Data Snapshot is a regular AFN feature in which we analyze agrifoodtech market investment data provided by our parent company, AgFunder. Click here for more research from AgFunder and sign up to our newsletters to receive alerts about new research reports.

Premium food and beverage consumer goods remained an active investment category in India’s agrifood scene last year, despite experiencing a dip in funding.

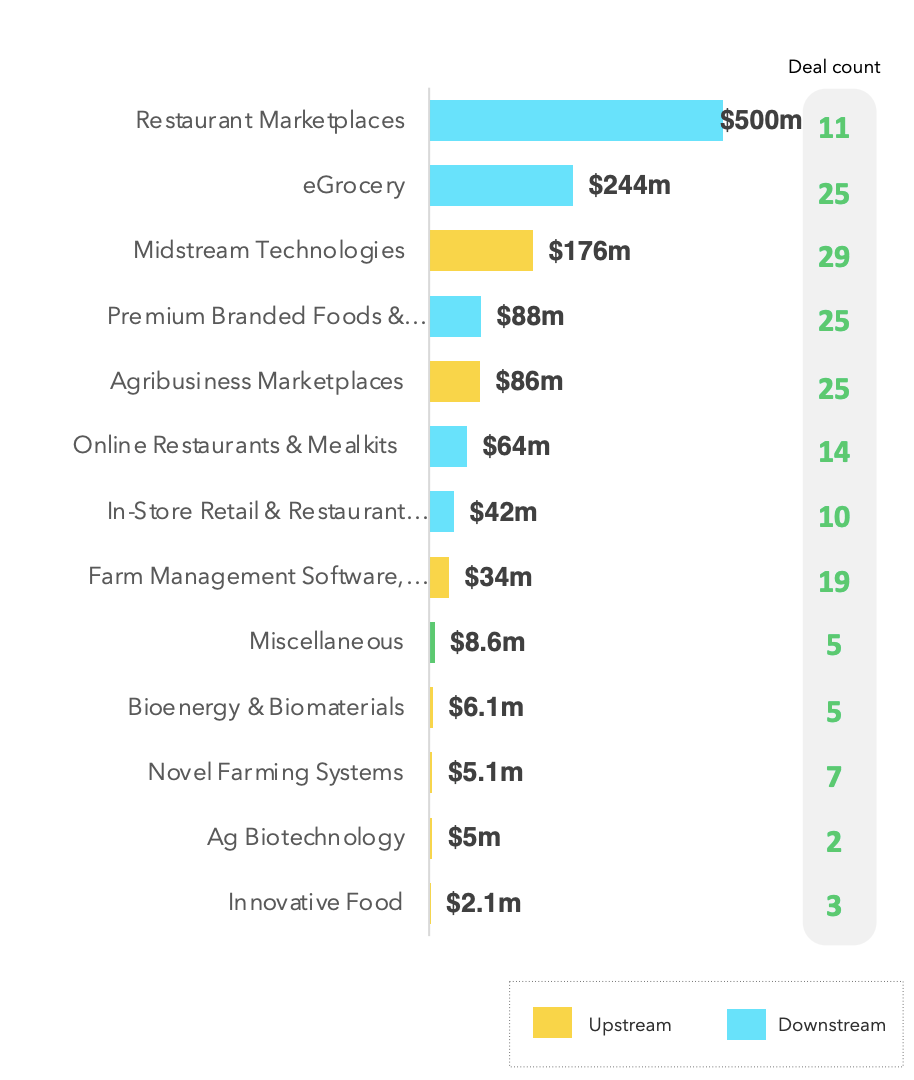

Indian startups in the Premium Branded Foods & Restaurants category raised $88 million in FY2021, down from $168 million in FY2020, according to data from AgFunder’s India 2021 Agrifood Startup Investment Report. Even so, it was the joint-second most active category for the year in terms of deal volume, tying with eGrocery and Agribusiness Marketplaces.

The category also raised the largest number of seed-stage deals with 17 total, beating out the other two categories’ 15.

India’s most active investment categories, FY2020-2021

Premium Branded Foods & Restaurants is a special category AgFunder includes in its India and China reports, to account for premium food experience offerings that play a key role in consumption upgrade in both of these rapidly growing emerging economies. These offerings include things such as ‘higher-end’ product design, formulation, and packaging, as well as thematic restaurants – often with a tech aspect, such as automated serving or app-based ordering.

In China, too, Premium Branded Foods & Restaurants represented the second largest category in terms of dollars invested in the last year for which full data is available (2020).

It was the top category by deals done, accounting for almost half of all agrifoodtech funding transactions over the 12-month period. That represented a big jump from 37% of total deals in 2019, pointing perhaps to the relative ease to start companies and raise capital in this category; in contrast to India, China — with its “zero-Covid” policy initiating a strict closure of international borders — was able to keep infection numbers low and lockdowns and shelter-in-place orders limited to select cities. This meant the domestic economy was largely able to operate as normal.

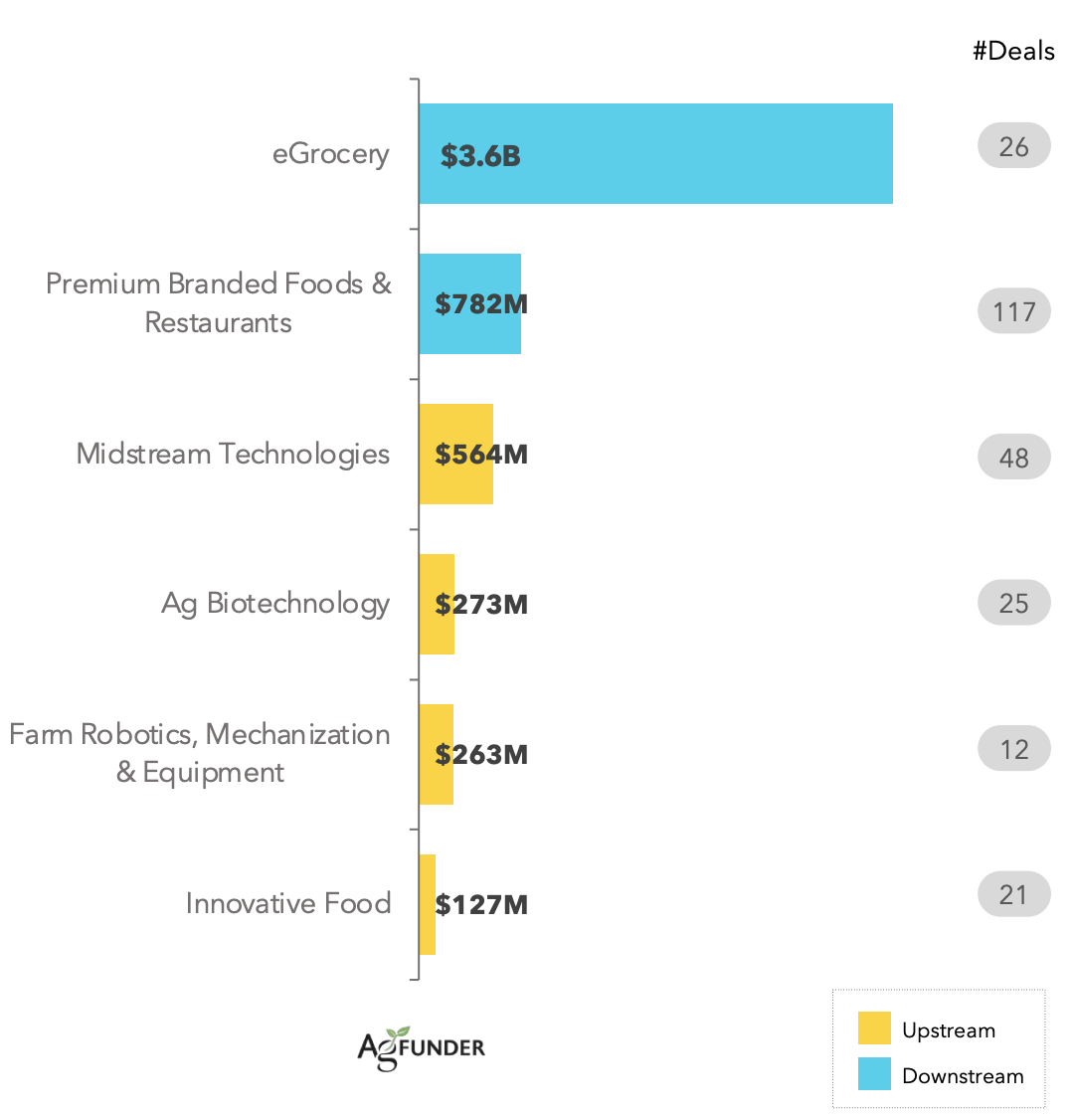

China’s most active investment categories, FY2020

Why the decrease?

The economic slowdown brought on by the Covid-19 pandemic is at least partly responsible for the dip in overall demand for, and investment in, consumer-facing categories like Premium Branded Foods & Restaurants.

India, which is home to more almost 1.4 billion people, experienced one of the deepest recessions of any major economy during the height of the pandemic. Its second wave of infections, in 2021, was particularly brutal as store and restaurant closings resulted in lost jobs and stunted overall consumer demand.

There was a silver lining for the category, however, as Covid-19 drove many consumers to seek out premium food products — which they deemed to be of higher quality and safer than standard options — for the first time.

Top Premium Branded Foods & Restaurants deals

In the last few years, discretionary spending among India’s middle class has risen, paving the way for more premium-branded food and beverage offerings.

Top deals for such brands in FY2021 include:

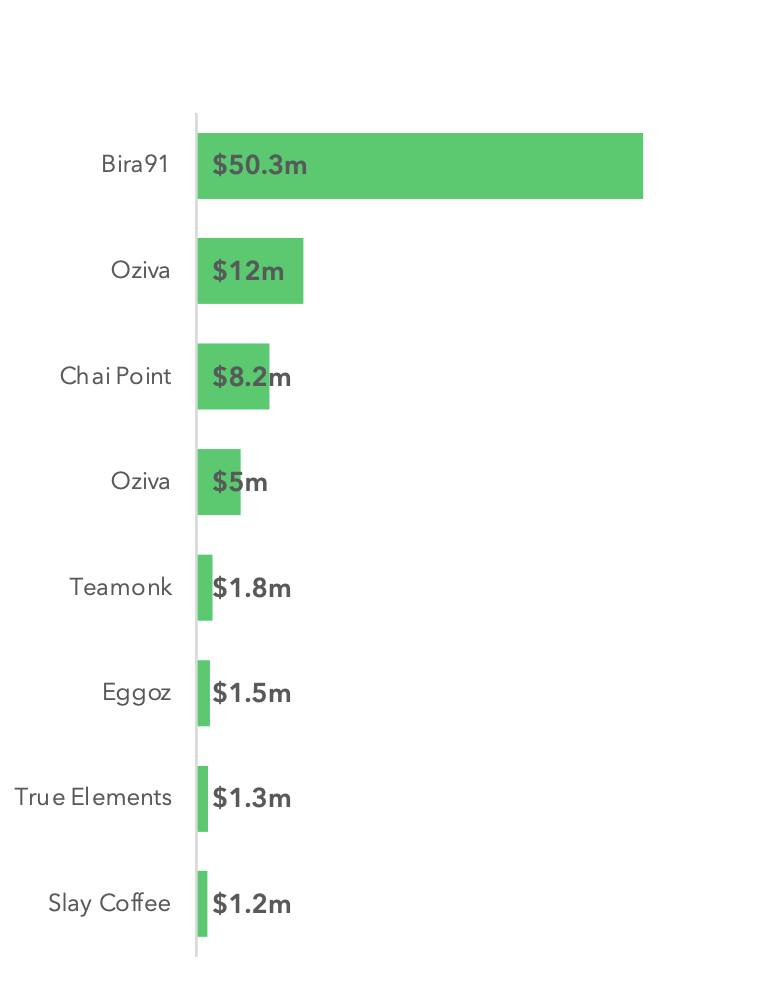

- Beer brand Bira 91 raised a $50.3 million Series B from Sequoia Capital, Kirin Holdings, and Sofina.

- Plant-based nutrition startup Oziva raised a $12 million Series B from Eight Roads Ventures, F-Prime Capital Partners, and Matrix Partners. Oziva also raised a $5 million Series A from Matrix Partners and Titan Capital.

- Premium tea and snacks company Chai Point raised a $8.2 million Series C from Eight Roads Ventures, Saama Capital, and DSG Consumer Partners.

- Farm-sourced egg brand Eggoz raised a $1.5 million Seed round from Avaana Capital and Rebright Partners.

India’s top Premium Branded Foods & Restaurant Deals, FY2020-2021

The report also makes mention of multiple packaged goods companies that continued to raise on the back of consumer demand for ‘healthy’ foods. They include breakfast snack brand True Elements, children’s snack brand Timios, vitamin supplements maker Power Gummy, dietary supplements brand Nutrova, and nutritional foods brand Habbit Health.

In China, Covid-19 helped concentrate capital on more established brands; those making ‘healthful’ claims, in particular, continued to attract investment.

Probiotic yogurt brand Simple Love raised Series A funding, while cereals brands HON Life and Wangbaobao received $21.8 million and $14.5 million respectively for their Series B rounds.

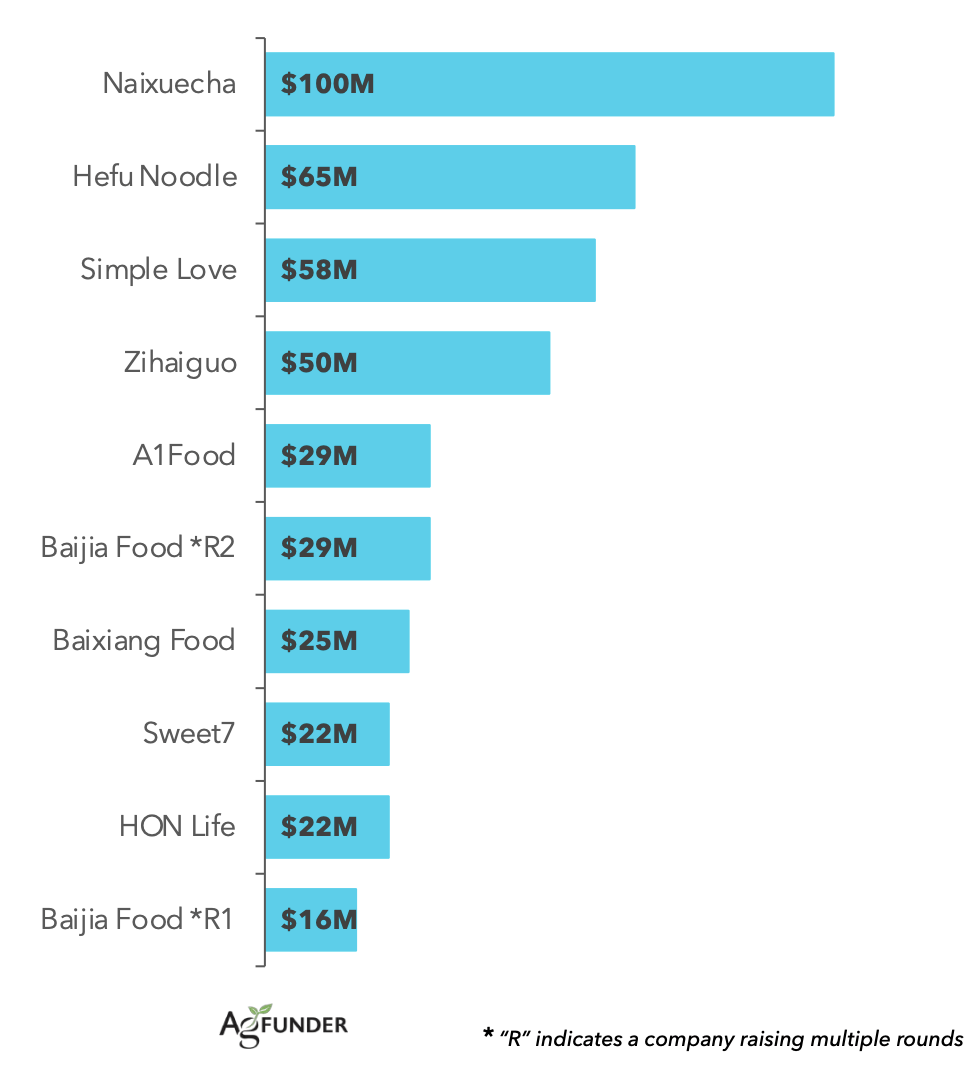

China’s top Premium Branded Foods & Restaurant Deals, FY2020