Earlier this week, we released the Europe AgriFood Tech Investing Report in collaboration with F&A Next, detailing $1.6 billion of investment to foodtech and agtech startups in 2018.

As part of our partnership and mission to foster a more cohesive ecosystem in Europe, we partnered with other local leaders to contribute data and insights. As a result, we believe this is now the most complete dataset on the European foodtech and agtech investment landscape today.

Thank you to our collaborators from across the region: Kevin Camphius from ShakeUp Factory, Johan Jorgensen from Sweden FoodTech, Alessio Dantino from Forward Fooding, and of course the teams at the founders of F&A Next – StartLife, Rabobank, Wageningen University and Anterra Capital.

Punching Below its Weight

Europe’s agrifood tech ecosystem raised just 9% of the funding that went to foodtech and agtech startups globally in 2018. When you think that the EU alone – excluding other European nations included in the reporting – represents about 20% of global GDP and it’s home to 12% of the world population, the region is clearly punching below its weight.

“Europe’s agrifood tech ecosystem is still young but much more active than you may think as the number of deals show; nearly as many deals closed in Europe as in the US, it just happens that most deals are mostly local with a much smaller dollar amount than in the US or in Asia,” says Kevin Camphuis from ShakeUp Factory.

Early Stage Emphasis

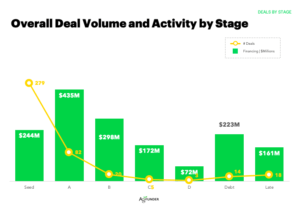

The good news, however, is that the number of deals closed grew 23% year-over-year to 423, and the majority of that activity took place at the earliest stages. Seed stage deals accounted for nearly 70% of deal flow in 2018 in Europe – compared to 55% globally – and 15% of dollars invested compared to just 4% globally.

This is good news as it highlights the increasing number of entrepreneurs entering the industry.

“The European food tech ecosystem lags other markets today. However, we have every reason to believe that a healthy funnel of promising earlier stage companies, growing investor activity and availability of corporate venture capital will close the gap rather sooner than later,” says Jeroen Leffelaar from Rabobank, another F&A Next founder.

While Europe’s food delivery startups were arguably the most mature globally — at least five of them have now exited to gain 7x returns in a five-year time period — there was an apparent lack in late-stage funding, which raises concerns that either financing is not available for startups to progress to later stages, or are failing before they can get there.

“Very few European startups have reached a level of maturity or geographical development that justifies the same amount of funding as most of the late stage funding you may compare them to,” says Camphuis. “But it’s changing, if you just look at three notable rounds, we’ve seen in France in the past six months, i.e., Ynsect, InnovaFeed, and Wynd. It’s clearly not a question of lack of investment as there is a growing number of big VC funds addressing Europe.”

Upstream on the Up, Downstream Downturn

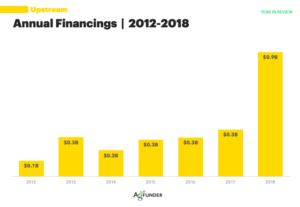

While the maturation of several food delivery startups contributed to a 50% drop in downstream funding, startups operating on the farm or in the supply chain before the retailer, raised 200% more in 2018 than 2017, reaching nearly $1 billion and representing 56% of total funding. While our reporting might be slightly improved in 2018 due to our new data partnerships, there’s no doubt upstream innovation is rapidly picking up steam. For those of us somewhat fatigued with yet another food delivery service, this is refreshing, particularly as they continue to thrive in the US and Asia and dominate the funding landscape.

While the maturation of several food delivery startups contributed to a 50% drop in downstream funding, startups operating on the farm or in the supply chain before the retailer, raised 200% more in 2018 than 2017, reaching nearly $1 billion and representing 56% of total funding. While our reporting might be slightly improved in 2018 due to our new data partnerships, there’s no doubt upstream innovation is rapidly picking up steam. For those of us somewhat fatigued with yet another food delivery service, this is refreshing, particularly as they continue to thrive in the US and Asia and dominate the funding landscape.

Furthermore, funding to European upstream startups — which include Ag Biotech, Farm Software & Robotics, Midstream Tech, Innovative Food, Biomaterials, Novel Farming Systems, and Ag Marketplaces — raised a respectable 13% of the global upstream total, and all categories at least doubled the amount of investment they raised.

Diversity Draw

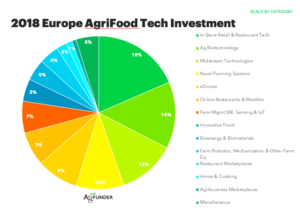

Broadly the European agrifood tech ecosystem is much more diversified than globally, where three downstream categories — restaurant delivery, grocer and retail tech — accounted for over half of investment in 2018.

In Europe, funding was much more evenly split across categories with some clear strengths too.

While removing an outlier deal in the retail tech category would push it below Ag Biotech, we’ve seen an acceleration in innovations for restaurants and retailers as they face challenges such as labor shortages, regulation, and competition from e-commerce! It was also the most active category by the number of deals.

Ag biotech is particularly active and relatively mature in Europe, which is unsurprising as home to some of the world’s largest crop inputs suppliers, and some of the world’s leading agricultural science institutions including our partner Wageningen. With the news last week that Monsanto (now Bayer) was ordered to pay $2 billion in damages to a couple who claimed Roundup weedkiller gave them cancer – and more trials to come – the large agribusinesses and farmers will be keenly looking for further acceleration in alternative crop inputs. Startups in this category in Europe are developing plant breeding, gene editing, biologicals, and microbial solutions.

Proportionally, Europe has a greater footprint in Novel Farming Systems – including indoor ag, insect farming, and aquaculture systems – than globally where it represented just 4% of funding in 2018.

Insect farming is particularly advanced in Europe with a few startups in scaleup mode for the animal feed industry— especially France where Innovafeed mobilized $65 million across two rounds in 2018 and Ynsect closing a record-breaking deal this year of $125m.

Farm management software sensing & IoT is another strength in Europe – for crop farmers and livestock farmers as well as aquaculture. Innovations run the gamut from computer vision in beehives to remote sensing to underwater cameras and more.

It would be remiss not to mention alternative proteins and innovative food in the wake of Beyond Meat and Impossible Foods’ stellar deals recently although globally and in Europe, these Innovative Food innovations are still a small portion of the overall pie (5% of total funding).

In Europe, there are some notable startups including Mosa Meat, which was founded by the first cultured burger manufacturer Mark Post in the Netherlands. There are a few alternative functional ingredients companies too like Stem one of our portfolio companies with a sugar replacement tech.

But in this category – and biotech – Europe does have challenges revolving around the regulatory environment; last week there was a headline around the EU wanting to ban the use of term burger and sausage for plant-based goods, and the EU’s strict stance on gene-editing is a source of much contention. Both of these regulations could hamper innovation, or even result in a positive for the UK if/when it exits the union.

Geographical Split

The UK and France contributed nearly half of total funding (45%) and 40% of deal flow in Europe’s agrifood tech market in 2018.

“We are proud to be cultivating a varied and diverse agrifood tech industry, united in the aim of improving the quality and sustainability of food and food production throughout the value chain. In addition, we are seeing government-back initiatives such as Innovate UK delivering millions of pounds of funding and resources to support PhDs and agrifood tech entrepreneurs kickstart their ventures,” writes Alessio Dantino from Forward Fooding in the report.

On France, Kevin Camphuis writes “France is a large market with strong consumer demand for innovation, a deep culture for food preparation, seasoned agri and agro know-how, and one of the most diverse corporate and retail ecosystems, from farm to shelf, including global leaders. And early 2019 shows clear signs of acceleration with as much funds raised over the three first months of 2019 as in full-year 2018.”

Spain’s total was bolstered by an outlier — delivery tech company Glovo, which raised a $129 million Series C round — though it was still the fourth most active market for deals closed.

While low on the leader board for total funding, Italy contributed the third highest number of deals in 2018. Its median deal size was only $400,000. Seed stage deals claimed 28 out of 31 total funding rounds, pointing to Italy’s nascent agrifood tech industry.

Two midstream tech deals over $30 million pushed Ireland’s totals up, while Nordic countries contributed more deals, mostly at the seed stage.

“A focus on health and sustainability drives innovation in the Nordics,” says Johan Jorgensen in the report.

Eastern Europe has yet to make strides in agrifood tech, though there are some leading farmtech startups, such as Agrivi out of Estonia.

Investor Insight

While local commentators complain about a lack of investors for the industry, some 603 investors participated in 2018, again representing around 30% of the global investor base in agrifood tech.

“Indeed, more multistage investors are entering the Agrifood space, and in our programs, we have been (fore) seeing and driving the trend for more high-quality agtech startups,” says Jan Meiling from StartLife, a founder of F&A Next.

If there’s another key takeaway from the roster of investors closing food and agtech deals in Europe, it’s that few are wholly dedicated to the sector (at least geographically.)

Out of 603 active investors in 2018, 498, or 83%, made only one investment in Europe’s food and agtech sector. Thirteen percent (13%) made two investments, while only 5% made three or more.

Generalist investors topped the list of most active investors in Europe’s food and ag sector.

The most active investor by deal number in Europe’s food and ag sector was UK-based crowdfunding platform Crowdcube, which backed more than 180 companies across a range of industries in 2018, 13 of which were in agrifood tech. Funding rounds ranged from a couple hundred thousand dollars to several million.

Bpifrance, a France-based entrepreneur-focused bank, and Kima Ventures, the global angel investor network, were also among the most active in Europe’s food and ag tech space, closing six or more deals in 2018.

Seraphim Capital was a notable exception to the generalist-funder trend. The UK-based space tech-focused investment firm invested in six companies involved in the food and ag sector via remote sensing technologies. For example, Finland’s satellite imagery company ICEYE is one of Seraphim’s portfolio companies.

Find out more about the top deals in each category, and the investors, startups, and technologies driving Europe’s agrifood tech ecosystem in the free 67-page report here.