Ariadne Caballero is a partner at SP Ventures, an early-stage fund investing in agrifoodtech across Latin America. Juliana De Podesta is head of ESG at SP Ventures.

When we talk about current challenges in global warming, we face two main ones that are complementary but often seen as antagonistic: the fight against climate change and the increase in demand for food.

In this context, we find ourselves with a sector that in our opinion will be a major player in the solution but is often seen as part of the problem: agribusiness.

Contrary to what many think, agribusiness has evolved a lot in recent decades, and this evolution has accelerated with the collaboration of agrifoodtech.

Through agrifood innovation, six major trends are repositioning the sector and unlocking its game-changing potential: on-farm technology, bio-alternatives, access to credit, more efficient supply chains, avoiding food waste and the increase of carbon markets.

Technology in the field

Historically the agrifood chain has already been replete with technological innovations that have improved the lives of farmers, increased productivity and elevated management to a new level.

The management systems themselves are a clear example of how technology is already present in the sector. Through SaaS models, these systems have been gaining more and more relevance and expanding their presence in the operation of small and medium-sized farmers, which allows them to be more efficient, reduce waste and increase their productivity. Startups that offer management technologies already represent more than 24% of agritech in Brazil that operate “on the farm,” with the highest adoption rates by farmers.

However, the Saas model goes beyond management systems. Agritech offers a set of services and tools that allow the producer to optimize routes during harvest, implement precision agriculture and even have access to remote soil analysis. Through these and other new technologies, increased productivity is achieved without the need for new land. It is accompanied by a reduction in the use of inputs, resulting in a more sustainable agriculture with lower emissions.

Examples of companies tackling this challenge in our portfolio: Aegro, Verge and Leaf.

Bio-alternatives

Along with reducing the use of inputs (fertilizers, chemicals) and increasing efficiency, alternative inputs appear. In an era where we seek productivity in parallel with conserving soil, water and biodiversity, biological inputs are gaining momentum. In 2021, according to Radar Agritech 2022, this category raised $ 2.6 billion, an increase of more than 30% in the volume invested over the previous year.

Biopesticides have been an innovative and effective solution to combat pests for small, medium and large farmers as a way to reduce chemical products. By replacing chemicals, even partially, the sector reduces significantly its potential negative impacts, eliminating the risk of soil and water contamination and often contributing to climate resilience.

Along with biologics that act as alternatives, the sector has seen the raise of complementary solutions, such as microbes. Innovation in this area may be key to restoring degraded areas (making production possible where it was not possible), as well as in adapting to climate change and increasing the resilience of food production in the coming decades.

Examples of companies tackling this challenge in our portfolio: Gênica, Decoy and PunaBio.

Access to credit

There is no point in having technology and alternatives if the farmer is unable to access them. Agrifintech has played a relevant role in the transition of the sector. The empowerment of small and medium-sized farmers allows not only greater professionalization and greater governance in the chain, but also the long-awaited increase in productivity and reduction of the carbon footprint.

The reduction of bureaucracy, the increase in speed and the inclusion provided by agrifintech have placed small and medium-sized farmers, so present in the Brazilian reality, closer to the big players in the sector. Agribusiness is intensive in working capital and activities should become more uncertain with the intensification of adverse weather events. The use of technologies combined with new business models is essential to finance agriculture that is resilient to climate change.

Reaching new levels of efficiency and productivity using technology, alternative inputs and greater intelligence in the field is essential to meet future demands and ensure a more sustainable agribusiness.

By implementing these best practices in the field and aligning them with ESG criteria, we achieve greater transparency and traceability of the chain and greater resilience of the sector. This new scenario with reduced risks enables most affordable credits for the farmers, feeding back a cycle of responsible evolution.

Examples of companies tackling this challenge: Agrolend, Traive and Verqor.

More efficient supply chains

In addition to innovations in the field and in the life of the farmers, the evolution of the sector expands throughout its chain. The search for efficient and shorter chains has intensified over the last few years and the appearance of solutions that connect the farmer with the final consumer has been key in this process.

The reduction and even elimination of intermediaries allows greater traceability of the products, in addition to reducing logistical costs and waste throughout the chain. As a result of this new way of operating, the final consumer has access to higher quality, more accessible products with a lower carbon footprint.

Along with the various advantages for the consumer, the reduction of links in the chain also contributes to a fairer remuneration for the farmer (fair supply), empowering him as well.

Examples of companies tackling this challenge: Agrofy, E-Rural and ZoomAgri.

Food waste avoidance

Going one step further in the chain, we need to take a deeper look at the issue of food waste. It is useless to produce more, reducing the carbon footprint of these foods and not enabling them to reach their destination.

We are currently in a reality where 30% of all food produced in the world is wasted. In addition to this problem going directly against the challenge of feeding an growing population, it still has a significant impact on fight against climate change, given that all this food waste leads to emissions in landfills and dumps.

Looking for solutions, foodtech companies have gained strength, not only disintermediating chains and collaborating with their efficiency, but also contributing technology as a partner in food management.

Examples of companies tackling this challenge: Frizata and Clicampo.

Carbon markets

Along with actions to reduce emissions, companies and farmers rely on a new market that has been gaining more and more strength: the carbon market.

Carbon credits, currently much discussed, are an important part of the solution to combat climate change. Through preservation, conservation, reforestation, carbon capture and even by efficiency of processes, it is possible to reduce concentrations of greenhouse gas and collaborate with the goals established by the Paris agreement.

However, it is important to remember that this market alone is not the solution. To fight climate change, we need to work with a set of actions, including climate change mitigation through emission reduction, process efficiency and investment in new ways of producing. In addition, the constant search for best practices and the focus on resilience and climate adaptation are essential.

Examples of companies tackling this challenge: Moss and GoFlux.

Different ways of contribution in the fight against climate change

The trends described above contribute to the fight against climate change in three different ways:

- Technologies that allow the reduction of emissions, contributing to net zero

- Technologies that contribute to climate adaptation and resilience

- Carbon negative technologies, which capture or storage carbon

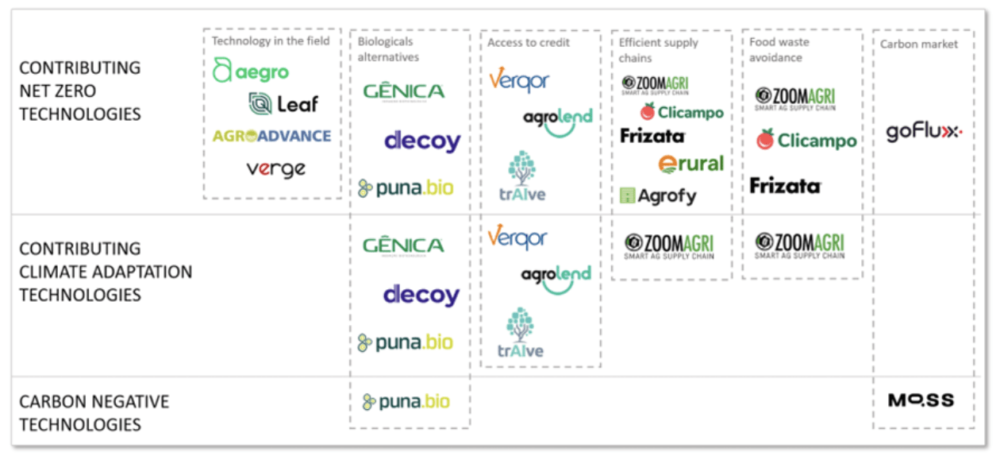

SP Ventures, in its most recent fund, AGVII, has a portfolio of agri companies that play an important role in against climate change. The image below illustrates the capillarity of impact of this portfolio and highlights the potential of startups in the face of current challenges.

Conclusion

These are some of the market solutions that have gained strength in the current context and that have positioned agrifoodtech as protagonists in the transition towards low-carbon agribusiness and a more efficient food chain.

However, the challenges of combating climate change and the increasing demand for food are far from resolved. We see a very fertile market for the future, especially within the ag and food sectors, but to ensure a positive impact and to move towards solving these challenges, it is necessary to evolve in the way of identifying, measuring, and monitoring the impact, providing transparency to the market.

The new report from S&P Global Sustainable brings data showing that less than 10% of climate funds are aligned with the global decarbonization goals, which emphasizes the need for consistent, comparable, and transparent methodologies with the market:

“Companies are under pressure to understand their warming trajectory and plan accordingly to decarbonize. This same analysis can be extended to equity and mutual funds, which represent trillions of dollars of investments and play an important role in the energy transition of the broader economy. Our analysis points to a systemic issue — few funds, even those that describe themselves using green or climate-specific language, are on track to meet the goal of the Paris Agreement. Understanding the trajectory is an important step toward planning for a low-carbon future.”

Given the relevance of startups on this journey, VC investors and funds play an important role not only in selecting their investments aligned towards these goals, but also in being part of this evolution, working with their portfolios to develop measurement methodologies and ensuring the quality and veracity of the data. This partnership is essential for the market and for the development of these solutions and those to come.