Editor’s note: Seana Day is a Partner at Better Food Ventures and The Mixing Bowl, with 15 years of finance, M&A, and technology experience. She is the author of the 2019 Agtech Landscape and Livestock Tech Landscape. Seana lives in Turlock, the heart of California’s ag land.

As many of you may know, I have been tracking the majority of agtech startups for close to five years. With this release of the 2019 AgTech Landscape, I am now tracking over 1,600 startups.

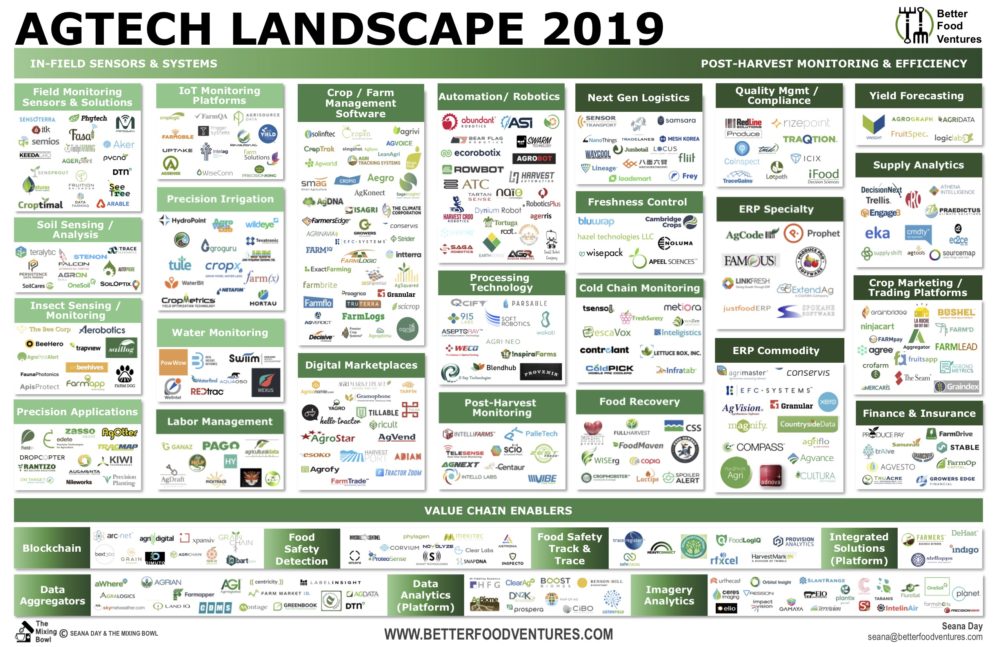

It’s been a wild ride watching the agtech landscape explode these past five years. We have seen the rise of in-field sensors and technologies like drones become commodities; the move from sensing for in-field data to correlating and analyzing data for insights that can be rolled up into farm management systems; the emergence of better farm business management tools; acknowledgment of the need to connect “ag” to “food”; and the rise of new, disruptive marketplaces connecting the seed-to-store value chain. It’s an understatement to say that the agtech landscape is developing and maturing rapidly.

Here’s a brief background on the landscape before I dig into my key takeaways below:

Landscape map background

- This is heatmap more than a comprehensive list. I would suggest you use the landscape as I do, as a tool to provide perspective on where activity is (or is not) and recognize some of the noteworthy companies in particular sub-sectors of AgTech. The goal of the landscape is not to exhaust your eyes with a comprehensive list of all of the AgTech startups and companies.

- Focus on IT for ag: The landscape focuses predominantly on digital and Information technology-related technologies, corresponding to my experience and that of my colleagues at Better Food Ventures and The Mixing Bowl.

- AgTech: seed through supply chain. My colleague Brita Rosenheim and I call part of the supply chain “the messy middle of food” where agtech meets foodtech, and that’s included here alongside farmtech.

- Focus on crops and outdoor agriculture: This market map does not include livestock-related technologies, including aquaculture, or indoor farming as I need to stay focused on the wealth of innovations for the outdoor crop farming world. (Watch out for the next Indoor AgTech Landscape from my colleague Michael Rose soon).

Key takeaways: 2019 AgTech Landscape

Post-harvest technologies gather steam: In previous years, this landscape was a more equal division between “in-field” and “post-harvest” startups, but now we’re seeing more startups — close to two-thirds — focusing on the post-harvest space.

Of course, the in-field space is still growing, particularly in some areas. For example, this year I created a new category for startups related to bees and pollinators called “Insect Sensing/Monitoring.” We have also added a category of “Labor Management” as we see technology springing up to address the acute challenges in the specialty crop sector with next-gen companies like Pago, Ganaz and HY improving the finding, keeping and managing of agriculture labor forces.

An important driver of this broader activity in agtech is a shift from “farming to maximize yield” to “farming to maximize profit” by looking at farming operations, not just precision ag. Abundant production in key commodities like grains and dairy have caused prices to drop and therefore producers seek ways to make farming operations more efficient.

Correspondingly, we are sensing a greater or renewed interest in farm management systems that link farming operations (digital agronomy) more tightly with farm business/finance operations to cut costs, identify new or lost revenue streams, or look more holistically at their true cost of production by seeking new data-driven financing options, for example. Producers need better linkages between the systems tracking the activity in the field and their financial systems, not just the cost of what producers are doing in the field. Existing companies like Conservis, Granular (part of Corteva), EFC Systems, and AgDNA are all taking steps to bridge the farm business data gap.

“Digital Marketplaces” are making it possible for farmers to buy inputs directly or rent/lease equipment (i.e., “Uber for tractors”). Much of this digital marketplace or “collaborative commerce” action is happening in developing economies where the spread of connected digital devices among farmers is improving access, although there are key players in the US such as Farmers Business Network.

Drivers of the growth in “post-harvest” innovation could be attributed to increased focus on the often overlooked “first mile” of food logistics and transport after the farmgate to the packer, shipper or processor. This segment includes logistics, sensing and analytics technologies that can be applied at the point of harvest through to the packer, shipper or processor.

This “messy middle” of food could be drastically improved and through better integration of on-farm activity with post-harvest activity (like logistics, freshness monitoring, and processing) there may be ways for food producers to reduce waste, improve profitability, monitor quality, or develop new value-add opportunities.

Investment to Midstream Technologies, as AgFunder calls them in its funding reports, increased 44% to $852 million in 2018, and while that’s the fourth biggest upstream category, it’s far behind the “last-mile” consumer-focused startups where more than $8 billion of funding went in 2018.

When you consider that food waste is a $1 trillion question — and that food delivery apps might be exacerbating it (plus plastic packaging) — funding can often seem misaligned with where innovation is needed.

The desire for better tracking, transparency, and security in our food system is also driving innovation. Data transparency will provide the linking mechanism in the previously mentioned drivers and also address the desire for food companies to tell consumers about the provenance of their products.

I would be remiss not to mention the buzzword of “blockchain for food”. I see this as a triggering technology that will wind its way — gradually — through the messy middle of food, driven in part by Walmart and IBM’s Foodtrust. That said, the adoption curve feels farther on the horizon in agriculture than many might have you believe; not only will farmers and ranchers struggle with the cost-benefit of adoption of blockchain, but there’s still a lot of work to be done to establish the basic data flows in agriculture operations. The data need to be in place first before we can start blocking and chaining it. The lack of adoption of open agriculture data standards has much of today’s ag data siloed and is a key barrier to seeing greater tracking and tracing in the industry.

Value chain enablers: A second, big macro change you will see to the landscape in comparison to year’s past is the horizontal band at the bottom for “Value Chain Enablers”. Further to the above theme of a greater focus beyond the farm, I want to recognize that a growing number of ag technologies are enabling both “In-field” and “Post-harvest” to connect and create a fuller value chain.

A new area in this category is “Integrated Solutions” that are well-financed companies like Farmers Business Network, Benson Hill, and Indigo Ag that aspire to turn supply chains into new value chains, creating greater linkages between farming and end food products, similarly for StellaApps and dairy in India. Looking forward, it is likely we will continue to see startups tackle the full stack of digital agriculture as they shorten supply chains and find ways to reallocate margin back to producers.

Looking ahead at the 4 Cs: Consolidation, collaboration, conservation, and (big) companies

Consolidation: To put it bluntly, we have had too many agtech point solutions funded and we can expect to see many go away or get consolidated. We have already seen this in AgFunder’s 2018 funding report where agtech M&A activity picked up substantially in 2017 and 2018. This is particularly evidenced in the FarmTech segment with in-field hardware, sensor and imagery companies but it goes for other agtech categories such as farm management systems as well. We will likely see more consolidation in the future, and although not always blockbuster outcomes for investors, an increased level of consolidation activity is generally a signal of a healthy ecosystem.

Big companies: We have started to see some of the big companies, including technology companies, increasingly step into the agriculture space and fill gaps in infrastructure and offer scalable solutions: from IBM on the weather, analytics and cloud infrastructure side; Amazon with AWS for Ag; Microsoft with its FarmBeats IoT solution; the big companies are paying more attention to this sector than they have and we can expect they will continue.

It is also worth mentioning big food companies like Costco (with its chicken operation in Nebraska) or Walmart (with its dairy operation in Indiana) are making moves upstream in the production chain. It will be interesting to see if this trend continues.

Collaboration: A key theme that I have seen over four years in this space is a recognition of the need to collaborate more, whether that is between farmers or between big companies and startups. Maersk created the FoodTrack by Maersk accelerator program to collaborate more with and invest in startups. We have also seen an interesting pilot partnership between Conservis and Rabobank; companies like Land O’ Lakes and Mars looking for external sustainable dairy solutions; the Pork Council reaching out with its Manure Management Challenge; and the Sustainability Consortium showing the value of collaborative efforts. The same can be said within the emerging growth ecosystem where there is a realization among many that the one-stop-shop approach is difficult and costly; to stay relevant, some startups are finding value in partnerships and data interoperability.

Conservation: Whether we call it conservation or sustainability, an undeniable theme is that it is not going away — and the European agrifood scene is leading the charge in many ways. The Europeans have already started to make a general mindshift to close the gap between agriculture and the rest of society to see what can be done to improve the impact of food production on the environment. The farming industry needs to do more to tell the stories of how farmers are acting as good stewards of the land, water and air, and the potential it has to do even more for the environment. It also needs to embrace new technologies that enable food producers to produce the data to quantify the sustainability benefits they are producing, Land O’ Lakes’ Truterra Insights is a good example.

I welcome your thoughts and reactions and look forward to following this exciting agtech landscape together for the coming years.