Despite constant news of multi-billion dollar funding rounds by a handful of AI companies, the rest of the tech market—both public and private—continues to be beaten down. What started as the so-called SaaS apocalypse has evolved into a broader software apocalypse, with public companies trading at historical lows.

Many are down to 2x-5x revenue multiples, levels you typically see for CPG valuations, compared to the 8-10x+ multiples we’ve seen historically.

Three fears are driving this:

- AI will eliminate jobs, so SaaS companies won’t sell as many seats.

- Customers will use tools like Claude Code to build their own solutions.

- The ease of building software will spawn 100x-1000x more products covering every longtail niche, preventing anyone from achieving sufficient scale while necessarily driving up customer acquisition cost.

The software apocalypse: public markets at historical lows

Consider a few examples.

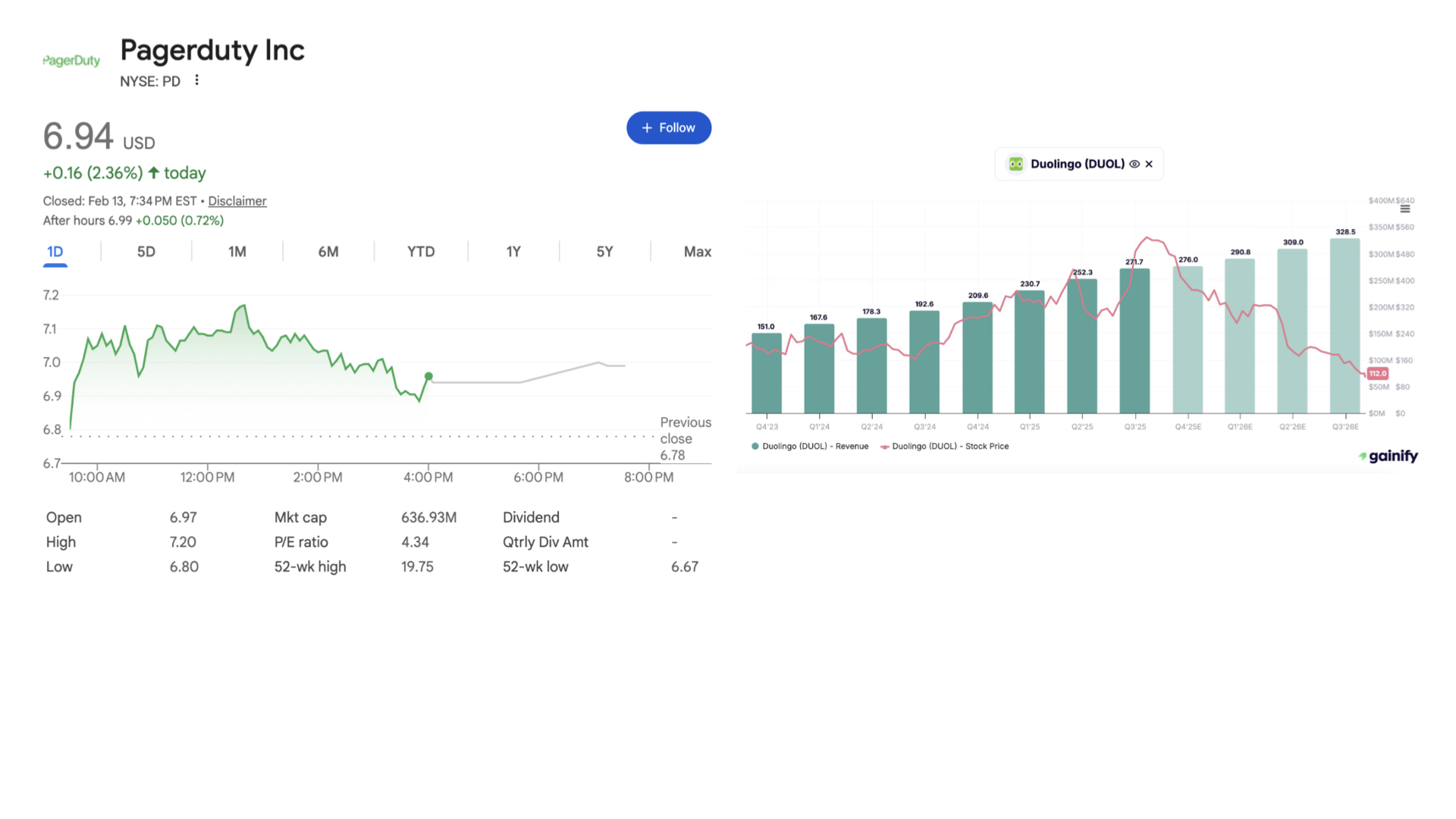

PagerDuty, which automatically detects, triages, and routes critical alerts to on-call engineers, now trades at a P/E of just 4.34 and a revenue multiple of 1.36x. Duolingo has grown revenue 2.5x over the past two years with healthy cash flows, yet the stock has fallen from its May 2025 IPO price of $529 to $112 today, trading at a P/E of 14. PayPal, which also owns Venmo, now trades at a 7.45 P/E and a price-to-sales ratio of just 1.1x. The company is valued at only $37 billion even after announcing $6 billion in buybacks for 2026—leading investors to call it “PainPal” because just when you think the stock can’t go any lower, it gets cut in half again.

Even beyond software, there is fear around supposed AI-safe havens like Amazon, which is trading at a P/E multiple of 27, compared to Walmart, which is trading like a hot internet company with a PE multiple of 47.

Similarly, Microsoft—which owns nearly 30% of OpenAI and has full access to their IP at any time—is trading at a $3 trillion valuation and a P/E multiple of 25.

I get the sense the market is playing a game of musical chairs: feeling existential dread around the impact of AI, and everyone is on a hair-trigger, trying to be the first money just before it all comes crashing down. As crazy as things are about to get, most of these companies are not going away anytime soon.

A vacuum in mid-stage private market funding

As hard as it is to believe, private markets are in even worse shape.

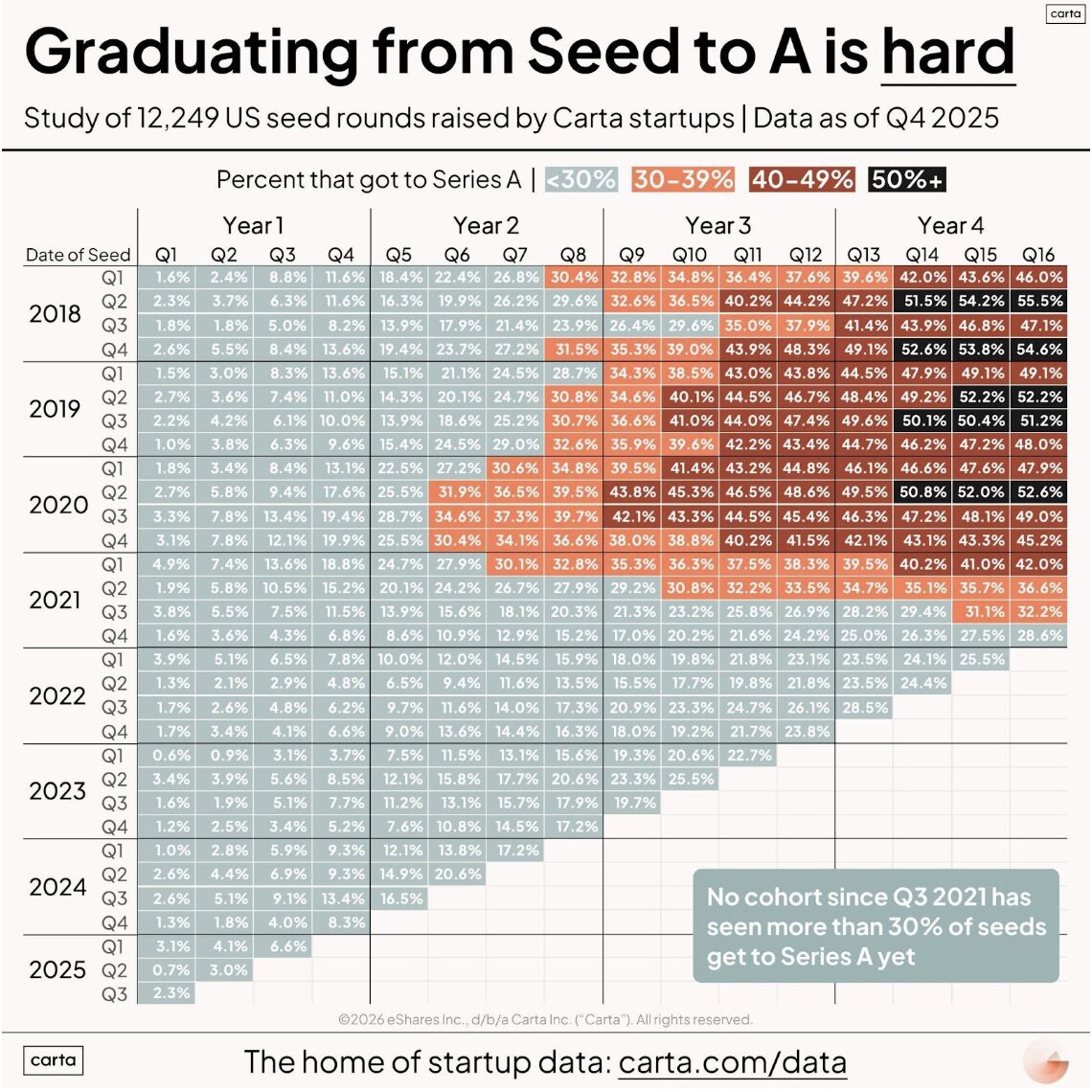

Carta’s data on seed-to-Series A graduation rates going back to 2018 tells the story. Historically, a decent company had around a 50% chance of raising a Series A within 3-4 years. That’s been cut in half. Since Q3 2021, not a single quarterly cohort of seed-stage companies has reached a 30% graduation rate. This isn’t a random sample either—Carta manages cap tables for all YC companies, which adds 500 new startups annually. And given the AI boom, you have to assume a significant portion of those graduating have somehow captured the AI zeitgeist.

The core problem is that the top 20 funds are capturing over 80% of all LP dollars. Because they’ve shifted their focus to a small pool of AI companies (and in some cases, defense and energy) and represent the vast majority of late-stage funding, this has left a vacuum in the rest of the market with no one to step in.

All of this is leading to fire-sale valuations across multiple stages.

Positioning for the future as value shifts to physical AI

Yet arguably, much of software may get commoditized away over the next 24 months, pushing value toward hardware and startups operating in the physical world, a space that’s been cast aside for the past four years, and exactly where we’ve focused. We just need to stay in the game long enough for the market to turn. And when it does, it should turn quickly.

The next 18 months are going to be crazy

Many Silicon Valley engineers are gripped by a deep sense of worry that hasn’t yet proliferated beyond the Valley. A few months back, top engineers at the AI labs were publicly saying they’d stopped writing code—claims that seemed at odds with most people’s experience, since the models still felt quite limited. Then, on February 5th, Anthropic released Claude Opus 4.6 and OpenAI released Codex 5.3, and there was a sea change in these models’ ability to do long-run, hands-off coding.

Internally, our engineers report they no longer write code—just orchestration—and in some cases are spending up to $1,000 per day in tokens developing GAIA, our internal AI system.

One tech CEO’s viral essay compared the current moment to February 2020: not the lockdowns, but the weeks before, when Covid was accelerating and most people were still shrugging it off.

“Nothing that can be done on a computer is safe in the medium term,” he wrote. The essay has drawn over 80 million views on X and may have contributed to the overall fear that pummeled the stock market recently.

And it’s going to accelerate further as these models begin to recursively improve themselves 24/7—first in the big labs, then into startups and large sophisticated tech companies. Incumbent industries will be much slower to adopt, not just because they lack the talent, but because they tend to have poor data hygiene, limited context for AI to operate, and data siloed across messy, heterogeneous systems. Getting AI into these companies will be like trying to drive an F1 car in a Baja race. Now compare that to an AI-native company that has legacy restrictions and can use agentic AI to its full potential.

The year of the agent: A new economy of recursive AI

AIs are also solving genuinely new problems in math and science. In January, OpenAI’s GPT-5.2 autonomously cracked several long-standing Erdős problems—including Problem #397, a 30-year-old conjecture about central binomial coefficients—generating proofs that were formalized in Lean and accepted by Fields Medalist Terence Tao.

Tao noted these represent “original proofs” rather than rediscoveries of existing literature, though he cautioned they remain “the lowest hanging fruit”—problems solvable with standard techniques, not profound breakthroughs. Still, the implications are clear: AI is now systematically harvesting the long tail of open mathematical problems that humans never got around to solving.

Then, just yesterday, OpenAI announced that GPT-5.2 had derived a genuinely new result in theoretical physics. Working with physicists from Harvard, Cambridge, the Institute for Advanced Study, and Vanderbilt, the model identified a previously overlooked kinematic regime where “single-minus” gluon scattering amplitudes are nonzero—overturning four decades of conventional wisdom that these amplitudes vanished. The AI spent roughly 12 hours reasoning through the problem, arriving at a simple, elegant formula and producing a formal proof.

Nima Arkani-Hamed called the findings “exciting,” noting that AI’s ability to “guess” the right formula represents a massive leap. The team has already begun extending the approach to graviton amplitudes—the particles mediating gravity—which, if successful, could bring us closer to reconciling general relativity with quantum mechanics.

In our own portfolio, Atinary just unveiled its human-out-of-the-loop self-driving lab in Boston. This is a system that can design experiments, run them, analyze the results, propose a new set of experiments, and repeat the process 24/7, speeding up discovery rates by up to 1,000x.

Attendees to the opening of the labs included MIT professor Stephen Buchwald, who will likely win a Nobel Prize one day for co-developing the Buchwald-Hartwig reaction. He had Atinary run an experiment using this reaction and called it “a miracle.” Scientists there had seen demos of other systems like Periodic Labs and Ginkgo that claim to do autonomous chemistry, but they said Atinary is the only one they’ve ever seen that can actually do it. Once you can speed up the physical world as we’ve done with the digital world, rate-limiting factors dissolve and everything starts to moves faster.

What we can expect for 2026 is that this will be the year of the agent. Just a few weeks back, an open-source project now known as OpenClaw went viral, 60,000+ GitHub stars in 72 hours.

The basic idea: you give an AI a dedicated computer with full access to emails, browsers, and coding tools, then let it iteratively and recursively go off into the world. Some users report (take it with a grain of salt) giving their bots $50 or $100, telling them if they blow through their token budget, they’ll be shut off. The bots then wrote arbitrage algorithms for Polymarket and woke up the next morning with over $3,000 in their accounts. One bot famously claimed to turn $313 into $414,000 in a single month exploiting 15-minute crypto prediction markets with a 98% win rate. In other cases, people have set up marketplaces where bots can pay humans to perform physical-world tasks for them. Think about it: there could be an entirely new economy of AI agents operating 24/7 with a “GDP” growing 100% week over week.

The dark horses: Why Google and Tesla are the long-term contenders

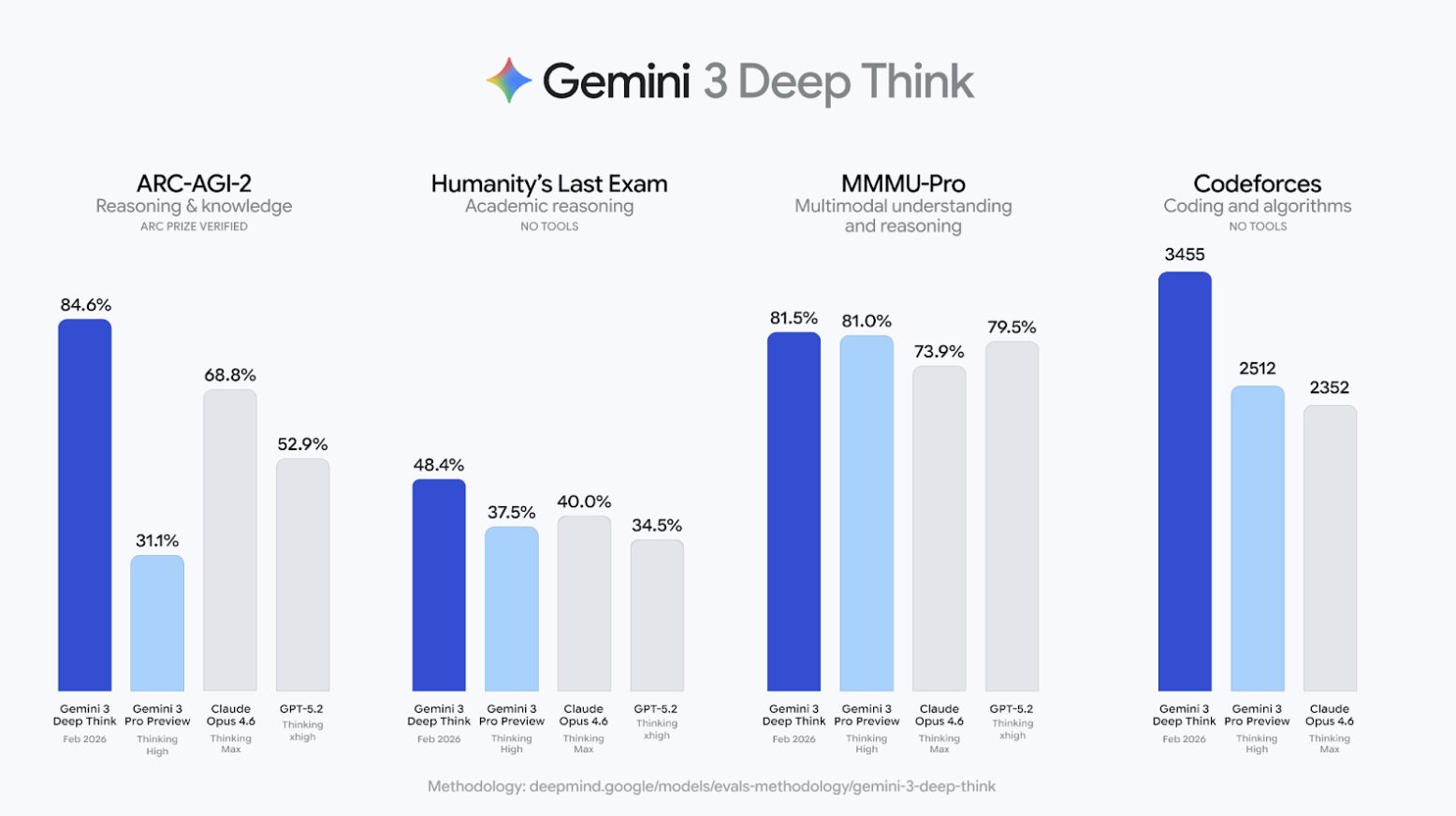

Today, OpenAI and Anthropic are the clear leaders, but I see Google and Tesla as the two dark horses that will come on late in the race. Google has the world’s largest data sources and the cash flow to outcompete anyone. They also have an incredible breadth of models spanning LLMs, video generation, science, and more—and I expect future models will integrate into a single world model. Below are the latest benchmarks from Gemini 3 Deep Think, which are absolutely crushing competitors in some cases. Expect Google to be a major player in 2026 and 2027.

Tesla should also have a big couple of years. If software commoditizes, greater value will accrue to chips, robots, and physical AI, and there is no company more advanced or capable of scale. Teslas are already driving without safety drivers or remote operators (unlike Waymo) in Austin, and Tesla is working on their own silicon.

They already have sophisticated world models developed for their cars, and they’re shutting down production of the Model S and Model X to make way for Optimus robots. No one else is even close.

Whatever 2026 brings, I urge all of you to lean into AI as much as possible so that you’re prepared for whatever comes.

Correction: An earlier version of this article included inaccurate characterizations of Verdant Robotics’ recent funding round, which closed earlier this year, oversubscribed. The relevant section has been removed.