“It is increasingly clear that private funding alone will be insufficient to fully fund first-of-a-kind cultivated meat facilities,” says The Good Food Institute (GFI) in a new report that highlights the industry’s “remarkable strides in reducing input costs” but acknowledges that private funding has almost dried up.

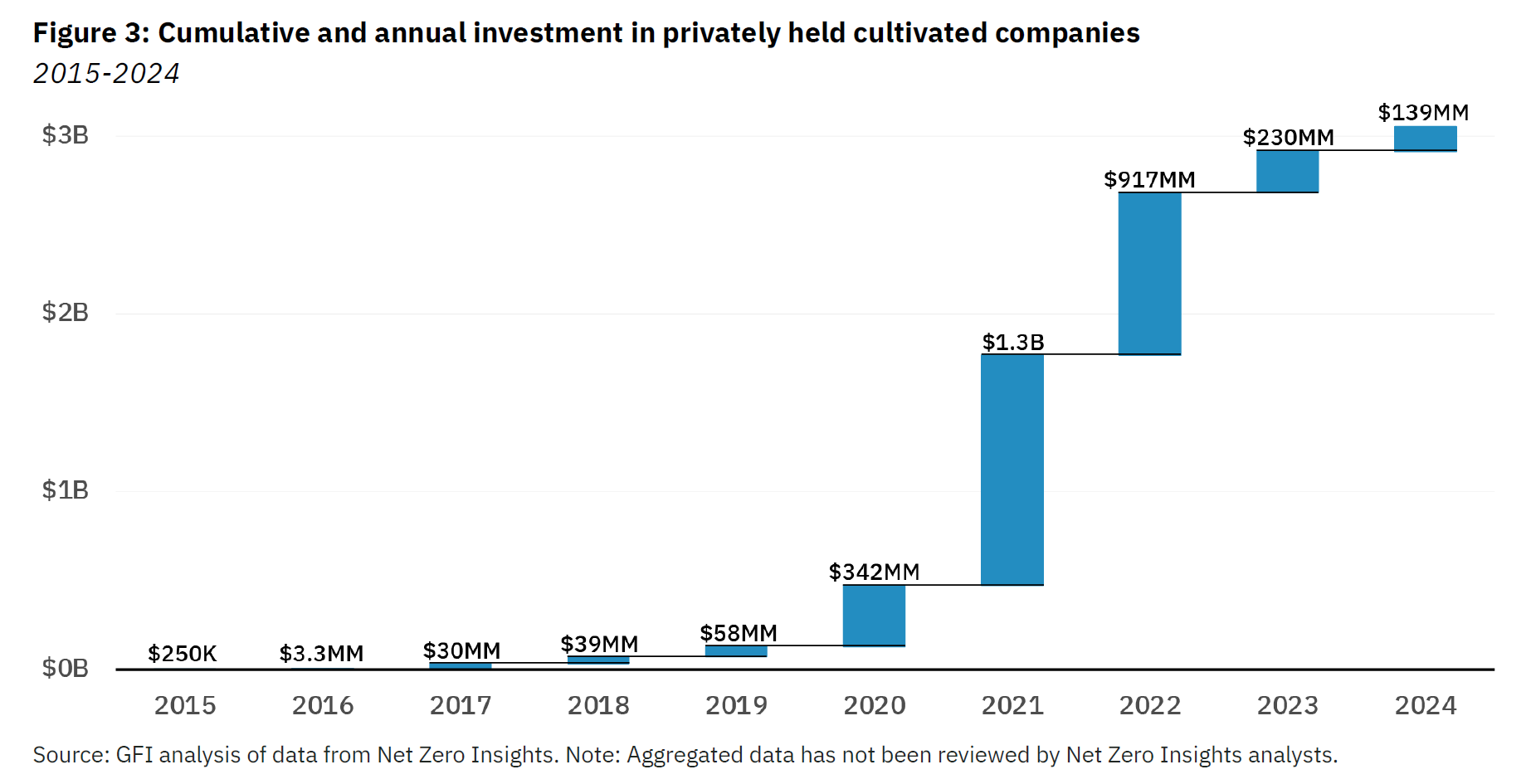

According to an analysis by the GFI (a think tank focused on accelerating the adoption of alternative proteins) and Net Zero Insights, cultivated meat and seafood companies raised $139 million last year, or just $84 million if you exclude a $55 million round from Prolific Machines, an optogenetics startup originally targeting cultivated meat that has since turned its attention to therapeutics.

This compares with $230 million raised in 2023, $917 million in 2022, and $1.3 billion in 2021, according to the GFI, which notes that little more than $3 billion has been pumped into the entire segment over the past decade, less than the amount of venture capital and private equity money invested in electric vehicles in the first three quarters of 2024 alone.

Top cultivated meat funding rounds announced in 2024:

- $43 million – Mosa Meat (Netherlands – muscle + fat)

- $10 million – Ever After Foods (Israel – bioreactors)

- $8.2 million – Ark (USA – bioreactors)

- $6 million – Simple Planet (South Korea – cultivated meat powder)

- $3.8 million – TissenBioFarm (South Korea – muscle + fat)

- $3.3 million – Innocent Meat (Germany – cultivated meat production system + recombinant proteins)

- $2.7 million – Cellva (Brazil – cultivated fat + plant cell culture)

- $2.6 million – Sallea (Switzerland – edible scaffolds).

‘No silver bullets to fill funding gaps in the cultivated meat sector’

Even if investor sentiment improves, however, it is unlikely to return to 2021 levels (when money was cheap and interest in alt proteins was sky high) any time soon, predicts the GFI.

“Venture capital is not typically well-suited to fund new facilities. As a result, companies looking to scale, especially via first-of-a-kind facilities, will likely need to identify alternative sources of funding.”

GFI’s recent Funding the Build report explores potential avenues for companies looking to scale such as equipment leasing, strategic partnerships, sovereign wealth funds, blended finance, and government programs, says the GFI. “Still, there are no silver bullets to fill funding gaps in the cultivated meat sector.”

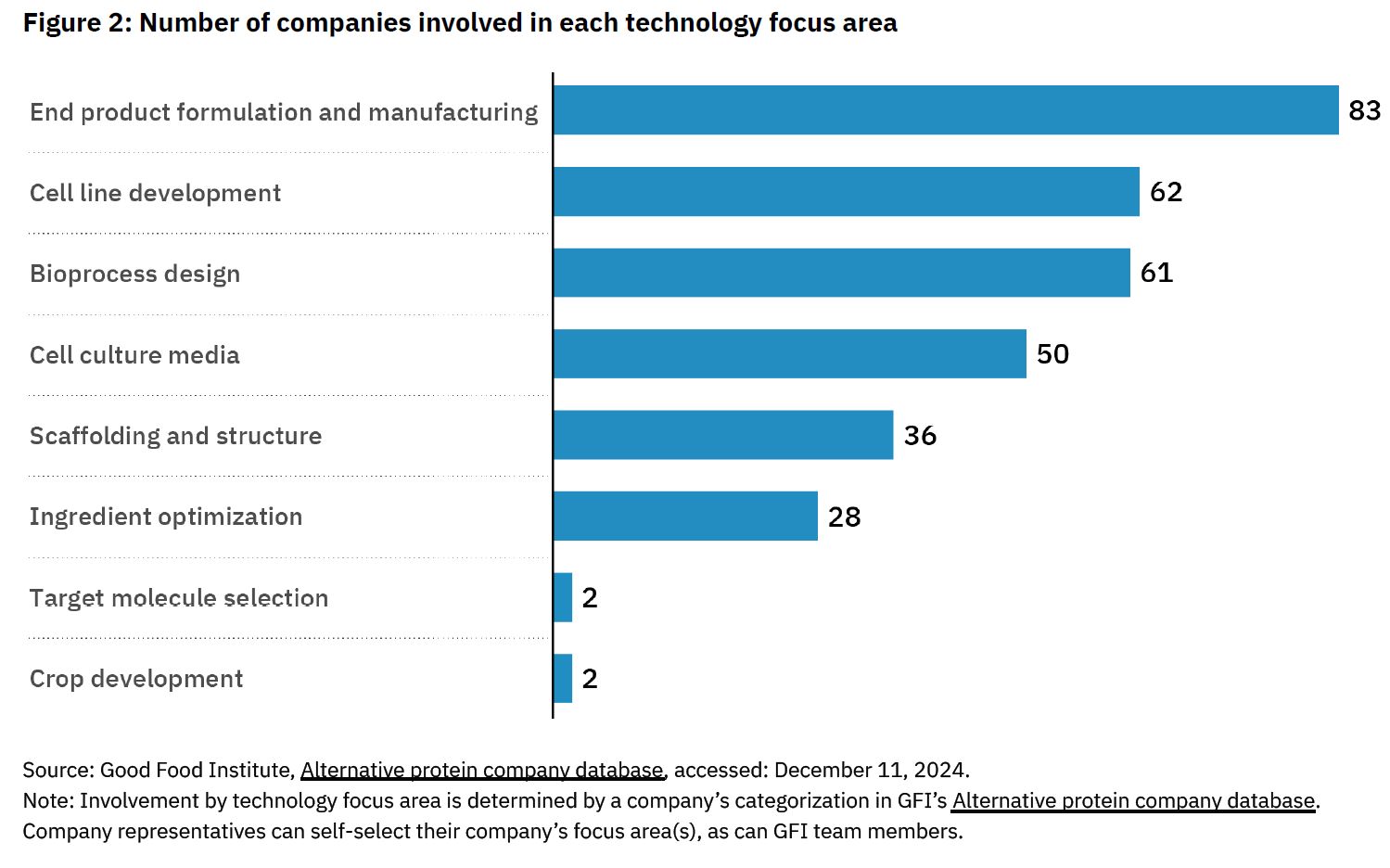

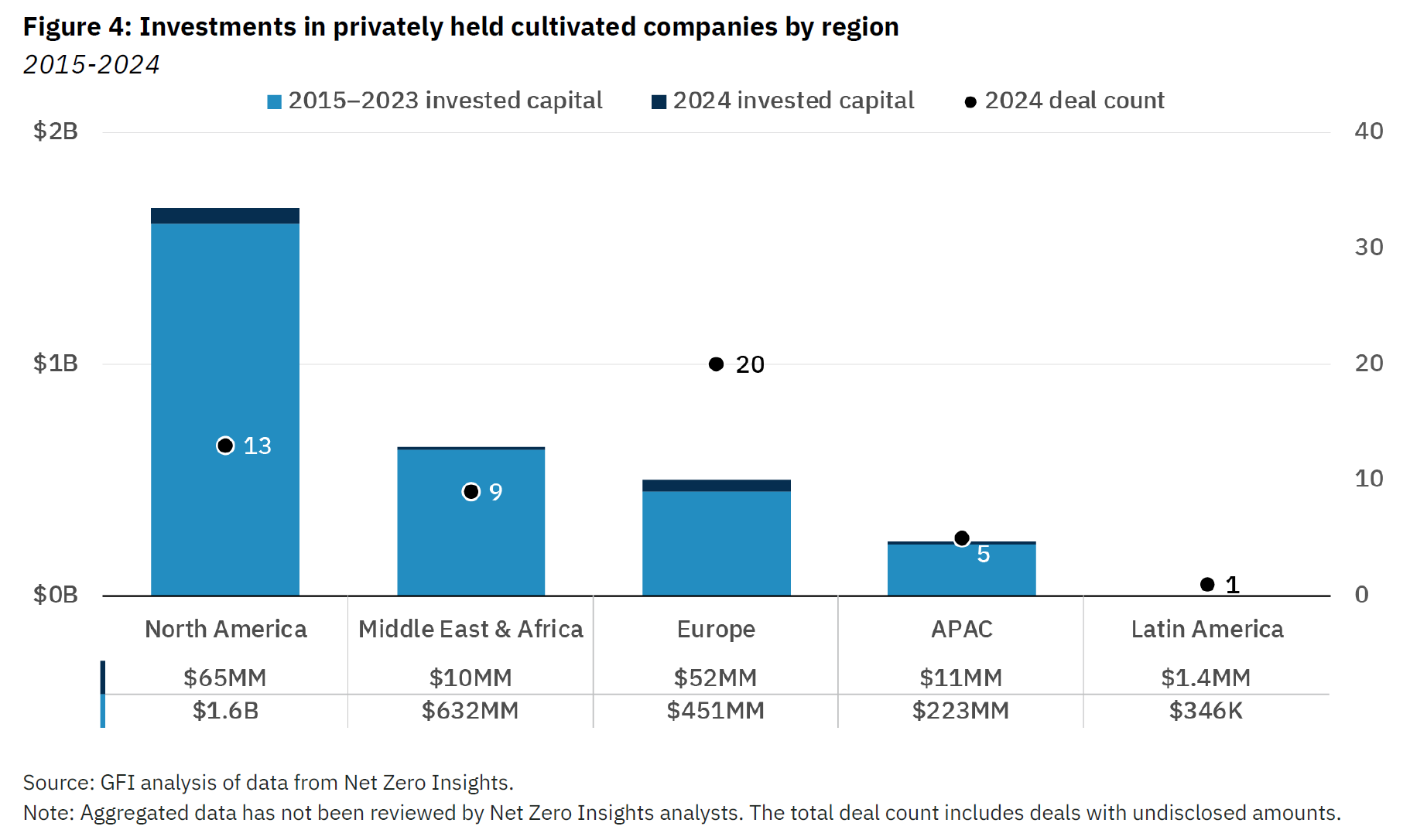

Meanwhile, those unable to access funding “will look to downsize, consolidate with other companies, or close,” says the nonprofit, which has 155 companies in its database “primarily dedicated to the development of cultivated meat and seafood inputs or end products.”

Public funding

On the plus side, while some governments have attempted to ban cultivated meat (Italy, Hungary, and some US states – with mixed results), governments in multiple jurisdictions have allocated money to cultivated meat research and innovation. China and India have made large commitments to develop domestic biotechnology capabilities, while Japan, New Zealand, Singapore, South Korea and New Zealand have funded public and private research to advance cultivated meat science.

The EU launched the FEASTS project to assess the role of cultivated meat and seafood in future food systems, while BBSRC and Innovate UK launched the National Alternative Protein Innovation Centre with £16 million ($21.4 million) of public investment.

Elsewhere, the Polish government provided a €2 million ($2.3 million) grant to cultivated chicken startup LabFarm and the Czech government awarded a €200,000 ($227,000) grant to Mewery for cultivated pork.

The Israel Innovation Authority awarded about $3.1 million for cultivated meat R&D, while Brazil invested a small sum to store cell lines for cultivated meat research and Massachusetts authorized $10 million for alt protein research grants and capital needs.

De-risking cultivated meat tech

However, a “category-wide shift in private capital tides likely requires a handful of cultivated meat companies to successfully de-risk their operations by increasing production, lowering costs, and demonstrating a path to profitability,” says the GFI.

“Companies made progress on all these factors in 2024, debuting cost-effective, animal-free media, introducing new bioreactors optimized for scaling adherent cell growth, and publishing studies demonstrating continuous manufacturing approaches leading to favorable economics at scale.”

But right now, the industry “is almost entirely pre-revenue” with just a handful of products sold in tiny quantities in three markets (the US, Singapore, Hong Kong), notes the report. “The number of consumers who have ever purchased cultivated meat is somewhere in the thousands. Meanwhile, billions of people worldwide regularly consume conventional meat.”

And while many commentators had expected that the top-funded players in the field would be selling meaningful quantities of product by 2025 following US regulatory approvals, some big names have delayed or scaled back plans in the past couple of years.

GOOD Meat, the first company to commercialize cultivated meat, has not yet landed on a model for profitable production at large scale, while UPSIDE Foods has paused plans to build a large-scale facility in Glenview, Illinois, in favor of expanding its smaller “EPIC” site in Emeryville, California and acknowledged its structured meat products are not yet scalable.

Meanwhile, Believer Meats, which is building what it claims is the “largest cultivated meat production facility in the world” in North Carolina, had previously said the site would be “operational by the end of 2024” but has not yet secured regulatory approvals to sell its products in the US or responded to questions about its progress in recent weeks.

Meatable, Mission Barns, Aleph Farms, Vow

On a more positive note, however, at least four production facilities in the cultivated meat sector opened in 2024, including Multus’ commercial-scale serum-free growth media facility in the UK, Nutreco’s food-grade cell feed production facility in the Netherlands, and BLUU Seafood’s pilot plant in Germany.

The Cultured Hub, a contract development and biomanufacturing facility launched by Givaudan, Bühler, and Migros, also opened last year in Kemptthal, Switzerland.

Meanwhile, Mission Barns unveiled proprietary bioreactors it claimed could dramatically improve the efficiency of its production process and secured an FDA ‘no questions’ letter regarding the safety of its cultivated pork fat, while Ever After Foods claimed its fixed bed bioreactors could also slash capex and opex costs.

Dutch startup Meatable today announced a partnership with TruMeat to set up a production facility in Singapore, while Australian startup Vow is now operating a proprietary low-cost 20,000-liter bioreactor and predicts it could soon be unit margin positive after securing the preliminary green light from regulators to market its cultivated Japanese quail products in Australia and New Zealand.

Finally Israeli cultivated meat startup Aleph Farms has secured regulatory approvals in Israel and unveiled modifications to its core technology that it claims will enable it to make whole cuts with fewer steps at lower cost.

Stepping back to look at the sector as a whole, “dramatic cost reductions in cell culture media are happening faster than anticipated,” claims the GFI report, which highlights a peer-reviewed study from The Hebrew University of Jerusalem and Believer Meats citing media costs of $0.63/L, a >99% decrease from a pharma-grade baseline.

The study also demonstrated how continuous production and reusable filters could reduce costs, while a techno-economic analysis from fellow Israeli startup SuperMeat that also featured a continuous manufacturing approach outlined favorable economics at scale, says the GFI.

Regulatory approvals

While it’s slow going, regulators in the US, Singapore, and Israel have now approved a handful of cultivated meat products for human consumption, while Food Standards Australia New Zealand (FSANZ) recently gave products from Vow the preliminary nod.

Some startups have also submitted dossiers to regulators in the EU and the UK (which has already approved cultivated petfood products from Meatly), while regulators in India, Brazil, South Korea and other markets are either accepting submissions or exploring how existing regulatory frameworks could accommodate cultivated meat.

Further reading:

Exclusive: Aleph Farms lands $29m to commercialize lower-cost whole-cut cultivated steak

Breaking: UPSIDE Foods engages in restructuring to stay ‘agile and efficient’

Inside the UK cultivated meat regulatory sandbox with Mosa Meat, Hoxton Farms, and BlueNalu

Breaking: Eat Just/GOOD Meat to pay ABEC $4.4m to settle legal dispute

Breaking: Mission Barns secures FDA approval for cultivated fat, gears up for US launch

ProFuse Technology expands focus from cultivated meat to drug discovery amid GLP-1 drug boom

Cultivated Meat at a crossroads: Highlights from the Tufts cell ag innovation day

![]()

Sign up for our weekly newsletter.