Data Snapshot is a regular AFN feature in which we analyze agrifoodtech market investment data provided by our parent company, AgFunder.

Click here for more research from AgFunder and sign up to our newsletters to receive alerts about new research reports.

2020 saw European agrifoodtech secure its lowest amount of late-stage investment in seven years – but that might not be as disappointing as it first seems.

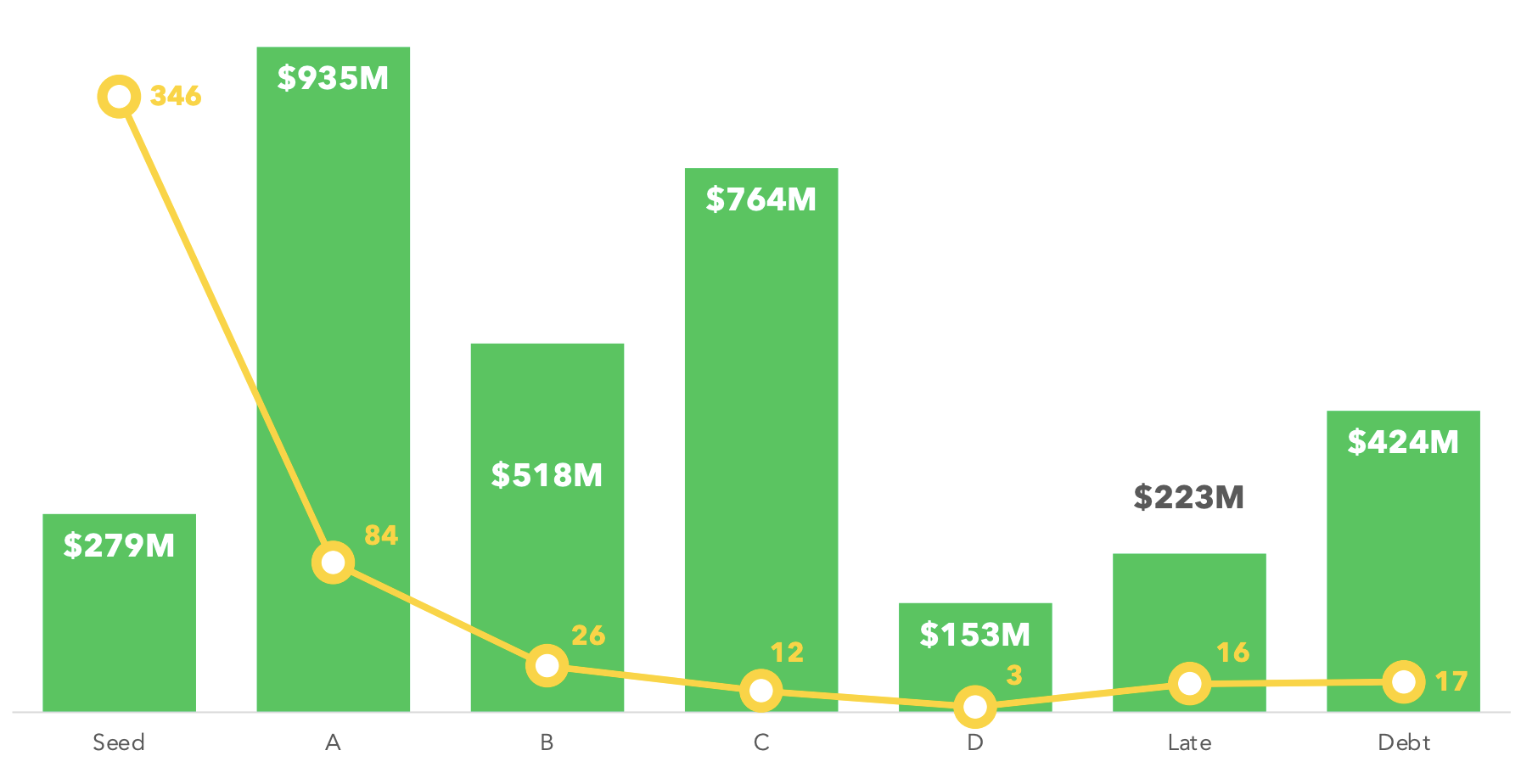

Deal volume ($) and deal count (#) by series, Europe 2020

European agrifoodtech ventures fundraising at Series D and later banked a total of $476 million in 2020, the most recent year for which AgFunder has published complete data.

That’s less than a third of what they pulled in at the same stage a year earlier, according to AgFunder’s ‘Europe 2021 Agrifoodtech Investment Report.’

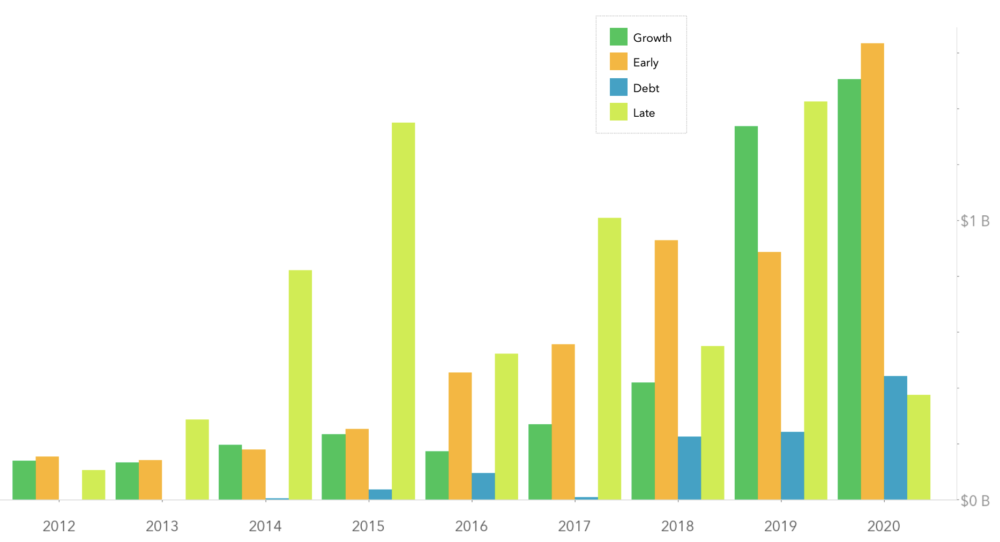

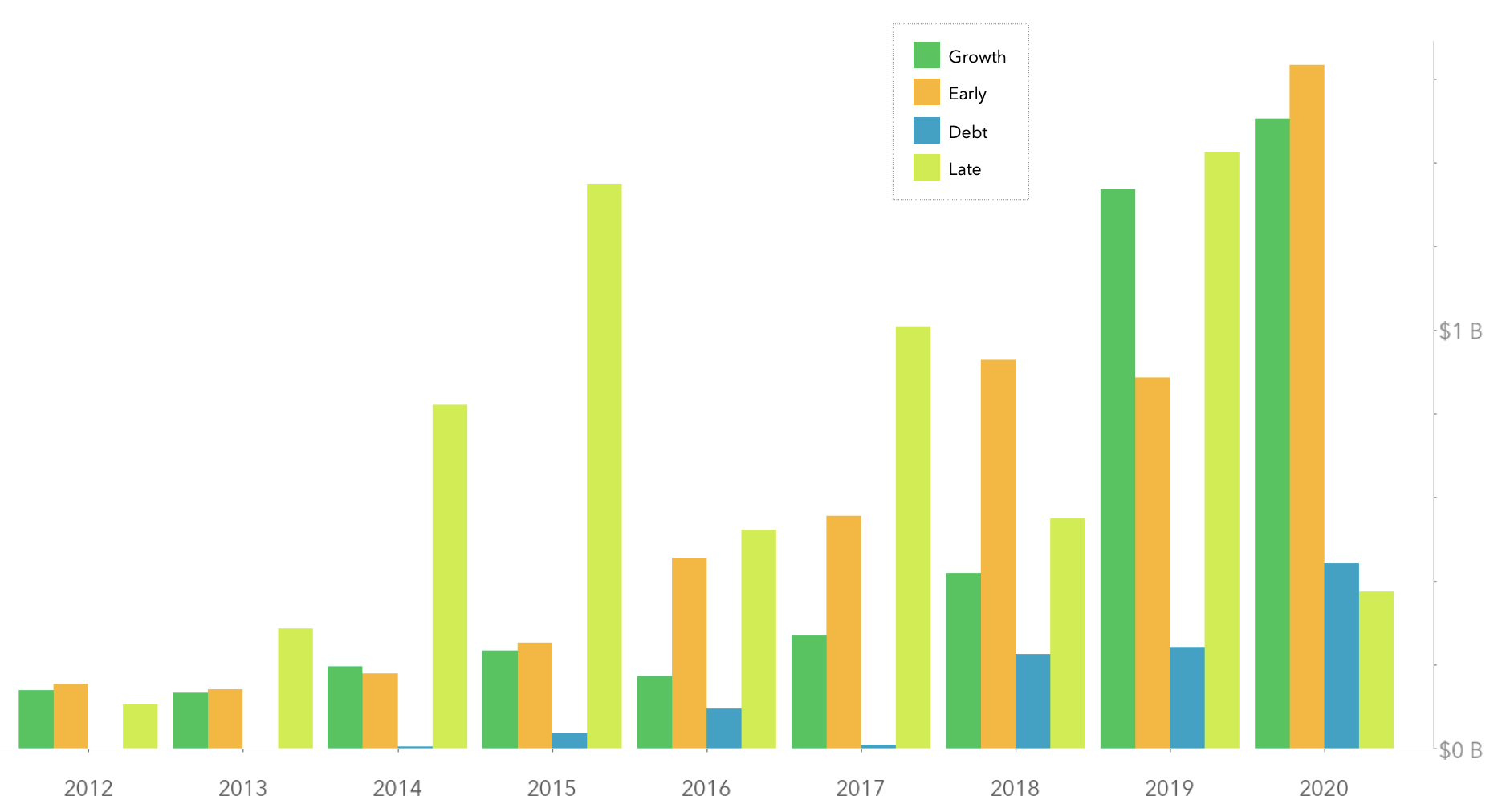

Projected deal volume ($) by stage, Europe 2012-2020

2020 was, of course, the year in which Covid-19 became a pandemic and caused economic chaos around the globe. However, this is unlikely to singularly explain the seemingly prodigious year-on-year drop in late-stage funding; after all, Europe actually recorded an increase in early-stage (seed and Series A) investment over the same period.

While late-stage investment was at its lowest ebb since 2013, early-stage deals comprised 86% of round counts in 2020 and saw more than twice the dollars invested in 2019. Series A funding by itself were nearly triple 2019 levels, in large part because of UK-based dark kitchen startup Karma Kitchen‘s $316 million raise.

So what happened? There are a few possible explanations:

- The size of many of 2020’s late-stage rounds were undisclosed, making total commitments appear lower. German food and beverage delivery company Flaschenpost, for example, raised an unknown amount for its May Series D round; it was acquired by Dr Oetker for $1.1 billion six months later.

- Companies that raised large late-stage rounds in 2019 did not raise again in 2020 – in some cases because they had an exit, or were expected to have one. Germany mealkit firm Marley Spoon IPO’d in April after raising $30 million the previous year, while the UK’s Deliveroo was preparing for its own IPO which took place in March 2021.

- Europe set about seeding its next generation of agrifoodtech startups in earnest. As mentioned above, early-stage investment on the continent substantially increased in 2020. Historical data appears to support this thesis, suggesting that 2020 may have been the start of a new investment cycle in European agrifoodtech. The last big drop in late-stage funding, in 2016, followed a late-stage spike in 2015. This pattern may have been repeated in 2020 – but we’ll have to wait for AgFunder’s full-year 2021 data — due out later this month — to confirm that.