Editor’s note: Seana Day is a partner at Culterra Capital and based in the US. She has 20-plus years of investment, M&A, and strategy experience in agrifoodtech. Her analyses on the sector are regularly used by participants in the space to understand the continuously evolving landscape.

The views expressed in this guest article are the authors’ own and do not necessarily represent those of AFN.

In part 1 of this series, I reflected on the last decade of investment in agtech and shared my long-held belief that there is still a big, underserved tech-driven opportunity for many founders and investors.

Over the past 10-plus years I’ve seen farmtech innovation opportunities progressing, from inputs (biologicals, genomics, etc.) and machinery (robotics and automation). Now, in the proverbial search for “the next big thing” across the coming decade of agtech investing, I believe focusing on the ag service category will create the next wave of value for farmers (and investors).

In particular, my investment lens will include a heightened emphasis on efficiency tools for farmers and their service providers. Today, the gap in digital capabilities (beyond excel) around accounting, finance, and workforce development continue to exacerbate the ag industry’s administrative and reporting headaches. Beyond headaches, real cost and productivity loss are creating a catalyst for ag to take a big leap forward in its digitization journey.

When the ‘heat map’ lights up opportunity

I’ve often referred to the landscapes I publish as “heat maps” of activity, innovation, and investment. It was this idea that inspired me to take a deeper look into ag services. The thesis came into focus when I compared investment over the last decade in inputs and machinery, relative to services.

- For perspective, let’s just look at one sliver of inputs investment. AgFunder estimates startups developing crop inputs (biofertilizers, biopesticides, and biostimulants, among others) collectively raised about $892 million worldwide from investors in 2021.

- Similarly for machinery and equipment, about $900 million was raised worldwide by 130 companies in 2021.

- Between 2018 and 2021, venture-backed input companies raised $5.3 billion across 510 deals, and machinery and equipment automation companies raised $1.5 billion across 303 deals. Important to also note that incumbents spend heavily on their internal R&D efforts too but it is not reflected in the figures, although it is a significant driver of further innovation and commercialization.

In comparison, over the last decade, startups developing for services applications have raised about $750 million, according to my calculations. However, $473 million, or 63% of that total, was from just three companies: Produce Pay ($343 million), Acre Trader ($83 million), and Bushel ($75 million).

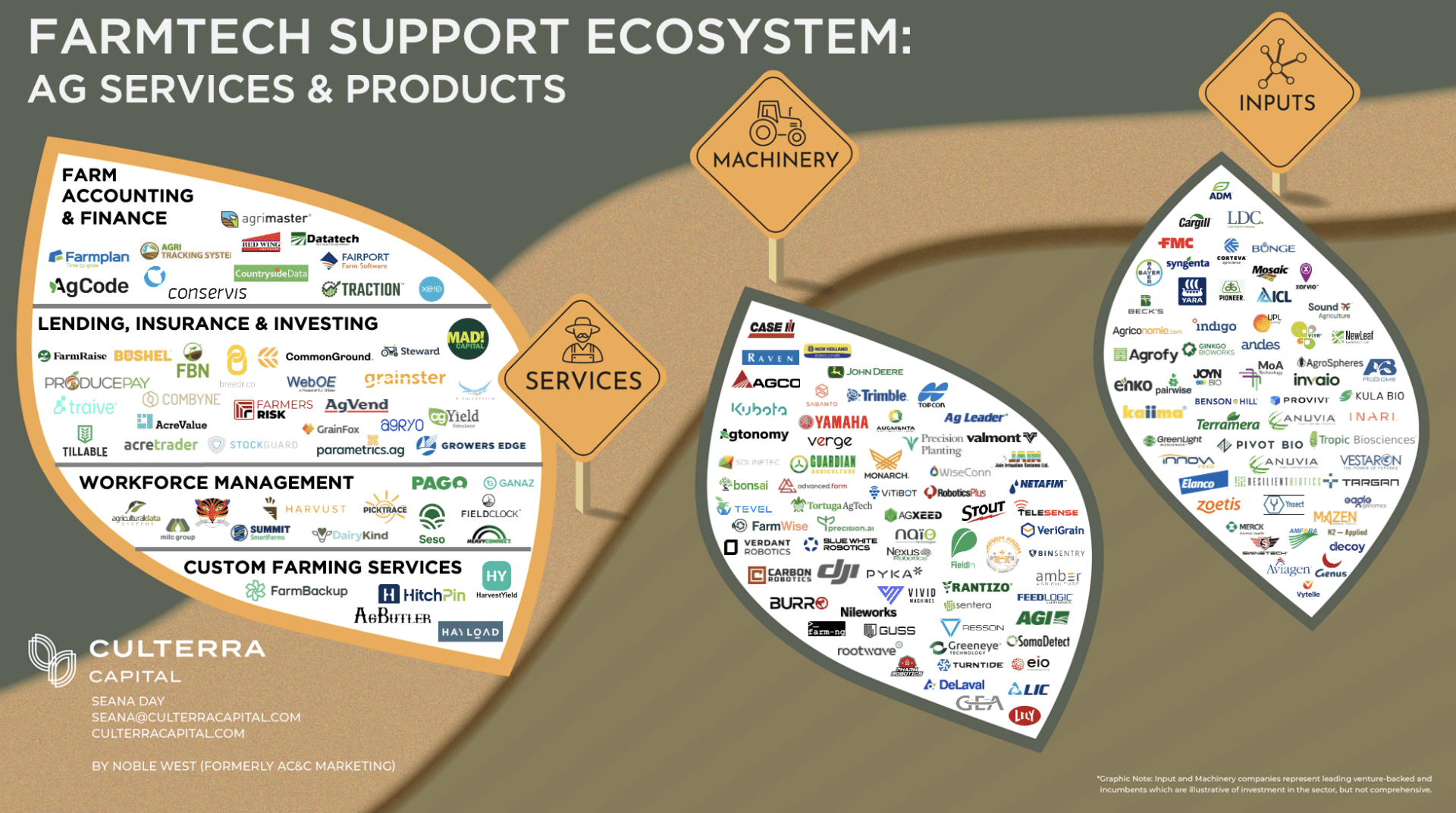

A guide to the Culterra Capital farmtech support ecosystem infographic

What this is (and is not)

- This ecosystem map (below) is focused on enabling technology inside the farmgate (but may include the First Mile in the future). While I include many innovators in the Machinery and Inputs sections, the main orientation is to highlight existing Services companies that provide tools used by the farmer to aggregate, share, or execute on services like tax planning/reporting, lending, investing/hedging, hiring, etc.

- This is not an exhaustive universe of solution providers, especially as it relates to Machinery and Inputs. That said, the Services group is, for the most part, comprehensive. I realize this might feel like comparing apples and oranges, but the idea is to illustrate a disproportionate level of innovation and investment relative to Machinery and Inputs.

Source: Culterra Capital. Download here.

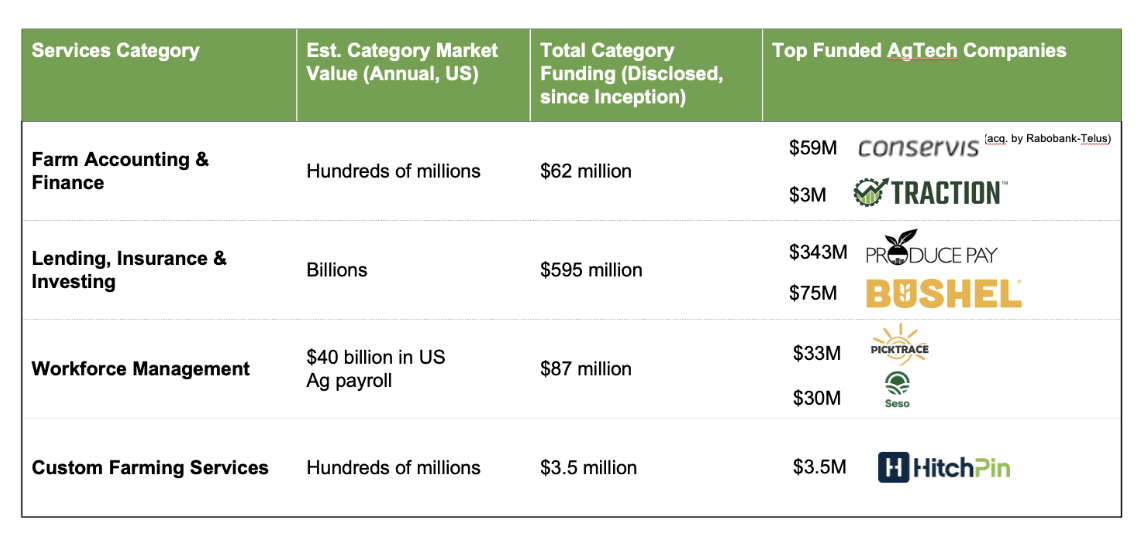

Farm finance & accounting

- Most of these companies are decades old and have built their highly sticky businesses as the vendor of record for farm financials with functionality that may include payroll, purchase orders, financial records, etc. In effect, the things a CPA might care about.

- It’s worth remembering that classic data ecosystems are built to meet reporting needs, not analytical needs. With existing infrastructure, analytical models require a considerable amount of time and customization. Extracting business insights from ERP systems requires a shift in data strategy and investment in analytics.

Lending, insurance & investing

- These companies are mostly on the forefront of the fintech + agtech wave and have raised comparatively more capital to disrupt existing models. I believe we are going to continue to see innovation and investment in this category as companies like Bushel, FBN, or Breedr extend their data infrastructure into financial services that can improve working capital for farmers.

- Many have carved niches that have been overlooked by traditional banks, investors, and insurers because of risk or economies of scale. These companies are digital native and using data to create or shift value pools (as I discussed in part 1) and investors have recognized the potential and jumped in aggressively.

Workforce management

- With $40 billion spent on US ag labor annually, and serious legal and financial risk for operators, the need for vertically focused ag HR platforms seems clear and compelling.

- I’ve also included several workforce training companies presently focused on the dairy sector. With an aging workforce that has high turnover, the need for knowledge transfer and onboarding is acute. I believe configurable training and communications tools designed to overcome low levels of literacy (reading and technology), as well as language barriers, will be increasingly critical as the Ag workforce modernizes and automation is more widely adopted.

Custom farming services

- Perhaps the least known to many readers, but this is a service layer that is essential to all production systems. It’s hard to estimate the size of this market but I would guess that it represents hundreds of millions of dollars of annual spend in North America.

- Custom farm services can include planting, spraying/applications, harvesting, and other activities requiring either labor or equipment that is offered “as a Service.”

- This sector of the farm economy is incredibly fragmented and still operates by phone, text, and paper. In the independent farm services sector, there are two primary ways of finding or selling services: signs on telephone poles or word of mouth. Given the size of the market and dependence on the farm services, the idea of a marketplace that can facilitate discovery and provide payment, settlement, and logistics feels like a clear opportunity.

The value of a strong middle market vertical stack

I often find myself navigating the investment tension between game-changing technologies that will have a big, disruptive financial impact on ag (and outsized investor returns) and the incremental, unsexy technologies that are creating the digital foundation for ag’s future.

There is a reason why investors have been hot on next gen inputs and machinery automation: they are game-changing. But verticals like construction, real estate — and even dental practice management (a $4.9 billion software market) — have embraced digitization despite being localized and highly fragmented. So again, I would say, “Why not ag?”

(PS) Why not another farmtech landscape?

After years of publishing maps for agtech, farmtech, and food supply chain tech that encapsulates the market landscape, I get a lot more excited these days when I can concentrate on a thesis or segment that reveals investable opportunities or overlooked trends. I think the difficulty of trying to capture them on one page reflects the vibrancy of global innovation and entrepreneurism in ag. This evolution is a good thing.