As managing director and head of FMC Ventures, Mark S. Brooks combines his experience as a climatologist, entrepreneur, and venture investor to back game-changing agtech innovations that address the climate crisis.

The views expressed in this article are the author’s own and do not necessarily represent those of AgFunderNews.

Agriculture feeds the world while holding the key to a healthier planet in an era of climate uncertainty.

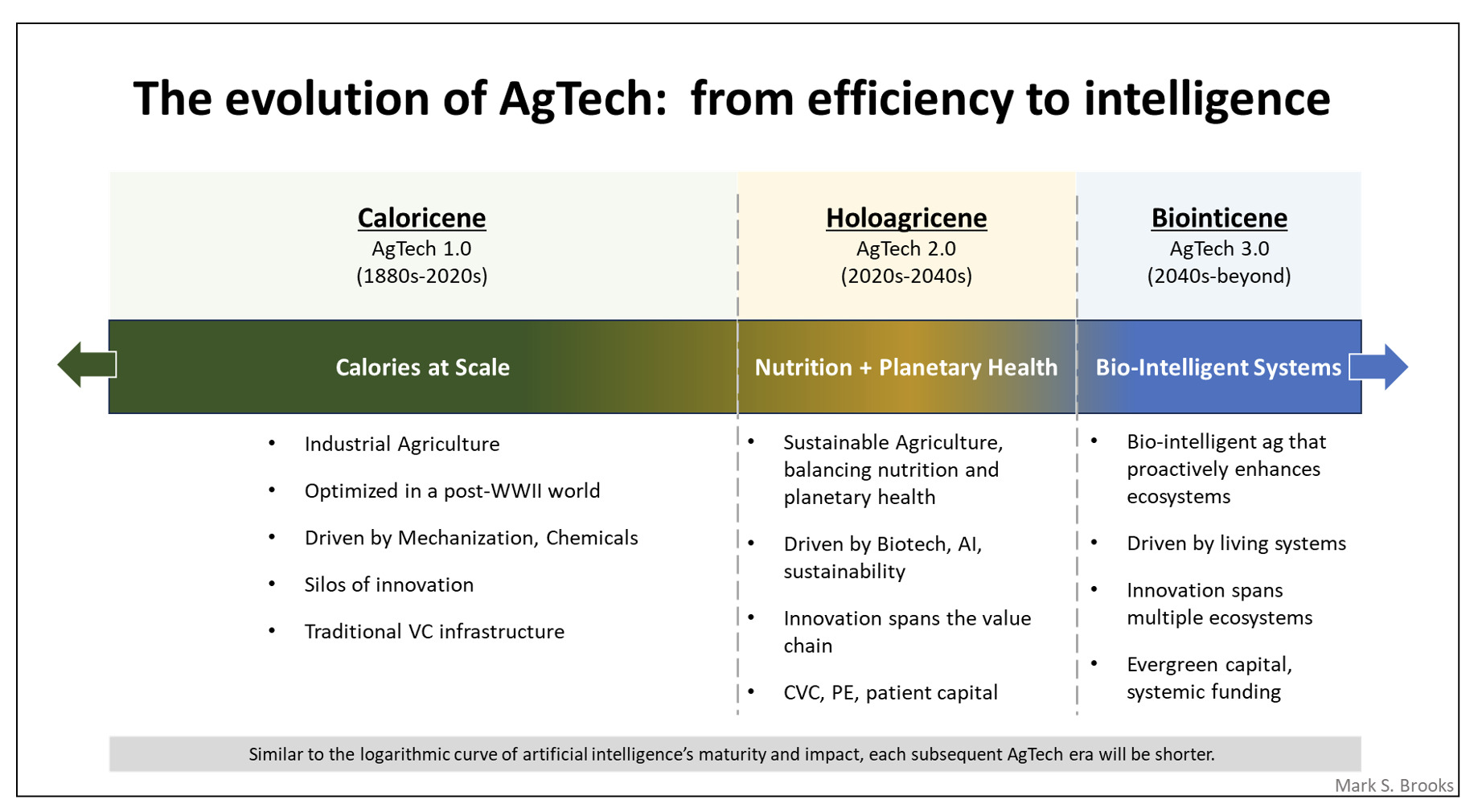

The pace and type of innovation in agriculture has gotten us to where we are today: an optimized food system that delivers calories at scale. This is agtech 1.0, or what I affectionately call “the Caloricene,” an epoch centered on caloric efficiency that spans roughly the late 1800s through today. Its optimization really came into view during the economic boom after WWII.

Agtech 2.0 begins now, where the mission evolves to be about delivering nutrition and planetary health outcomes in addition to calories. This is driven by consumer demand for nutrition, sustainable practices, carbon-aware food systems, biotech in seeds and crop protection, and the use of generative AI in ways we’ve yet to imagine. I call this era “the Holoagricene,” where agriculture feeds people and heals the planet.

Looking farther ahead to the 2040s and beyond, agtech 3.0 could mark the era of bio-intelligence. This era will move beyond simple control or optimization and embrace living, proactive ecosystems that produce food while actively enhancing the environment. The “biointicene” will be agriculture’s ultimate evolution. Different from letting nature simply do its thing, agtech 3.0 is about harnessing and enhancing nature with intentional design, optimization, and integration of technology and human intervention.

Innovation is the path to get us from here to there. But innovation needs funding. Venture capital has allocated more than $40 billion to agtech over the last decade. However, few exits have occurred, and even fewer category-shaking companies have emerged.

Think of agtech’s evolution as a timeline where each era demands different funding models. This brings us to a defining question: Is venture capital the right vehicle to fund agtech 2.0?

The VC mismatch

The roots of venture capital are found in Silicon Valley. It was created as a financial instrument to fill a white space banks, lenders, and wealthy individuals could not fill themselves. The original intent was to capitalize high-growth, high-risk, technology startups that could exit quickly. A 10x return was typically targeted, knowing that many investments would ultimately fail with no return. Venture capital is the reason we have companies like Apple, Google, Amazon, Tesla, Uber, Paypal, and many others.

But when was the last time you heard of a high-growth, fast-exit, high-valuation agtech company? In contrast to the origins of venture capital, agtech is slow-growth, has long-time-to-exit time horizons, and low-exit valuations. In other words, agriculture demands patience. The same funding models that birthed Google and Uber will not feed the world or save it.

M&A has been slow

M&A, a critical engine for scaling startups and attracting new capital, is largely absent in agtech. Since the ag market downturn in 2022/2023 and the spike in interest rates, all the corporate ag strategics have been dealing with a challenging balance sheet. This has resulted in restructurings, many of which are still in progress. The real cost? Startups stall, innovation stagnates, and agtech risks losing its pioneers.

The new capital stack: emerging solutions

Agtech-focussed VC funds are contracting due to the lack of exits within the typical 10-year venture capital lifecycle. What’s missing is more patient capital with a 10- 15-year-plus horizon. Fortunately, this profile is increasingly active in agtech, which is important to keep capital flowing.

This new capital stack includes:

Sustainability funds: doing well by doing good. New sustainability-oriented funds—often grouped under the banner of “climate tech” funds—are reshaping how capital flows into transformative industries. These funds bring a dual mandate: maximize impact and deliver strong financial returns. While agtech may not be their sole focus, their patient timelines, mission-driven ethos, and appetite for systemic change make them invaluable allies. Unlike traditional VC, these funds aren’t chasing quick exits or sky-high valuations. Instead, they are guided by a bigger vision: healing the planet while generating profits.

Corporate venture capital (CVC): strategic patience. Agrifood corporate VCs are stepping up to play a more critical role. The parent companies of CVCs have incredible market power via the channel, world class R&D capabilities, regulatory expertise, and a global footprint. For startups, CVCs offer something traditional VC cannot: strategic alignment and a clear bridge to commercialization. Corporates are keen to accelerate innovation for their pipelines and CVCs are one of the few tools at their command. This playbook is beginning to mirror pharma: outsource discovery to startups, then scale promising innovations internally. It’s a win-win for startups and corporates.

Private equity (PE): new exits. As startups struggle to raise their next round and venture investors aspire to exits, the private equity (PE) model is stepping in. PE can roll up multiple companies to achieve economies of scale and realize synergistic benefits. It can also accelerate scale-up and profitability by acquiring, optimizing, and flipping companies. For agtech, PE brings liquidity, scale, and discipline—trends that have transformed other industries and are now making their mark here.

Open-ended, patient, evergreen capital: playing the long game. Building the Holoagricene demands patience. Instead of the traditional VC cycle of deploying and harvesting within 10 years, we need longer-term, evergreen capital that recycles returns into the next breakthrough while providing dividends to LPs. These open-ended fund models have no end date or fixed capital benchmark, ensuring innovation doesn’t stall as we move towards the future.

What does this mean for agtech innovation?

High interest rates and tighter credit markets have made funding harder to come by. For now, startups with clear commercial traction will attract what capital remains. This is accelerating a shift to fewer but larger agtech deals. But this is a short-term reality; as rates fall and exits return, early-stage funding will rebound. Will we be ready with the right capital stack?

What starts slow grows quietly and holds the power to shape our survival and our future—if only we have the patience to nurture it. If we get this right, we feed the world and heal the planet.

Agtech 2.0, the Holoagricene, isn’t just a vision—it’s a necessity, and it’s already underway. To fund it, we need patient, evergreen, strategic capital with strong CVCs. The question isn’t whether agriculture will evolve. The question is whether investors will evolve to fund it—or let the opportunity pass while chasing faster, shinier returns. Agriculture can’t wait, and neither should we.