Data snapshot is a regular AgFunderNews feature in which we analyze agrifoodtech market investment data provided by our parent company, AgFunder.

Click here for more research from AgFunder and sign up to our newsletters to receive alerts about new research reports.

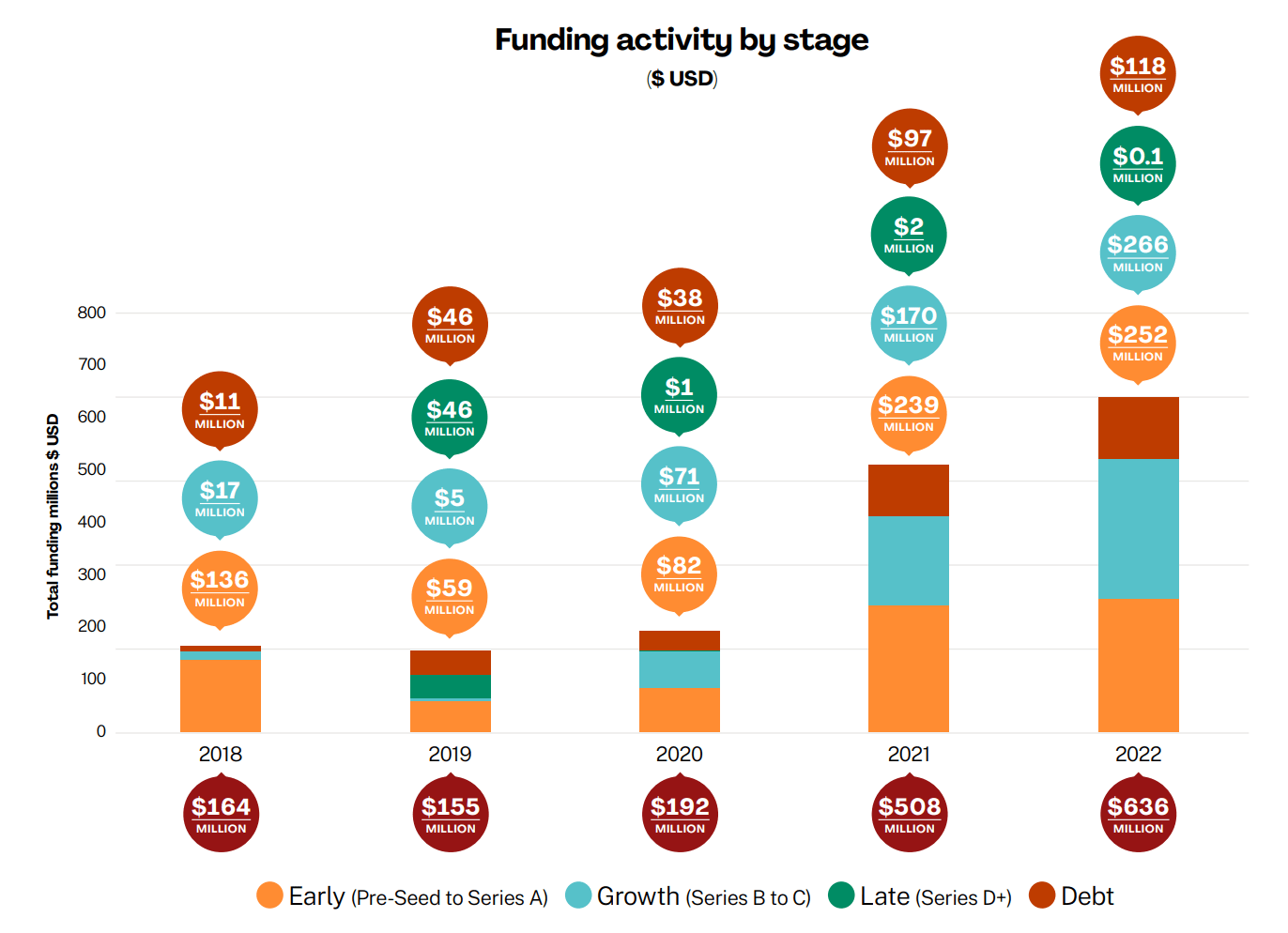

Funding dynamics in the African agrifoodtech ecosystem have for years been characterized by venture capitalists having a bias for early stage startups. Over the past two years, however, there has been a notable shift as investors direct resources to maturing firms, according to AgFunder’s new Africa AgriFoodTech Investment Report produced in collaboration with the Bill & Melinda Gates Foundation, FMO Ventures Program, and Mercy Corps Ventures.

The report indicates that although Africa continues to witness a mushrooming of agritech startups, investors are pumping relatively more money into growth stage firms today than they were a few years ago.

Ghana’s Complete Farmer, which recently closed a $10.4 million pre-series A round, is among early stage startups that have cited “seed funding scarcity” as a challenge.

The shift towards series B and C funding and debt is evident. In 2022, growth stage startups attracted 28.1% of the funding compared to 10.3% in 2018.Debt financing, which was nearly non-existent five years ago with only $11 million in funding, topped $118 million in 2022.

Factors behind the emerging trend include increasing risk aversion among investors, an eye on economies of scale driven returns, and exit planning. This is critical at a time when investors are grappling with economic uncertainties including high inflation and rising interest rates.

Though early stage startups still dominate in terms of deal count, accounting for 77.5% of deals in 2022, mature firms such as Kenya’s Wasoko have attracted the lion’s share of investment capital, raising $125 million in 2022, while MaxAB and Apollo Agriculture both raised $40 million in series B rounds.

Nigeria’s ThriveAgric, which secured $55 million in debt financing last year, is another pointer to how maturity anchored on strong financial bases, sound management and governance and unambiguous strategies is informing investment decisions.

“We see growth in agro-lending, agro-light processing, agro-logistics and agro-marketplaces,” says Ndubuisi Ekekwe, chairman at Tekedia Capital.

That said, early stage startups remain fundamental in Africa’s agricultural landscape, explaining why investors pumped $252 million into early startups last year.

Apart from offering investors a huge pool of investment options, a key factor on why early stage startups remain on the radar of investors is the zeal and determination of founders to scale, impact and expand.

A case in point is Tunisia’s Beekeeper Tech that raised $640,000 in a seed round. The agritech startup has invested significantly in R&D to develop its own genetic breeding models for the purpose of naturally selecting the most resilient colonies. The impact has been reducing losses for beekeepers due to climate change, pesticides and mites.

H1 2023: Sharp YoY declines in funding

Investment in agrifoodtech startups in Africa surged 25% in 2022 against a backdrop of sharp declines in most other markets. However rising interest rates, currency volatilities, and inflationary pressures have curtailed this growth trajectory in the first half of 2023, according to AgFunder’s Africa AgriFoodTech Investment Report 2023, which you can download HERE.