Mark S. Brooks is former Head of FMC Ventures; former investment manager, Syngenta Ventures.

Mark works at the intersection of science, capital allocation, and innovation in complex industries, with agriculture as a recent lens. Reach him at [email protected].

The views expressed in this article are the author’s own and do not necessarily represent those of AgFunderNews.

Rather than a temporary downcycle to be waited out, agriculture is undergoing a fundamental repricing of risk.

The market is no longer just reacting to earnings—it is rewriting the cost of capital for an industry where competitive advantage erodes faster than ever.

Corporate lifespans have compressed dramatically since the mid-20th century, and markets punish slow reinvention. Despite the world’s need for sustainable food, fiber, and fuel, this industry’s incentives and capital structures favor defense over reinvention.

In an era of rapid change, defending the past is riskier than creating tomorrow. Here is what’s shifting and where advantage will compound next.

Surface signals

These data points are illustrative, not judgments of leadership. The takeaway is that this system is being repriced.

Upstream players:

FMC Corporation’s market cap has fallen ~80% over the last two years (~$7.9B at end-2023 to ~$1.7B at end-2025), driven by channel destocking (especially Brazil), patent cliffs, and margin pressure.

BASF plans to partially list its Agricultural Solutions business around 2027. This suggests that the capital intensity, regulatory burden, and timelines of traditional ag R&D no longer clear internal return thresholds versus other capital uses.

Corteva’s plan to decouple IP-driven seed growth from the rising regulatory and litigation uncertainties of crop protection unwinds a two-decade industry narrative that traits and chemistry should be integrated.

Bayer’s glyphosate litigation has imposed multi-billion-dollar settlement/provision costs and created a persistent equity overhang.

Syngenta remains vertically integrated, but as a state-backed Chinese enterprise, its economics and strategic priorities are less transparent to public markets. Its position nonetheless shows how geopolitics and state-backed capital can shape competition in ways investors cannot easily price.

Fertilizers are a parallel stress-test. For example, Yara reported restructuring costs in 2025 and continues to flag the sector’s sensitivity to energy (natural gas) costs.

Generics and fast followers (UPL, other formulators) are resetting price ceilings as more actives go off-patent, strengthening retailer leverage and accelerating private labels.

Downstream players:

Distributors (Nutrien, Wilbur-Ellis, Growmark) are expanding private labels and tightening shelf control as rebates weaken and price transparency rises. More gross margin shifts to products they control, not pass-through brands.

Equipment manufacturers (Deere, AGCO, CNH) are repositioning around precision, autonomy, software, and data, recognizing that iron alone no longer captures enough value. OEMs are being valued less as cyclical manufacturers and more on data value and switching costs.

Processors (ADM, Bunge, Cargill) are navigating margin volatility, geopolitical trade shifts, and rising scrutiny around resilience and sustainability. This pushes the system toward more auditable supply chains, and raises the value of data and verification infrastructure.

A workforce reset is also underway. Strategics have announced more than 25,000 role reductions since 2023. Retirements accelerate, experienced leaders switch industries, and more people join or start new ventures.

Furthermore, venture capital has pulled back. Global agrifoodtech investment fell to $15.6B in 2023 (-49% YoY) and was about $16B in 2024 (-4% YoY)—still far below the $51B peak in 2021. Fewer pure-play ag funds exist. More startups are being forced into exits or downrounds. Survivors must quickly prove defensible IP, clear regulatory paths, distribution, and strong unit economics.

Together, these are signs of a system being repriced from every angle.

Pressure beneath the surface

Regulatory tightening, litigation exposure, geopolitics, and high capital costs are colliding with technological change. Biologicals are moving from adjacent to essential. AI is lowering the cost of creating candidates across chemistry, biologicals, formulation, and traits. The gap between “promising” and “proven” is widening because field validation, regulation, and channel adoption don’t speed up at the same rate. Patent cliffs shift bargaining power to the channel and the lowest-cost formulators.

R&D intensity is hitting a ceiling and, in real terms, has been flat or declining in recent years as incumbents prioritize capital efficiency over raw discovery.

The science-intensive parts of the industry are “pharma-izing.” Discovery gets cheaper at the front end, while development and launch stay expensive and regulated. Ag majors may do what drugmakers did: reduce R&D burn, source more innovation from startups and universities, and concentrate spend on development, registration, manufacturing scale-up, and commercialization. Advantage shifts from the biggest lab to the best access-and-scale engine.

The hardest constraint remains the farm P&L. When commodity prices soften and input costs stay high, purchases get deferred, thresholds for adoption rise, and inventory and credit become the throttle on volumes and pricing.

None of this means agriculture is broken. It’s inelastic. People don’t stop eating. Farmers don’t stop farming.

The system continues to generate cash even in stress. What is breaking are the capital and operating models that governed the last 50+ years.

Where value compounds

Value concentrates at choke points: formulation and manufacturing; aggregated IP platforms (especially in biologicals and delivery); distribution and channel access; trusted agronomy/advisory networks; financing tied to inputs and offtake; and data layers that create feedback loops and visibility across the value chain.

Returns can be disproportionate because these choke points have recurring take rates—a spread on units moved, hectares served, products registered, or batches manufactured—reinforced by switching costs, channel access, and regulatory complexity.

Similar compounding is visible in adjacent spaces like timber and forestry (e.g., Weyerhaeuser, Nuveen). There, long-cycle biology, plus data, asset control, and financing create optionality (carbon, materials, land-use).

The next ag/food cycle will favor long-horizon orchestrators who can align capital, discovery, manufacturing, regulation, and go-to-market into durable cash flow, defensible moats, and platform-level compounding.

This is where risk is mispriced. Venture capital operates on 6- 10-year return horizons. But meaningful innovation in ag (biological discovery, regulatory approval, farmer trust, platform build-out) unfolds over 7- to 15-plus-year cycles.

The irony is that what frustrates short-term capital is what makes agriculture one of the most resilient and mispriced systems in the global economy.

One way to see the opportunity is through fulcrums, points where shifts in commodities, biology, logistics, inputs, and offtakes have outsized effects. Capital that understands where fulcrums form can reshape how value flows through the system. That’s the lens.

Consolidation is here

Consolidation is now a survival tactic used to right-size operations and rebuild innovation engines under intense balance sheet pressure.

Many incumbents face significant balance sheet strain. Bayer reported net financial debt of €32.7B (30 Sept. 2025) and has said financing flexibility isn’t for M&A. FMC reported total debt of $4.5B (Q3 2025) with negative free cash flow. With cost discipline and deleveraging taking priority, expect fewer transformational deals and more structured, capital‑efficient partnerships. At today’s valuations, structured combinations become plausible.

Startups face the same pressure. Capital scarcity, overlapping technologies, and fragmented go-to-market are forcing them to confront uncomfortable realities. A smaller number of platform companies that aggregate IP, data, manufacturing, and distribution are likely to emerge as category leaders through rollups. This may be the best moment in decades for consolidation across the industry.

If I’m wrong, it will be because regulation loosens faster than expected, cost of capital falls quickly, and incumbents regain pricing power through a new product wave. In that world, consolidation slows, M&A picks up, and the old model gets a second act. I don’t see that as the base case, but it is a falsifier.

What comes next

Innovation in ag isn’t dying. The old model is. If the last decade was about building and defending scale, the next will be about orchestrating systems.

The next cycle belongs to leaders who can deliver through near-term volatility while still investing through long-cycle uncertainty. That requires an operating model built for options where corporate venture capital, partnerships, and M&A are core levers tied to enterprise renewal and risk discipline.

In the new cycle, defending the past is not the safest bet. Creating tomorrow is.

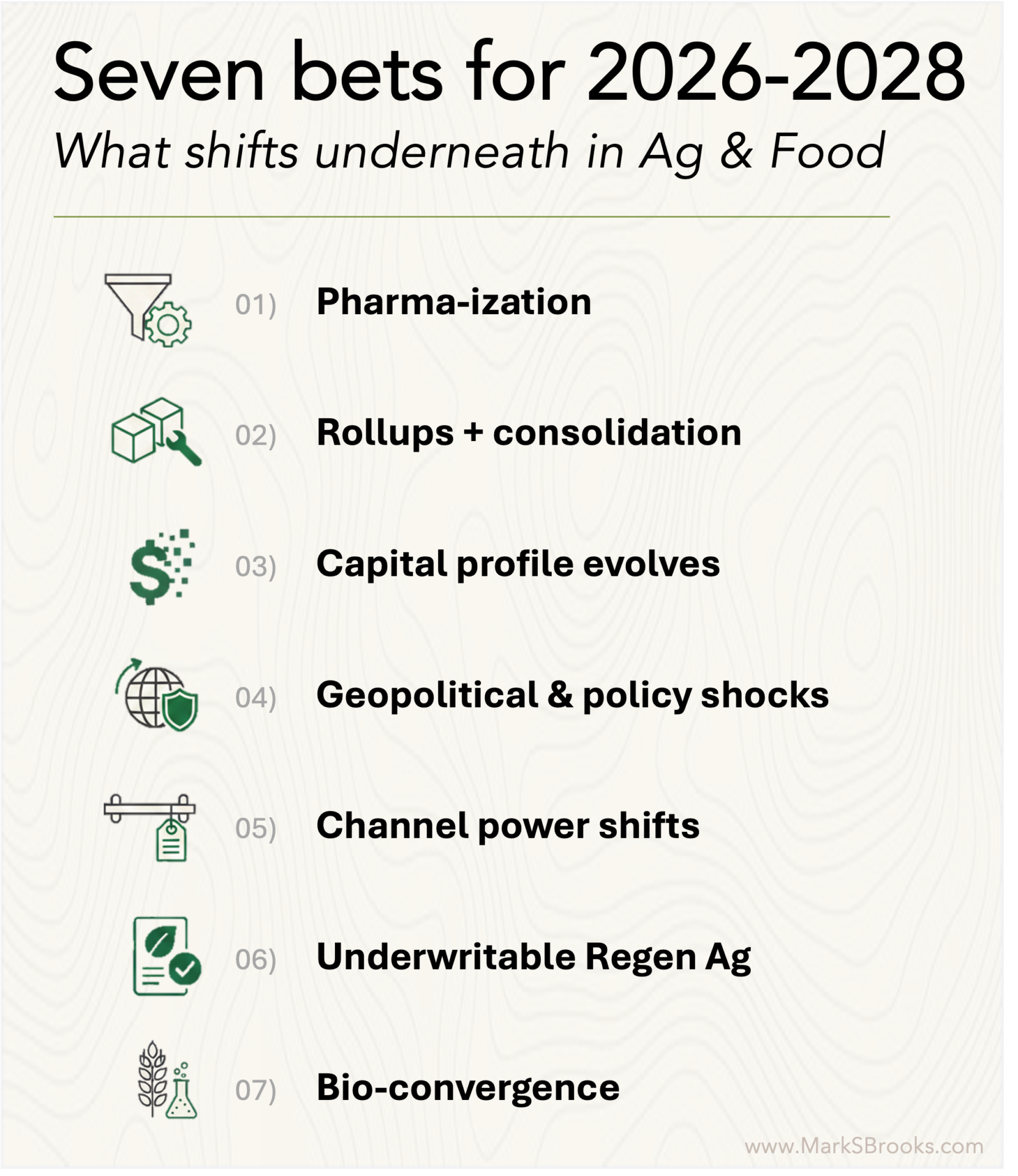

Seven bets for 2026-2028

“Pharma-ization” shows up in how strategics spend and partner.

- As discovery becomes cheaper and decentralized, competitive advantage will concentrate in late-stage registration, manufacturing scale-up, and commercial access.

- Watch for: R&D spend flattening/falling, more licensing, co-development, and JVs.

Two layer consolidation – assets rollup, majors refocus.

- Builders with domain expertise will rollup fragmented assets. Some strategic consolidation at the top may follow as balance sheets and portfolios force focus.

- Watch for: mergers of equals, distressed tuck-ins, rollups anchored on channel access + manufacturing/formulation + IP stacks; and, at the top, carve-outs and deals framed around deleveraging or litigation containment.

Capital profile evolves.

- Traditional agtech venture capital continues its retreat, replaced by more patient, long-term investors.

- Watch for: increased family office exposure to early-stage startups and a rise in blended finance models.

Policy and geopolitics create constraints.

- Trade wars and export controls can trigger sudden shocks to technology and commodity flows. Corporate performance will increasingly be dictated by policy exposure rather than pure execution.

- Watch for: stricter screening of foreign VC in “sensitive” sectors (AI, biotech, food security) and guidance moves tied to geopolitical shifts.

Channel power shifts.

- Distributors decouple from major manufacturers by scaling private and white-label products sourced from startups and generics suppliers.

- Watch for: increased in-house formulation and shelf-space decisions that favor distributor-owned SKUs.

Underwritable regen ag.

- Regenerative agriculture scales when outcomes are verifiable enough to be insured and financed.

- Watch for: contracts, loans, and insurance terms tied directly to verified outcomes (traceability, residues, soil health); channel-embedded finance; innovation in forestry and timberland.

Bio-convergence pulls ag into new value pools.

- Agriculture moves beyond calories to provide verified inputs for human health (metabolic outcomes), the energy transition (low-carbon feedstocks), and advanced materials.

- Watch for: contracted acres with premiums for measured specs (protein, oil profiles, residues).

![]()

Sign up for our weekly newsletter.