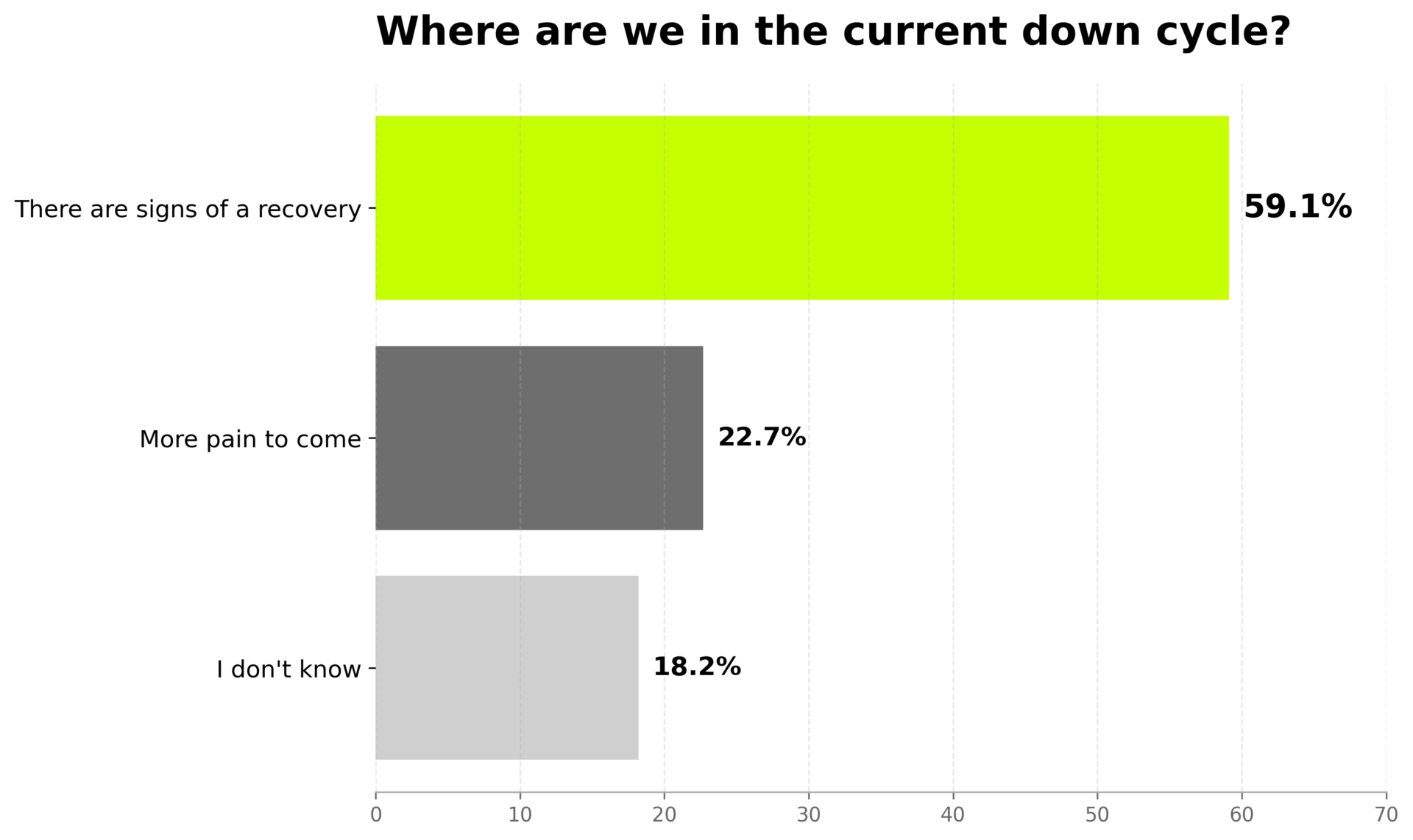

If 2025 was characterized by “chaos and uncertainty,” buckle up, say agrifoodtech investors we quizzed ahead of our global investment report In 2026 we could be in for an even wilder ride, compounded by tariff uncertainty, extreme weather, and war in the Middle East.

On top of that, throw in AI, which is both exciting and hugely destabilizing, notes AgFunder* partner Rob Leclerc, PhD: “AI is starting to create covid-level anxiety for people closest to it. That will spread.”

Antony Yousefian at UK-based investor The First Thirty, who is bullish about the potential of AI to “remove large technical barriers that have existed in ag and food,” also warns of a “private equity correction triggered by AI’s rapid destruction of old-economy business models, which narrows exit pathways and keeps early-stage funding constrained.”

At the same time, AI could prove transformative, he predicts.

“Physical AI agtech” could “draw a lot of capital and bring back ‘tourist’ VC. We’re excited about founders capturing primary data at field and supply chain level enabled by edge AI, robotics, IoT that now work autonomously.”

Several respondents in our annual investor survey say AI is now moving from promise to practical deployment, with Francisco Jardim at São Paulo-based SP Ventures predicting opportunities across the industry to remove the “friction between humans and complex data systems” via natural language interfaces.

Crucially, AI is now shifting “from models to applications embedded in workflows,” says Maarten Goossens at Netherlands-based Anterra Capital. “Agrifood is one of the largest ‘real economy’ opportunity sets where workflows are still under-digitized so ROI is unusually tangible.”

Looking further ahead, Leclerc believes the next wave will be driven by agentic AI: “2026 is going to be the year of the [AI] agent. It may not hit agtech for 1-2 more years but it’s coming and we’re going to see an entire internet for agents, which is going to deeply disintermediate traditional commercial channels.”

As always, however, the ‘garbage in, garbage out’ mantra applies, says Ali Morrow at Clay Capital: “AI is only as good as what it’s trained on.”

* Disclosure: AgFunder is AgFunderNews’ parent company.

Capital flows and the role of corporates, sovereign wealth funds

In the meantime, money remains tight, say investors, who point to a widening Series B-C funding gap, agtech’s “valley of death.”

According to long time investor and independent advisor Mark Brooks: “I expect capital to further concentrate, with the middle—after seed, before growth—being squeezed the most. I also expect more secondaries as funds reach the end of their cycle and need liquidity.”

Ali Morrow at Clay Capital adds: “The funding gap in the middle of the capital stack hasn’t closed. Series B and C remain genuinely hard, and there aren’t enough growth-stage investors with the patience and sector literacy this space requires. Corporates are the most realistic exit option for most of our portfolio, but they’re navigating their own margin pressure and restructuring.”

Against this backdrop, Jason Silm at Cibus Capital expects strategic capital from sovereign wealth funds and government-backed entities to play a greater role.

Other investors we polled believe corporates should play a bigger role in filling funding gaps, meanwhile.

Gentiane Gorlier, PhD, at The Yield Lab, for example, says corporates should provide “credible demand signals, not just innovation theatre,” via co-development projects with clear procurement pathways, commercial pilots tied to scale clauses, minority investments where strategic value is real, and “helping with distribution and validation: the two biggest bottlenecks.”

Morrow at Clay Capital adds: “The best thing a corporate can do is validate a startup’s solution on a timeline that actually works for the startup — not an 18-month procurement process that consumes half its runway before a PO is issued. Both sides can do better at scoping engagements: clear goals, a realistic timeline, and a defined commercial pathway from the start. CVC has also played a useful buffer role where pure VC has retrenched, but capital without commercial commitment doesn’t move the needle much.”

Jaap Strengers Future Food Fund, in turn, says corporates need to provide “patient capital for series A/ B+ in areas where VCs with closed end funds struggle,” while Mark Durno at Rockstart urges them to “spread their access throughout fund allocation.” As an LP, he claims, “They will get better exposure and access for M&A later, and do not risk crushing the company during scaling.”

Tomás Peña at The Yield Lab LATAM, also urges corporates to “develop more fund of fund strategies [investing in other investment funds rather than directly in companies].”

Exits… look to Hong Kong and India for IPOs?

But exits remain the biggest question mark for the sector, which has returned little capital to date. As potential acquirers, the big strategics are distracted with internal issues or unwilling to pay 2021 valuations, while most agtech fundamentals are not yet attractive enough to bring in public market investors or private equity buyers, notes PJ Amini at Leaps by Bayer.

“While there have been signs of early consolidation and selective M&A, 2025 did not deliver broad rollups or truly category-defining exits,” says Jardim at SP Ventures. “Valuation gaps between buyers and sellers, lingering macro uncertainty, and a cautious stance from strategics slowed large transactions.

“Instead, the year was more about groundwork: companies strengthening fundamentals, cleaning up balance sheets, and positioning themselves for consolidation once confidence, pricing, and capital conditions align more clearly.”

The picture looks a little different in China, however, where there was a flurry of M&A activity, says Matilda Ho at Shanghai-based Bits x Bites: “Longping’s Lantron Seed alone acquired three companies in just two months with state-backed capital. Meanwhile, policy-backed IPOs in AI and robotics elevated Hong Kong to the world’s largest IPO market, unlocking a surge in agrifood tech listings and setting the stage for a stronger exit environment in 2026.”

“What excites us most about 2026 is the return of systemic liquidity, fueled by pro-growth national policies and support from state-backed ‘patient capital’ in China. We see this year not just as a recovery but as a transition to a more resilient, exit-focused investment cycle. We’re encouraged by the reopening of strong exit opportunities through HKEX Chapter 18C and the STAR Market, especially in sectors like AI, robotics, and biotech. With the 15th Five-Year Plan giving us a fresh boost, 2026 looks like it will be a good year for high-tech IPOs and a big wave of industry consolidation.” Matilda Ho, Bits x Bites

Mark Kahn at Omnivore, who is particularly excited about biomaterials, full-stack CDMO, and robotics in the coming years, expects that “in the next year or two, you’ll see the first IPOs in the space” in India, meanwhile.

According to Durno at Rockstart, mealtime platform Wonder Group is “a likely front-runner for IPO in the not-too-distant future,” although in general he says, companies need better access to growth capital: “There are not enough Series B+ rounds to drive exciting exits yet.”

For Michael Lavin at Germin8 Ventures, this has prompted a broadening of his firm’s aperture to include life sciences, “where there is a more exit-rich environment and tech transfer opportunities highly relevant to agrifood.”

Even so, investors remain optimistic about several areas they believe are poised to attract capital in the next investment cycle, with 2026 all about “turning validated technology into scaled, durable businesses,” predicts Jardim at SP Ventures.

“Agrifoodtech is poised to benefit as science moves closer to market. AI-enabled biology is advancing from lab validation to real commercial adoption through clearer regulatory and go-to-market pathways. Startups are entering the year leaner and more disciplined, with stronger unit economics and more realistic scaling plans.

“Meanwhile, strategic capital is returning driven by concrete strategic needs rather than optional innovation bets.”

Hot areas: Midstream tech, farm robotics, ag biotech

Looking ahead to 2026/27, says Goossens at Anterra Capital, “Midstream technologies will lead: the biggest checks will flow to workflow-native platforms that digitize and automate the messy middle of the value chain.”

Jardim at SP Ventures, meanwhile, reckons farm robotics will attract the largest share of capital, driven by AI, labor scarcity, and continued progress toward supervised autonomy and fully autonomous systems.

“Solutions that tightly integrate hardware, computer vision, and software with clear on-farm ROI should lead investment activity,” he says.

“Alongside this, ag biotech is likely to continue capturing significant capital, particularly platforms leveraging in silico design to accelerate discovery, reduce development costs, and improve regulatory efficiency in biologicals and biotech. Other categories, including Farm Management Software, Sensing & IoT, should also benefit as adoption increases through more intuitive, AI-driven and user-friendly tools.”

Investors’ pet peeves:

As for pet peeves, what brings out investors’ inner Grinch?

– “AI sucking up all growth capital globally.” Mark Kahn, Omnivore

– The AI-ification of all decks. Of course AI is having an impact, and there are real opportunities in food and ag for this technology to create value. However, the sector’s fundamental problem is a lack of digitization and a lack of clean data — you can’t build durable AI value on top of that.” Ali Morrow, Clay Capital

– “Aggressive lead investors… leave something on the table for early backers or they won’t come back and create deal flow for you in future. We need pre-seed/seed investors.” Mark Durno, Rockstart

– “Companies still receiving valuations as if they can exit at unicorn levels.” Jaap Strengers, Future Food Fund

– “AI decks with no data access plan, ‘platform’ claims without a wedge, climate buzzwords with unclear buyers, pilots presented as revenue, founders who dodge questions on gross margin, payback, and churn.” Gentiane Gorlier, The Yield Lab

– “Regenerative agriculture is now a buzzword picked up by CPGs and other corporations, which has, as per usual, bastardized the meaning and power of the concept a bit.” Kalob Williams, LANCRY Natural Capital

– “The UK continues to be a disappointment in terms of quality founders and the speed at which they grow their business plans. This isn’t necessarily their fault; there is so little money going into tech in general in this country. Institutions need to allocate all the way down the curve if they want growth.” Stephanie Mathern, The First Thirty

– “Investors who write off agrifood as a category because a few highly visible themes underperformed.” Maarten Goossens, Anterra Capital

– “Seeing pitches where AI is presented as the product rather than a tool. Also, the “tourist” mindset of some investors who expect Silicon Valley returns without understanding the biological cycles of agriculture.” Tomás Peña, The Yield Lab LATAM

– “’AI buzzword’ paired with ‘open-source data.’ This does not make a defensible venture case.” Mark Durno, Rockstart

2025 agrifoodtech investing in three words:

Asked to summarize agrifoodtech investing in 2025 in two or three words, here are some of the responses we received:

- No new money

- Too f**king slow

- Show me revenue!

- Internalizing market reality

- Disciplined, selective, resilient

- Disciplined, fundamentals, opportunity

- Almost impossible

- Consolidation, hesitation, first signs of new real businesses

- Back to basics

- Inside rounds

- Walls to studs scrutiny

- Not for me

- Austere, selective, execution-driven

- Doing just fine

- Dead cat bounce

- Flat like pancake

- Varied, volatile, inflection point

The most surprising things about 2025 in the agrifoodtech industry:

– “How quickly agrifoodtech shifted from narrative-driven innovation to fundamentals-driven execution.” Francisco Jardim, SP Ventures

– “How quickly climate investing in the US retrenched across the board.” Maarten Goossens, Anterra Capital

– “We saw a lot of geopolitical turbulence and unpredictable trade barriers—like the on-and-off rules around drone trading and the sudden tightening of GRAS standards—turning regulatory and asset-security risks into headaches for every deal. At the same time, climate change went from being a distant worry to a real pain for supply chains, causing some serious price spikes, especially in categories like coffee and matcha. 2025 really showed us that volatility is the new normal.” Matilda Ho, Bits x Bites

– “The speed at which fintech and agtech merged. The ‘agfintech’ space showed that financial inclusion is the true enabler for technology adoption in emerging markets. This is a natural next step for AI-driven risk models.” Tomás Peña, The Yield Lab LATAM.

👉 Checkout the latest interviews in our Investor Q&A series.