[Disclosure: AgFunderNews’ parent company is AgFunder.]

VC investment to consumer-facing sectors continued to fund primarily restaurant tech and anything related to food delivery in 2025. Funding declined across the whole downstream sector, in keeping with agrifoodtech funding overall. eGrocery is once again the top-funded downstream category, but this time with less of a lead over other categories than in years past.

The AgFunder team will present full investment figures for 2025 in the coming months with the launch of its annual Global AgriFoodTech Investment report, including total funding for the year.

In the meantime, the preliminary numbers tell us who is raising capital right now and what to keep an eye on in 2026.

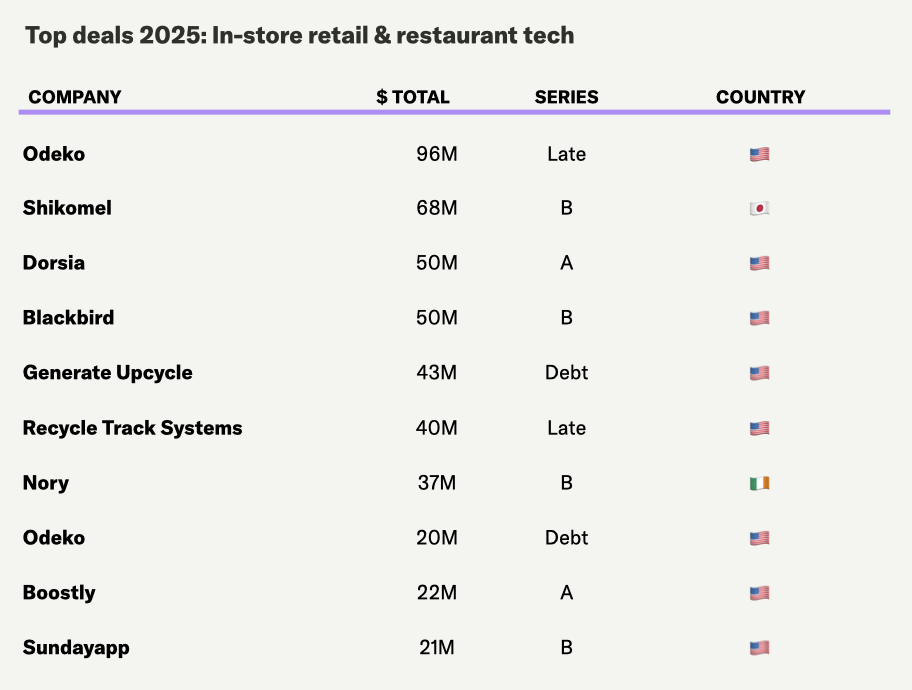

What’s up: In-store retail & restaurant tech

Funding in 2025: $743 million

Deal count: 112

Why it matters: Platforms that manage inventory and operations (Odeko, Nory) continue to garner capital as restaurants and cafes look to bring costs down. This is the first year since 2016 that the entire in-store retail & restaurant tech category raised less than $1 billion (based on preliminary data that could change as final deal numbers come through).

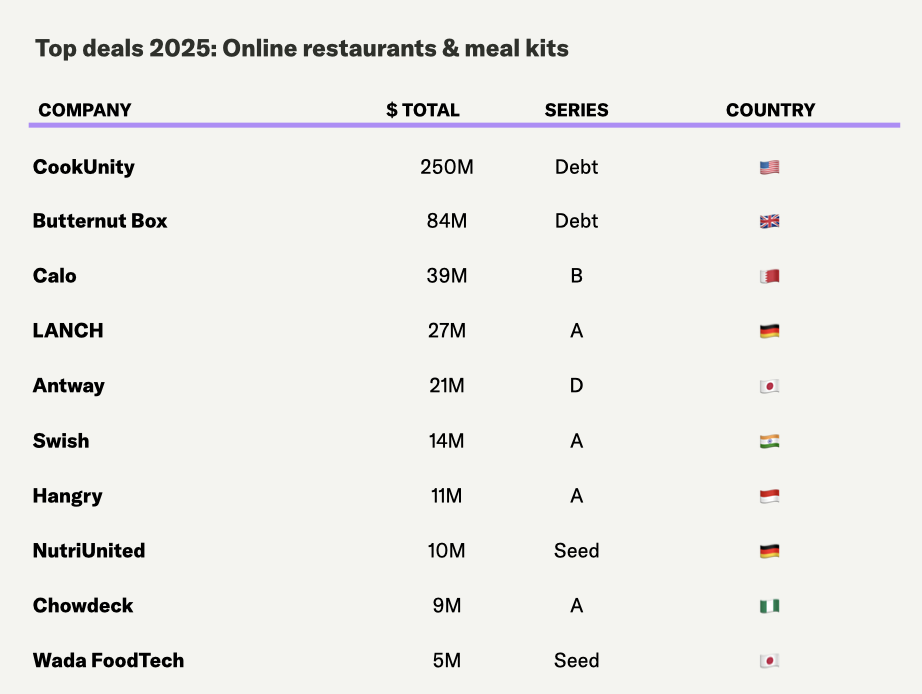

What’s down: Online restaurants & meal kits

Funding in 2025: $500 million

Deal count: 45

Why it matters: Half of this category’s total funding went to a single round, while another large chunk went to a pet food delivery company (Butternut Box). Food delivery apps are still a booming business all over the world, but a handful of now-public companies (DoorDash, Delivery Hero, etc.) control the bulk of these markets.

What’s debatable: eGrocery

Funding in 2025: $925 million

Deal count: 49

Why it matters: eGrocery was the top-funded category in 2025, a status it has kept for a number of years now among consumer-facing categories. However, total funding to the category dropped 63% year over year, while deal count dropped around 37%. Absent Zepto’s mega-raise, eGrocery would land next to last in funding to downstream categories.