Francisco Jardim is founding partner, and Marcella Falcão is associate, at SP Ventures, São Paulo, Brazil. The views expressed in this guest commentary are the authors’ own and do not necessarily reflect those of AFN.

Last month, SP Ventures announced its first ‘climate tech’ deal: leading Moss.Earth’s Series A round in a $10 million co-investment syndicate including Acre Venture Partners, Celo, The Craftory, and Jive Investments.

Climate tech is quickly becoming a mainstream venture investment category worldwide, but is still relatively misunderstood. What follows is a summary describing our understanding of this exciting new space.

Let’s start with the basics. Climate tech encompasses a broad range of segments representing the challenge of decarbonizing the global economy, with many countries and companies having set specific goals to reach net-zero greenhouse gas (GHG) emissions by 2050 while preparing businesses for the adverse effects of climate change.

Climate tech’s applications can be grouped into three broad sector-agnostic categories:

- Direct emissions mitigation or sequestration

- Adaptation to the impacts of climate change

- Enhancement of our ‘climate understanding’

According to PwC‘s “State of Climate Tech 2021” report:

- A total of $222 billion was invested in climate tech between 2013 and H1 2021, across 3,000-plus startups;

- $87.5 billion was invested between H2 2020 and H1 2021 alone, representing 210% year-on-year growth;

- Over 6,000 unique climate tech investors have put money into the sector since 2013, ranging from VCs, private equity firms, corporate VCs, angels, philanthropists, and governments.

The US remained the leading geography for climate tech investments over the 12 month period, accounting for nearly 65% of all funding in the sector. China saw $9 billion in climate tech investments during the same timeframe, while Europe totaled $18.3 billion, driven by a 500% increase in the mobility and transport vertical.

Latin America is still not among the top destinations for climate tech capital, despite the region’s huge potential.

Brazil may have the largest potential carbon reserves of any country in the world. Let’s compare this potential with the present-day petroleum industry: Saudi Arabia, the world’s leading exporter of crude oil, has the 49th highest per capita income in the world at about $20,000, according to an analysis by asset manager Schroders. Brazil is 84th in the same table, with less than half the per capita income. But factoring in the annual benefit of Brazil’s forests to its economy at theoretical price — Schroders uses EU carbon credit prices and forestry company valuations — Brazil’s income per capita would rise to about $25,000.

There’s an opportunity — and an urgency — to shift capital towards new solutions and geographies with this kind of untapped climate impact potential: in other words, allocations that will generate greater carbon reductions per dollar invested.

Of the 15 segments that PwC identifies within climate tech, the top five — solar power, wind power, food waste technology, green hydrogen production, and alternative food and low GHG proteins — represent over 80% of future emissions reduction potential.

However, they received just 25% of total climate tech investment between 2013 and H1 2021.

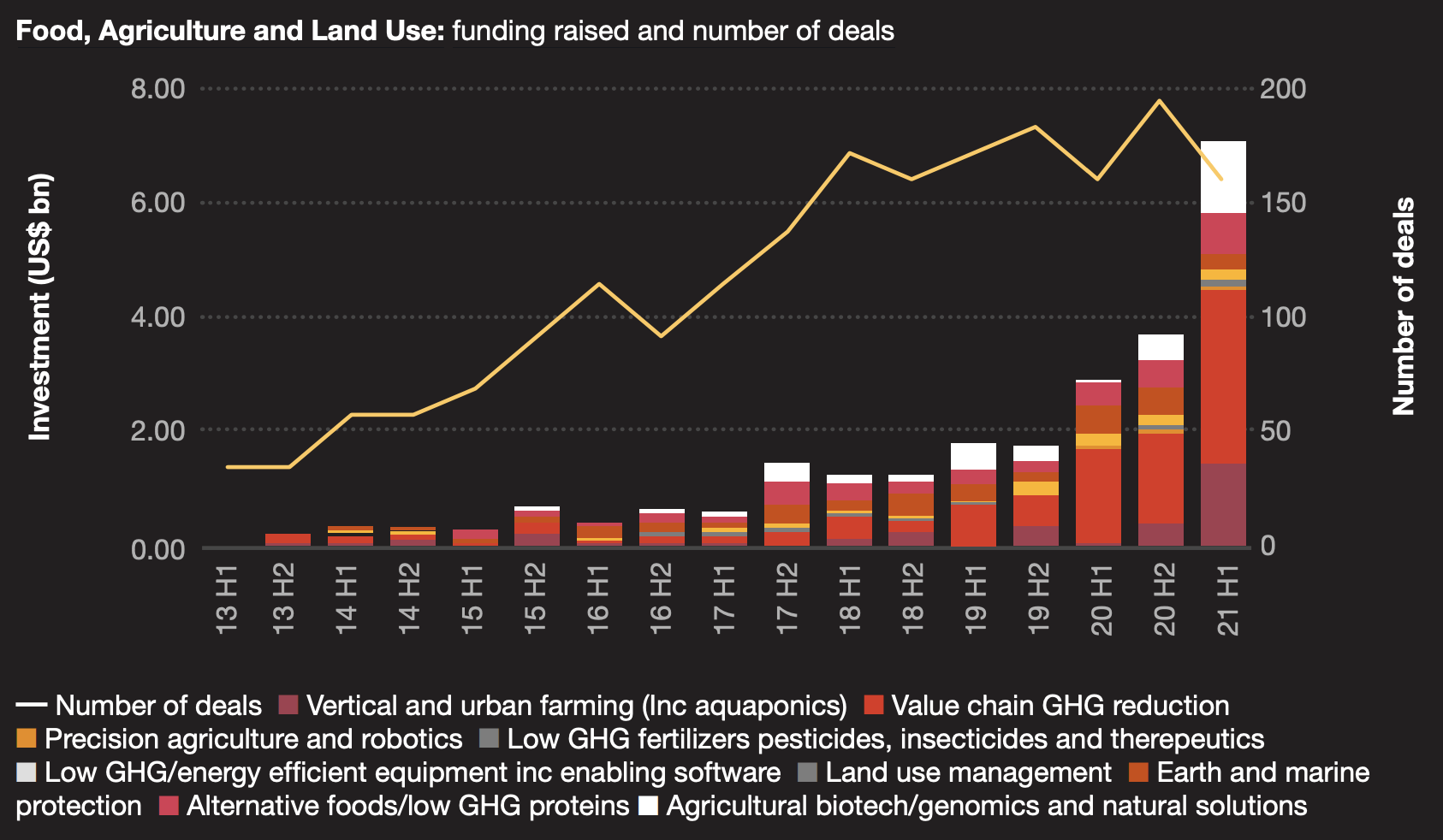

PwC’s report says that technologies addressing food, agriculture, and land use — which together are responsible for a fifth of global GHG emissions — have received $10.7 billion in investment capital between H2 2021 and H1 2021, representing year-on-year growth of 132%.

Food, ag, and land use also provides 13 of the 78 climate tech unicorn companies identified in the report. Digging down, these unicorns cover:

- Alternative foods and low GHG proteins (five companies)

- Value chain GHG reduction (x3)

- Precision agriculture and robotics (x2)

- Vertical and urban farming (x2)

- Agricultural biotech and genomics (x1)

Grabbing the opportunity

Based on these key drivers and our core beliefs, we are certain that agrifood will be the hero of the climate crisis. This is one of those moments in history where an extraordinary investment opportunity intersects with the most pressing challenge of a generation. Quite literally, this is about generating outstanding financial returns while saving the planet for us and those that follow.

Below are some straightforward ways in which agrifoodtech startups are already saving the day:

- Agfintech – through data science and aerial imagery, firms can certify and issue debt for farmers with sustainable agricultural practices, offering a “greenium” of low interest rates.

- Digitalization to increase productivity per hectare – reducing pressure to expand agricultural land frontiers into forests while optimizing use of inputs (fertilizers, crop protection, water) which have direct and indirect GHG impacts.

- Precision ag and biotech – optimization and substitution of inputs preserves water and reduces agrochemical use (these inputs can have a huge carbon footprint, while water management is key in climate uncertainty.)

- Key infrastructure to build and scale carbon markets – credits originated through productivity surges in agriculture or livestock, to fund farmers’ transition toward a lower-carbon agriculture.

- Surplus food – marketplace platforms that connect buyers and sellers of surplus or near-to-expire food.

Climate tech is surging in Latin America and will become one of the most liquid VC investment categories in the coming years. We believe that the more stakeholders get engaged in this ecosystem, the higher the likelihood that we will figure out innovative solutions to mitigate the worst impacts of climate change and reach net-zero emissions by 2050.