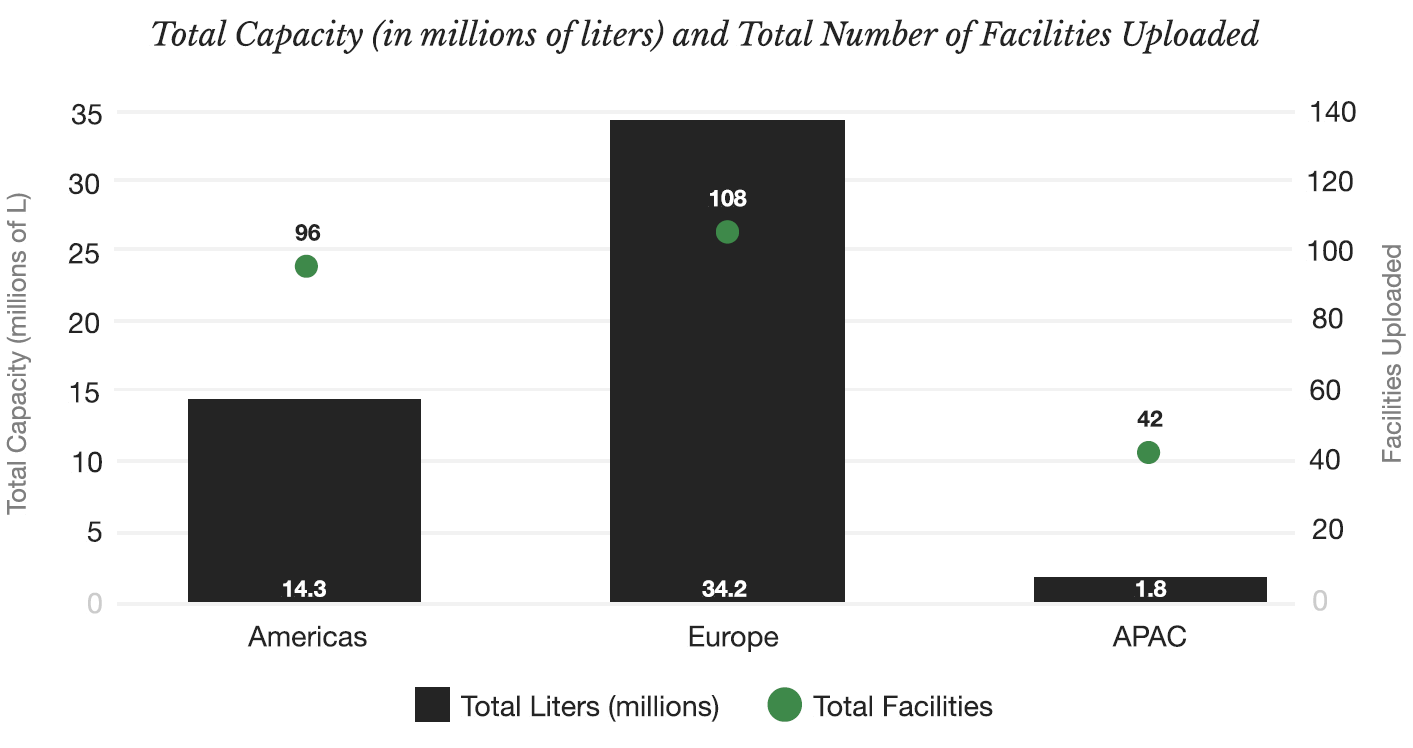

- At 34.2 million liters (vs 14.3m in the Americas and 1.8m in APAC), Europe has the most available capacity that Synonym is aware of (although there is likely a lot in China that is not yet captured in its database, acknowledges the firm).

- Most facilities focus on bench and pilot scale, with comparatively few focusing on demo and commercial scale operations.

- There is a huge gulf between supply and demand for fermentation capacity, especially for larger vessels. “There are only 20 facilities with tanks greater than 100,0000-liters for true commercial operations,” says the report. “If every company using Scaler sought a facility to match their largest modeled capacity need, over 595m liters of capacity would be needed to serve the market, more than 10x the capacity available today on Capacitor.”

- Flexible facility designs that are “compatible with the high performing microbial strains of tomorrow are critical to ensure that equipment investments today don’t become stranded assets tomorrow.”

- Based on aggregated and anonymized Scaler data, “there are many techno-economic scenarios that suggest companies are already capable of producing at the scale and efficiency needed to compete with legacy animal- and petroleum-based products.”

- Capacity in APAC is growing as CDMOs (contract development and manufacturing organizations) such as Singapore’s ScaleUp Bio gain traction.

Fermentation: ‘There’s a catch-22 problem…’

“It’s surprising the number of companies that are still working on products without actually understanding what the unit economics will look like at scale,” Synonym chief investment officer Brentan Alexander told AgFunderNews.

But even if you’re coming to investors armed with a solid technoeconomic analysis, it’s still a challenging time to raise money, he said.

“If you’re a software company and you need to go from 10 users to a billion users, everyone understands the cost structure of doing that because it’s been done. If you’re a precision fermentation company that needs to go from 100 liters to a million liters, we’ve done the work to show what that cost down looks like, but the capital markets do not yet have an understanding of the viability of that pathway.”

As in any new market, he said, “There’s a catch-22 problem. You need large purchase orders to justify the investments into larger facilities. But you often need to have a large facility in order to get those large purchase commitments.”

Right now, there’s interest in new fermentation technologies and products, but volumes are low and most startups are working with small scale contract manufacturers where pricing is high, he said.

As the industry matures, titers will improve and more efficient microbial hosts will enable more products to work at smaller scale, but “in the short term, you’ve got to walk before you can run,” said Alexander. “And at the smaller scale there’s definite differences in the COGS of making very high-value ingredients vs more commoditized ingredients via fermentation. If you start with something highly specialized, the chicken and egg problem is a lot easier to solve.”

What will kickstart the bioeconomy?

But if venture capital providers are reluctant to finance infrastructure projects for unproven tech, what is going to kickstart the bioeconomy?

According to Alexander: “It could be a purchaser who’s willing to make a large purchase to support a large-scale facility on a credit worthy balance sheet. It could be government incentives and government programs that drive investment into these facilities. It could be philanthropic dollars that offset some of the risk profile for more institutional dollars. And then it could be just slowly building your way up.”

In the US, he noted, as part of the Biden Administration’s biotechnology and biomanufacturing initiative, the Department of Defense “has ambitions to put multiple billions of dollars into biomanufacturing over the next five years, although that has to be appropriated by Congress… And then there’s the DoD’s loan programs office that has expressed support for biomanufacturing assets, including for food.”

Governments in Asia-Pacific and the Middle East are also investing in biomanufacturing to ensure food security, he said, noting that US-based animal-free dairy co Change Foods is building a precision fermentation facility in Abu Dhabi with the support of the Ministry of Economy of the UAE under the NextGen FDI initiative (designed to help high-tech businesses launch and scale from the UAE).

Finally, environmental reporting requirements may prompt more large food companies to invest in bio-based alternatives to animal- and petroleum-derived products in order to lower greenhouse gas emissions, he said: “In California by the end of 2027, all firms with over a billion dollars in revenue will have to have to report scope three emissions. There’s a lot of tailwind that will drive demand into this industry, which is what’s necessary to drive the capital.”

Commitments from strategics

If you’re a precision fermentation startup making food ingredients, a clear commitment from a strategic buyer interested in purchasing your product will be critical to raise capital, he said.

“The terms of that purchase agreement are really important. If it’s a durable purchase agreement with a credit worthy counter party, that will open the door to a lot of institutional capital sources that are used to doing more project finance transactions. But in food, those are hard to come by.”

As for bank debt, he said, “It’s really difficult to get debt on to anything that is not backstopped by an offtake agreement, which is coterminous with the term of the debt. So if you try to get seven year debt, you need someone who says they’re going to buy your stuff for seven years.”

Down the road, if and when technologies have been proven, he said, things could look very different, although debt financing would likely still be contingent upon “successful implementation and proven durability…

“I would like to say one or two years would be enough,” said Alexander, “but we’re probably looking at four to five years’ worth of durable market demand before true institutional capital at the 6-7% debt rate is willing to come into this space.”

Capacity under development

Synonym has recently launched a new feature enabling providers to tag facilities as ‘under development,’ which helps users to identify capacity that will be coming online in the next few years, including Liberation Labs’ 600,000-L facility in Indiana and ScaleUp Bio’s new facilities in Singapore.

In Europe, Belgium-based Bio Base Europe Pilot Plant has also been expanding capacity to help startups road-test their technology at a larger scale.

Speaking to AgFunderNews at the Asia-Pacific Agri-Food Innovation Summit in Singapore last week, head of business operations Hendrik Waegeman explained: “About two or three years ago we were fully booked, so we tripled our capacity… but then we hit a bit of a recession. As a result, we now have capacity available and we have shorter lead times, typically three, four months, which is a healthy situation, actually.

“We’ve grown the organization in 10 years from three people to 180, with many coming from Ghent University, which is a very good university when it comes to bioengineering and it’s close to our facility. We’ve also got people in-house working on continuous fermentation. I’d say about 50% of our work is on alternative proteins, but we also work on enzymes, bio-pesticides, and low caloric sweeteners.”

Michele Stansfield, founder and CEO at Australian continuous fermentation specialist Cauldron, meanwhile, is on a mission to build Asia-Pacific’s largest network of “smaller, smarter” precision fermentation facilities as a CDMO (contract development and manufacturing organization).

She told us: “In this market there aren’t going to be too many $200 million or $300 million raises for precision fermentation startups to build their own plants. To me, that’s a capital-intensive distraction; these companies should be asset-light. It makes much more sense for us to build smaller, smarter, cheaper facilities.”

Speaking to AgFunderNews at the same event, Tao Zhang at alt protein investor Dao Foods International added: “I would say China definitely has a competitive advantage as far as fermentation capacity is concerned. For some of the international companies in biomass or precision fermentation, my advice is, take advantage of what China can offer so you can lower costs, achieve price parity, and make products that are more interesting to mainstream consumers.”

Download the Synonym report here.