Data snapshot is a regular AgFunderNews feature in which we analyze agrifoodtech market investment data provided by our parent company, AgFunder.

Click here for more research from AgFunder and sign up to our newsletters to receive alerts about new research reports.

Venture capital money allocated directly to agrifood only accounts for about 2% of the entire global investment pool, says Roberto Viton at Valoral Advisors, who has been tracking the agrifood funding landscape for more than 10 years.

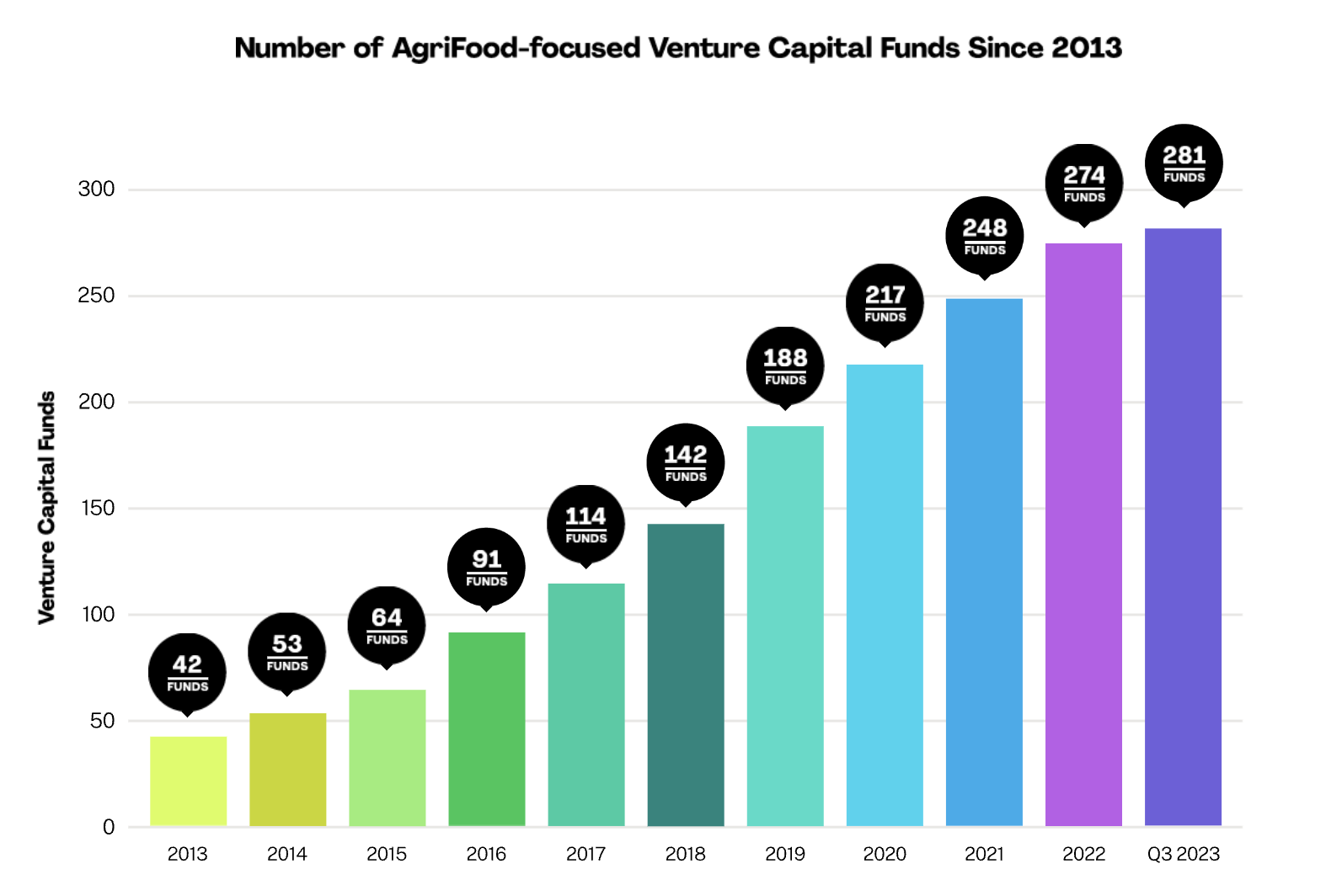

And while the number of agrifood-focused VC funds has grown worldwide from a mere 42 in 2013 to more than 280 as of the third quarter of 2023, that growth has slowed in the last few years.

“Growth was possible because we were starting from very low levels’,” Viton says of the rise in agrifood funds over the last decade.

Putting that growth in context, he says, “Typically when you talk to an institutional investor, like a pension fund, and you ask how much money they have directly invested in [agrifoodtech], they will tell you anything between zero and 2%. Or maybe 3% if they include forestry.

Like others, he also believes 2024 is going to be another tough road for agrifood.

“This year is going to be the toughest one in my view,” he says. “More companies will really struggle and many companies will close. But this will evolve. I see a lot of conversations between startup founders to merge businesses, to consolidate. I think that’s what’s going to happen next.”

More efficient food production requires more capital

According to data provided for AgFunder’s 10-year anniversary special report, the agrifood-focused VC funds have grown in number each year for the last 10 years.

Viton cites four factors that have pushed the number up:

- Supply, such as limited planetary resources and the impacts of climate change

- Demand, including population growth and changing diets

- Geopolitical and economic factors such as war and inflation

- Technological breakthroughs across industries

“Over the last 10 or 20 years, we’ve have the challenge of producing more food in a more efficient and sustainable way while facing a number of challenges,” Viton tells AgFunderNews. “We need to make [food production] more resilient, we need to build supply chains, and we need to bring technology to fill the gaps that we have. All of that calls for capital.”

But, “All this growth was possible because we were starting from very low levels,” he adds. “Even today, I would say we’re in the early innings.”

He believes the reason more capital has flowed into the agrifood space is “attractive potential returns.” Larger asset managers are developing new strategies in the space alongside specialized managers and banks, he says.

2024 will be ‘the toughest’

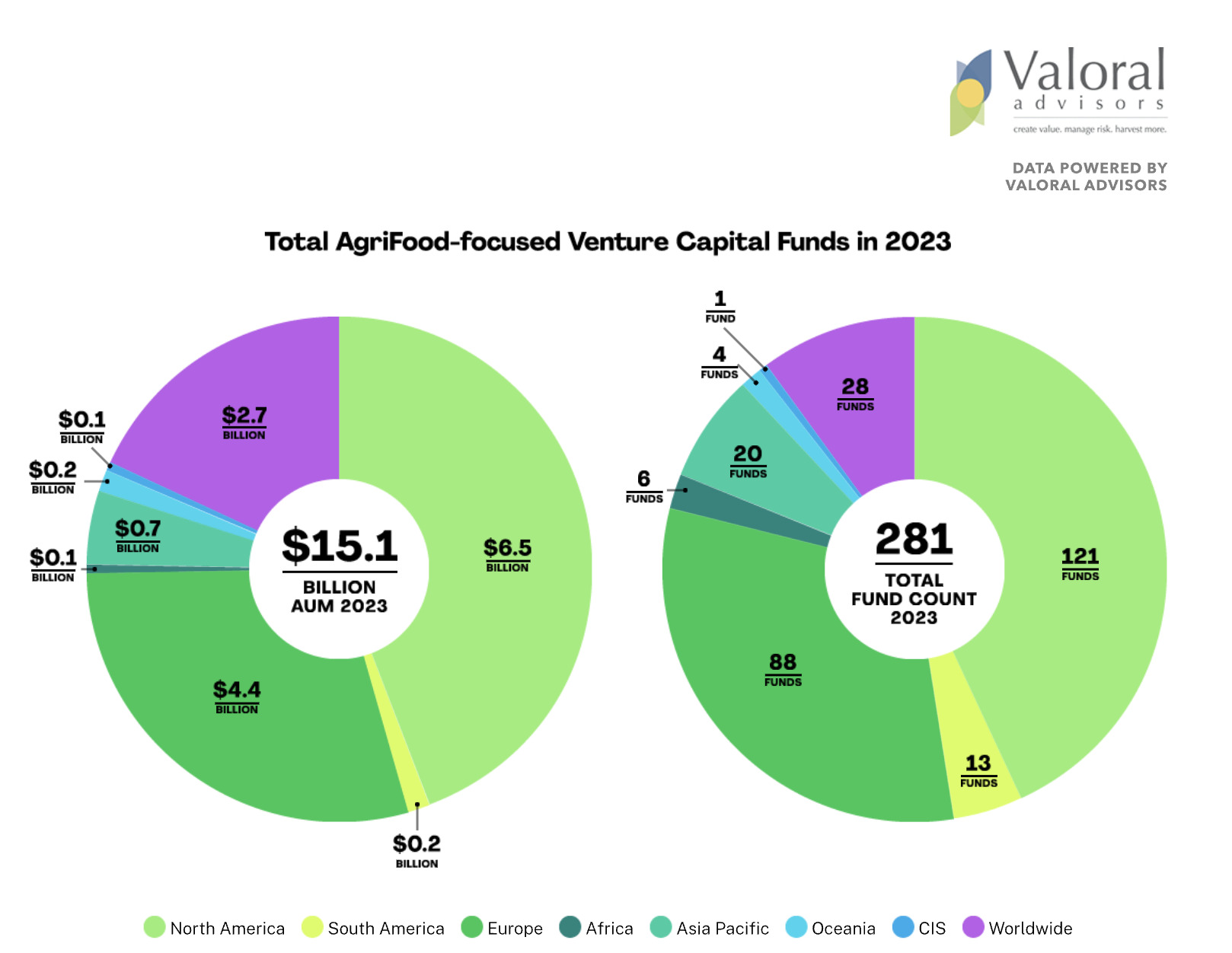

Total agrifood-focused venture capital funds in 2023 had $15.1 billion in assets under management (AUM), which include farmland, private equity, venture capital, private debt, listed equities and commodities.

A closer look at Valoral’s data for 2023 reveals that, while the number of agrifoodtech VC funds was up from the previous year, it was only a 2.5% growth rate.

Compare this with the 32% increase in the number of funds from 2018 to 2019, or even the more modest 15% increase from 2019 to 2020. In fact, since 2019, the number of funds has increased but at a noticeably slower pace.

“If you’re a new fund manager, it was really hard in the last few years,” says Viton. “If you look at the long term, I’m sure that we will see more investment flows in this space.

“But when you start zooming into the specific assets, strategies and geographies, a lot of funds in the last few years struggled to raise money. When you look at who did better [over this timeframe], it was usually the more established asset managers because they already have an LP base, they have a track record.”

The bulk of agrifood’s AUM came from North America ($6.5 billion) and Europe ($4.4 billion).

“Most of the capital or the investors are in the US and Europe, and those are the two markets which are more advanced in terms of innovation and talent,” says Viton. “It’s not surprising that you keep seeing new funds and more investments there.”

At present, Viton says he rarely finds companies in these regions doing more than about $2 million in revenues.

“The obvious evolution should be to see more activity in Latam, Africa and Asia-Pacific,” he adds. “But it’s going to take time.”