By now, we’ve rehashed agrifoodtech’s post-2021 correction so many times we’ve run out of ways to describe it. Funding winter. Trough of disillusionment. Market rationalization. Pick your preferred cliche.

It’s time to move on.

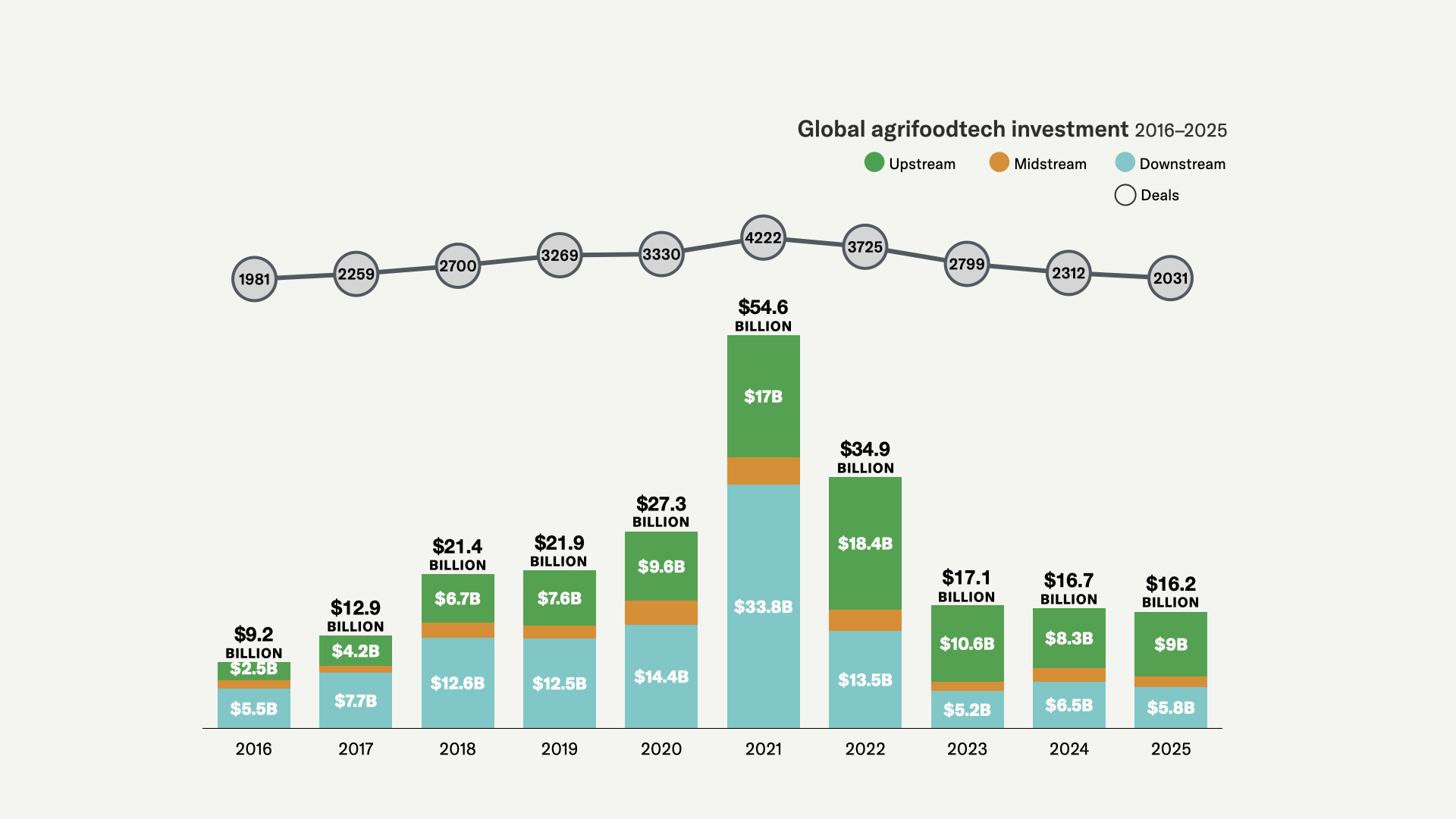

AgFunder’s Global AgriFoodTech Investment Report 2026 confirms what everyone already suspects: global funding is flat at $16.2 billion, deal count fell 12%, and nobody reading this is surprised.

And yet food systems have never been under more pressure. Trade tension and geopolitical conflict are redrawing supply chains in real time. Climate volatility hit coffee, cocoa, and grain prices hard in 2025. Water stress, soil degradation, and labor shortages aren’t waiting for the funding cycle to recover. The problems are accelerating, and the capital is being more selective about which solutions it backs.

That selectivity is the real story of 2025.

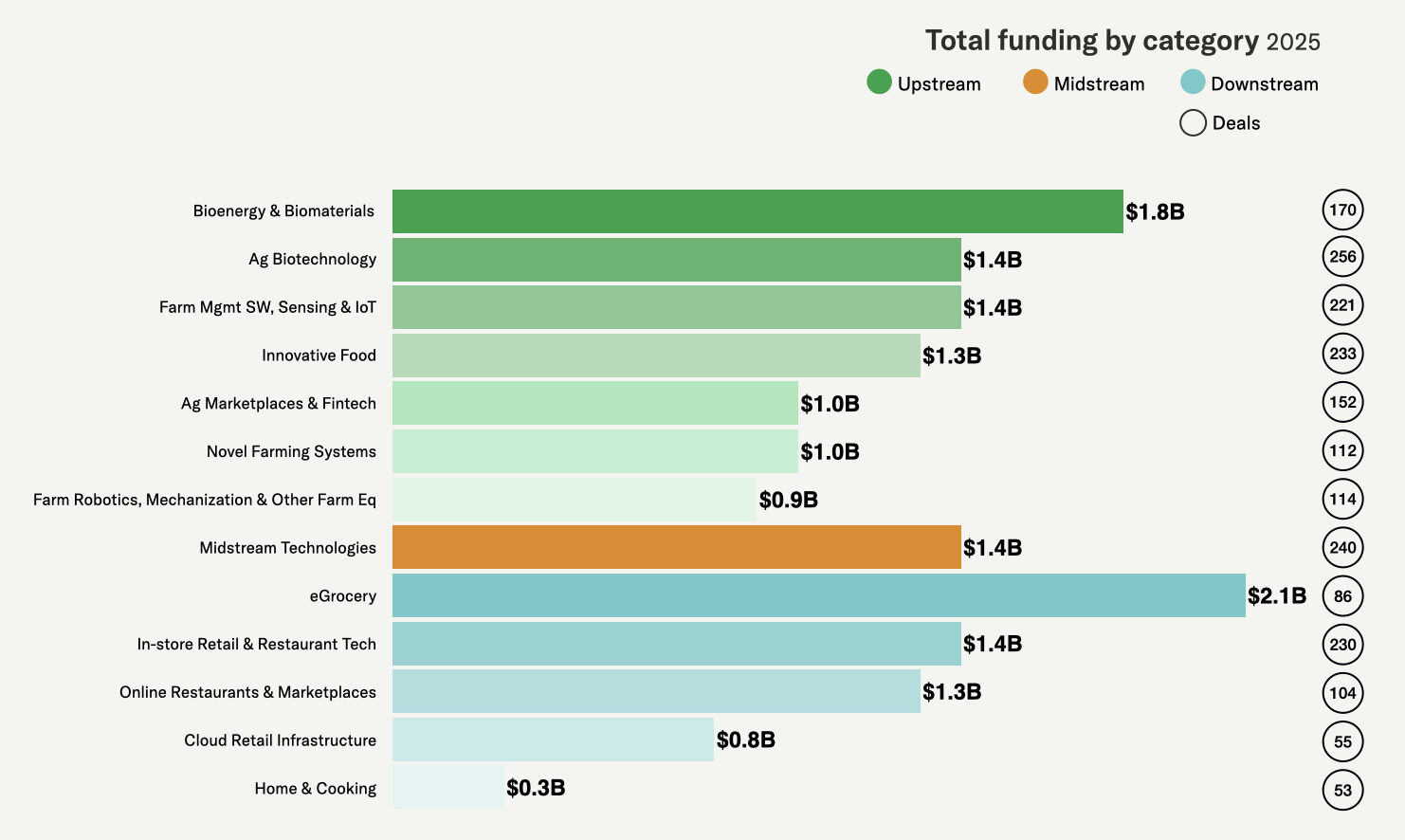

The money moved upstream

Upstream startups—those working on farms and in food production—drew $9 billion in 2025, up 7% year over year. Downstream categories, dominated by eGrocery and food delivery, continued to shrink. Wonder’s $600 million Series D was the year’s largest deal. In 2021, it would have been a footnote.

The era of $3 billion mega-rounds for grocery delivery apps is over. The largest deals in 2025 were 35% smaller than 2021’s top-tier rounds. Generalist investors have largely left the building.

What replaced them is more interesting. Debt financing hit 18.2% of total agrifood funding, its highest share in a decade. Companies like Chestnut Carbon ($370 million across two rounds), Cambrian Innovation ($150 million), and Samunnati ($267 million) raised through debt and late-stage instruments rather than traditional venture equity. This could be read as a sign of distress, but it’s also a sign that some agrifoodtech companies now have revenue profiles that debt investors can underwrite.

The share of deals going to first-time-funded companies ticked up to 46% after years of decline with new logos entering the pipeline again. Whether they can raise follow-on rounds in this market is the next question.

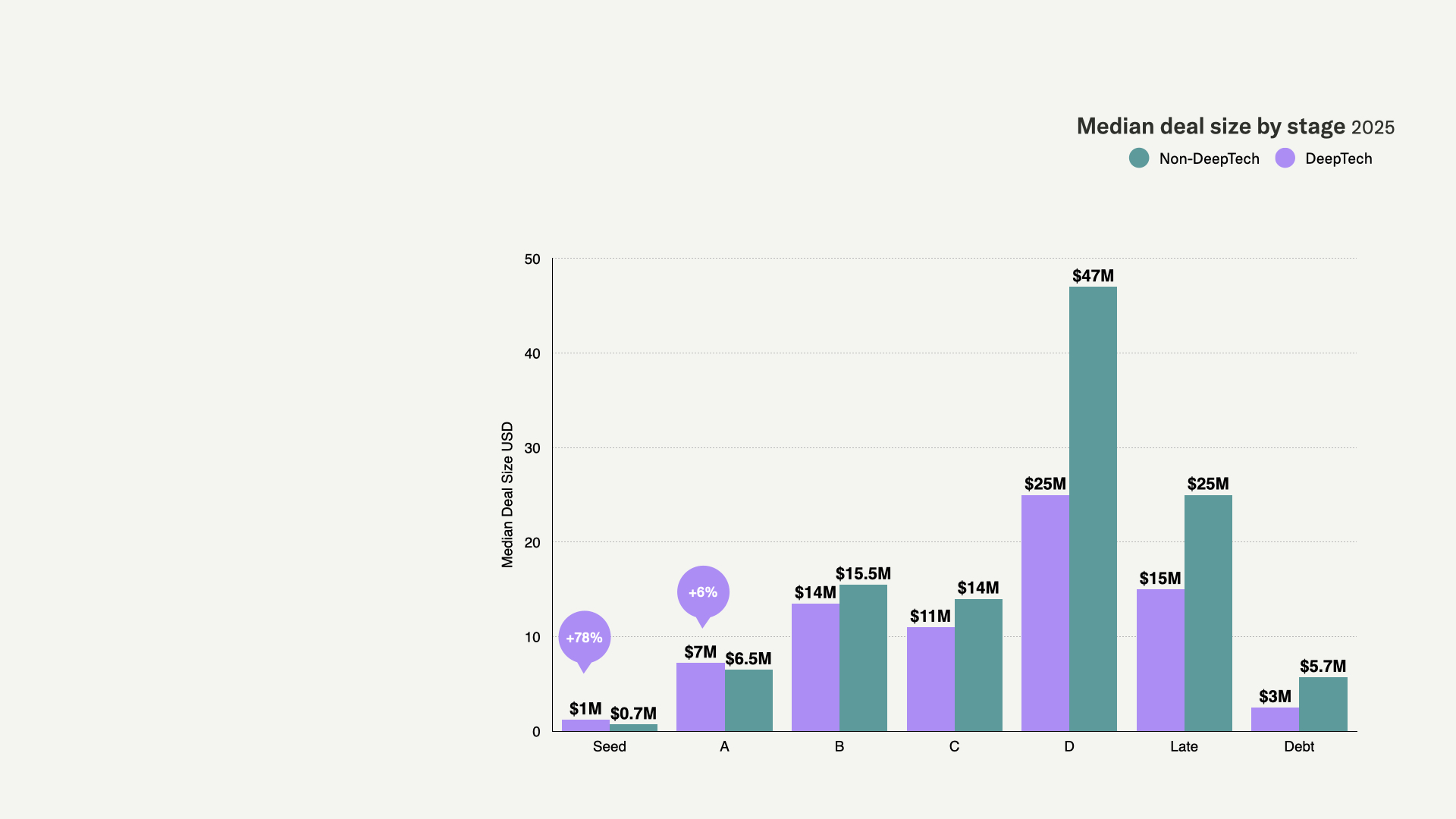

The deeptech premium—and where it disappears

For the first time, this year’s report breaks out deeptech as a distinct layer of analysis, and while modest, there is an uptick in deeptech investment activity in agrifood.

Deeptech’s share of agrifoodtech deals has climbed to 32% from 22% over the past decade. At the seed stage, deeptech rounds close at a 78% premium over non-deeptech equivalents, which means investors are paying more to back science-led companies early.

But the premium vanishes at Series B and beyond. No deeptech agrifood company broke $200 million in a single round in 2025. Seven non-deeptech companies did.

The pattern makes sense if you remember what happened last time. Five of the 33 deeptech companies that raised $200 million+ rounds between 2019 and 2022 have hard-failed, according to analysis we did with data from The New Bioeconomy, all in Novel Farming or Innovative Food. Growth investors got burned and they haven’t forgotten.

Since 2021, deeptech funding in agrifoodtech fell 62% while total agrifoodtech funding fell 70%. Non-deeptech fell 73%. Deeptech held up better, but the growth-stage gap remains wide open. Bridging it is the central challenge for the sector in 2026 and beyond.

What to watch

Agrifoodtech is not going to produce a banner funding year in 2026, but the composition of capital continues to shift in ways that matter.

Climate tech within agrifood recovered to $3.9 billion from $2.8 billion in 2024; China grew 43%, driven by state-backed biotech investment; South Korea surged 171%. Farm robotics deal activity held steady while almost every other category’s deal count fell.

The market has reset. The companies still standing are building against real constraints—soil, biology, supply chains, physics—that create natural defensibility. The question is whether the capital markets will meet them at the scale they need.

Download the full report [here] to find out:

- Why deeptech rounds close at a premium at Seed but not at Series B

- Which two countries allocate nearly half their agrifood funding to deeptech

- The category where 97% of deals qualify as deeptech

- What the failure pattern looks like for companies that raised $200 million+ rounds

- How debt financing is reshaping the capital stack

![]()

Sign up for our weekly newsletter.