Editor’s Note: Thomas van den Boezem is program manager at StartLife, a Netherlands-based incubator for agrifood tech startups, cofounded by world-leading agriculture university Wageningen University & Research. StartLife has a portfolio of 200 startups and startup programs across Europe. Here van den Boezem and AgFunderNews editor Louisa Burwood-Taylor write about the developing ecosystem of agrifood tech startups in Europe.

AgFunder CEO Rob Leclerc will be sharing more about Europe’s agrifood tech startup scene and more in an exclusive data presentation to attendees of the World Agri-Tech Innovation Summit in London next month.

Europe has always been a dominant force in the food and agriculture industry. The Netherlands, Germany, and France are all top exporters of agricultural products globally.

Europe is home to world-leading knowledge institutes in food and agriculture, such as Wageningen University & Research in the Netherlands, Rothamsted Research in the UK, as well as agrifood giants like Bayer and Nestlé.

Startup activity in food and agriculture innovation is also growing in Europe. In the last three years, investment activity has increased as many support resources for food and agtech startups have emerged, including accelerators, incubators like StartLife and government programs.

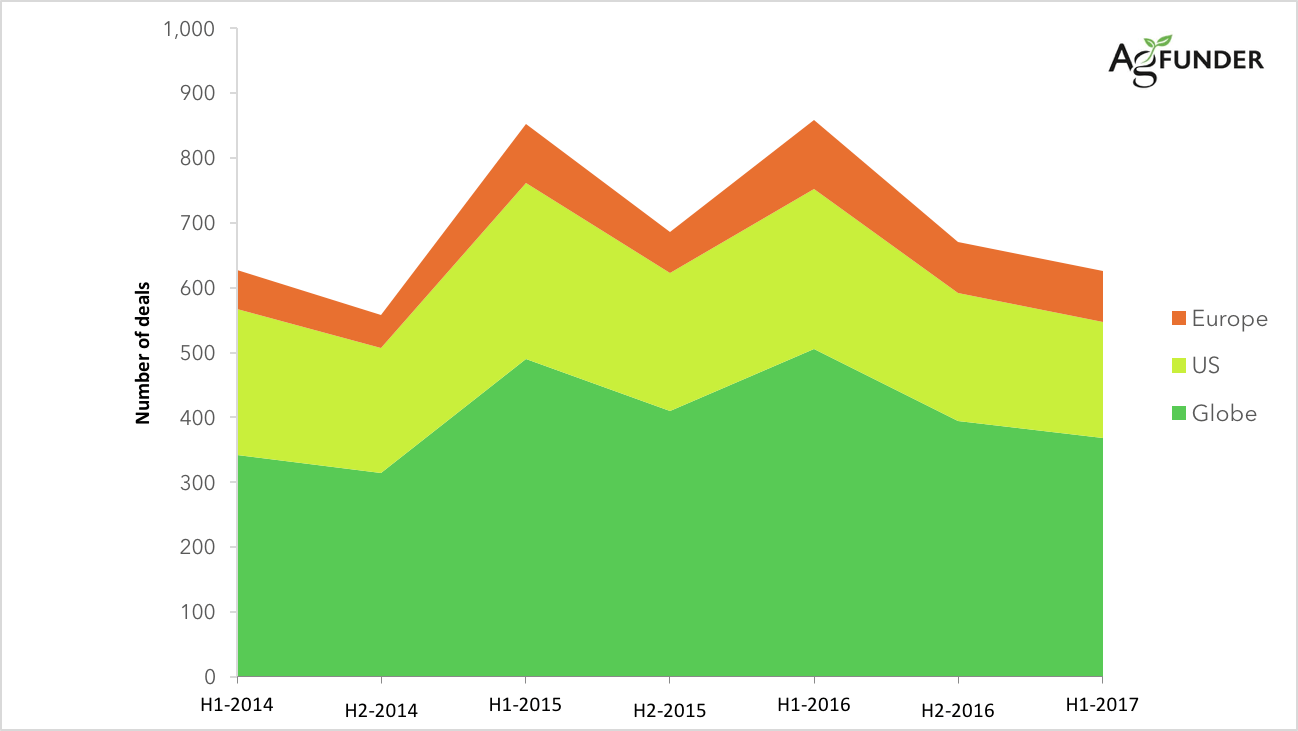

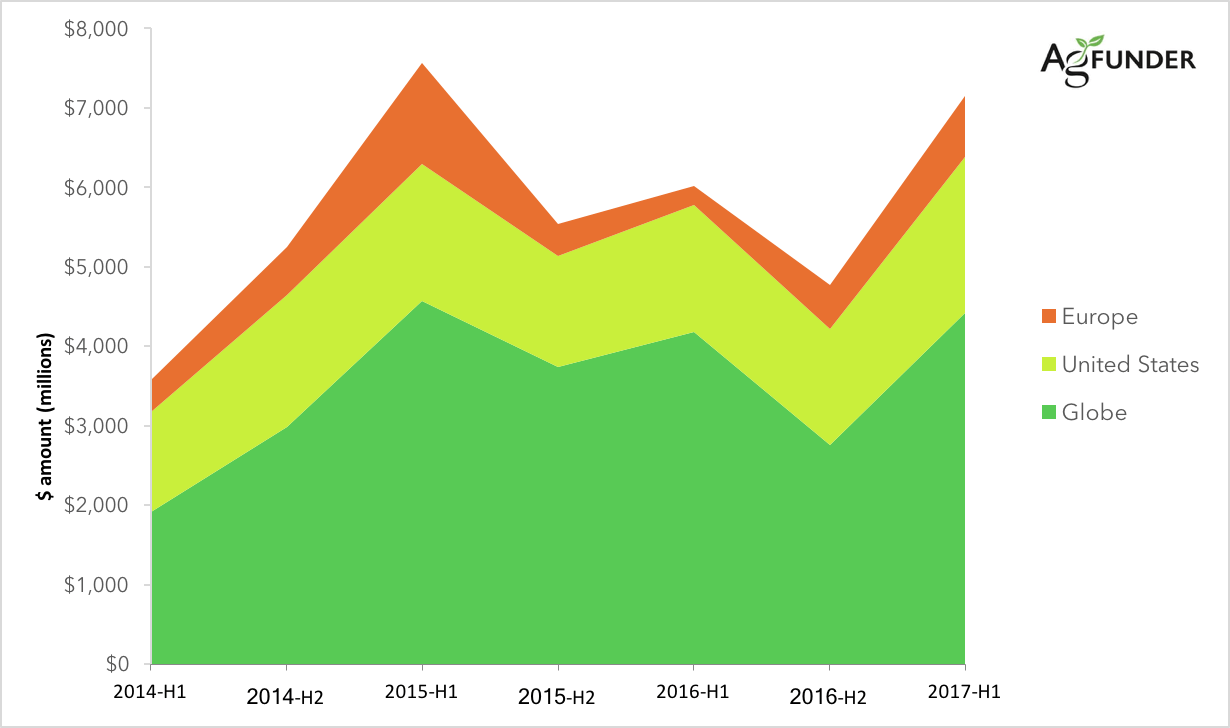

In the first half of 2017, investment in European agrifood tech startups represented 21% of global deals, up from 17% in the first half of 2014, when AgFunder records began. And agrifood tech startups in Europe raised $770 million during the period, the second highest ever level for dollar funding levels after the record-breaking first half of 2015 ($1.3bn).

The UK is the most active European country for agrifood tech investment, with 21 startups (out of 79) raising funding in H1. Next come France and Germany, where nine startups raised rounds in each country. Ireland and Italy both contributed eight deals during the period, with Holland contributing five and Sweden four. The remaining countries of Austria, Belgium, Denmark, Finland, Latvia, Norway, Russia, Slovakia, Spain, and Switzerland contributed three deals or less.

Where does Europe stand out?

Novel ingredients

Europe is home to some large and innovative ingredients companies such as Givaudan, the Swiss company that covers the flavorings and fragrances market, and Döhler, a global provider of technology-based ingredients headquartered in Germany. Both these companies have an excellent track record of collaborating with food and agtech startups.

This strength has translated into startup activity as there are several European agrifood tech startups now operating in the novel ingredients space, for both human and animal food.

NutriLeads, a StartLife portfolio company, develops proprietary nutritional ingredients with clinically proven health benefits. This year, it raised an undisclosed Series A round to further the development of its lead ingredient, which should support immune function to increase resistance against common infectious diseases.

Simris Alg is another promising ingredient startup, cultivating algae as a food ingredient for the B2B market, as well as developing consumer superfood and supplemental products. The company has raised over $11 million for the expansion of its algae farming operations in Sweden. Meanwhile, Seamore Food from the Netherlands has developed pasta and bacon alternatives from seaweed.

Europe is also home to a small number of insect farming groups aiming to provide protein replacement ingredients for animal feed, particularly fishmeal. Protix out of the Netherlands raised one of Europe’s largest funding rounds in H1, and the largest ever for an insect farming startup, with a $50 million Series B. Ynsect is farming mealworm to produce a fishmeal placement and raised $15.2 million in a Series B funding to scale up its robotics-enabled insect factory in France. Hexafly is another example of an insect farming startup targeting fishmeal, which raised just over $1 million after taking part in the IndieBio EU accelerator in Ireland where the startup is based.

Crop technology

Europe, and The Netherlands in particular, is a leading player in horticulture production. Earlier this month, National Geographic reported on some of Holland’s mind-boggling horticulture achievements. Its vast, high-tech, automated greenhouses have enabled hyper-efficient horticulture production, making the country the world’s second-largest agricultural exporter measured by value, while drastically lowering the amount of water and fertilizer needed.

As the indoor agriculture space itself is already relatively technologically advanced compared to other regions globally, startups are cropping up — (pun intended!) — to help service this sector on the farm as well as after the farm. Holland’s PeelPioneers, for example, is focused on repurposing waste, by turning citrus peels into oils, fibers and food ingredients.

On the crop production side, European startups are manufacturing biotech products to help increase crop yields in both horticulture as well as row cropping in a sustainable way. In H1, Belgian ag biotech startup Agrosavfe raised over $11.5 million in Series B funding for its biopesticide technology. And Wageningen-based startup Solynta has developed a breakthrough technology for the targeted breeding of potatoes.

On the digital and data side, Sencrop from France and the UK’s AgsenZe both raised seed funding rounds for farm management software and IoT tools to help farmers increase the efficiency of their operations.

Food Delivery

Startups creating technology platforms to help consumers buy food on-demand continues to grab investor attention globally, and Europe is no exception where the space is highly competitive. These startups range from Restaurant Marketplaces to eGrocery to Online Restaurants & Meal Kits, and in H1 globally they raised $2.7 billion. While the largest deal in this segment went to a Chinese company – ele.me raised $1 billion in Series H funding — German Restaurant Marketplace Delivery Hero raised the second largest deal at $421 million, shortly before listing on the Frankfurt stock exchange with a valuation of over $5 billion. The company is part of the family of Germany-based RocketSpace, known for cloning and scaling business models that proved to be successful in the US.

eGrocery startups tend to dominate the European food delivery landscape, as retailers are trying to escape or take advantage of the “Amazon effect.” eGrocery funding accounted for 13 of the 28 deals in the overall space in H1, with 10 at seed stage. Dutch eGrocer Picnic raised the second largest food delivery deal in Europe with a whopping $108.5 million Series B round to expand operations across the country. The company, which is less than two years old, has since been on a hiring spree for tech talent.

New resources for agrifood tech startups in Europe

In the last year and a half, the number of support resources available to agrifood tech startups in Europe has increased sharply, boosting the overall startup activity in the industry. These resources include:

- Investment funds

- Incubators and accelerators

- Corporate programs and other resources

- Government-sponsored programs

Incubators & accelerators

In France, ShakeUpFactory set up a Paris-based FoodTech incubator in Station F, claimed to be the world’s largest startup campus. According to Kevin Camphuis, co-founder of ShakeUpFactory, Paris is on track to become the global hotspot for foodtech startups. Camphuis cites the backing of French tech billionaire Xavier Niel for Station F and his investment activity in foodtech through Kima Ventures, a seed-stage investment fund, as important drivers of the ecosystem in Paris.

Italy too has its share of support resources. For example, Startupbootcamp FoodTech, a Rome-based accelerator program, is launching its second cohort in October this year. Milan also hosted former US President Barack Obama at the annual Seed & Chips food innovation conference earlier this year.

Corporate initiatives

There is a growing number of agrifood industry corporates providing resources for startups from venture capital funds to incubator initiatives, and this worldwide trend has caught on in Europe too.

In the last 18 months, corporates have quickly and widely picked up foodtech and agtech as a strategic priority. Large European companies like Nestlé, Rabobank, and Unilever all have platforms to stay on top of emerging startups and technologies in food and agriculture; for Rabobank, it’s the multi-location FoodBytes! business competition and accelerator program Terra.

Corporates are also getting involved in externally organized and managed initiatives like the European FoodNexus Startup Challenge, which aims to identify and accelerate leading food and agtech startups. Launched in seven European countries, including Denmark, Spain, and The Netherlands the challenge, coordinated by StartLife, will help startups grow by connecting them to corporate partners, including Unilever, Nutreco and FrieslandCampina, a dairy giant.

Government programs

Government bodies play an active role too. Initiatives on all levels of government (European, national and regional) aim to foster startups in all phases, from applied research to scaling up internationally. The European Commission has its Horizon2020 program, an $80 billion fund to stimulate early-stage research and innovation across sectors and bring new technologies to market across Europe. The program requires the public sector and the industry, including startups, to work together in delivering innovation. Solynta, the aforementioned potato-tech company, has been a recipient of Horizon2020 funding. National initiatives, such as the Dutch Startupdelta help to position Europe as a single market for startups and scaleups, by removing barriers to international expansion and linking Europe to the rest of the world.

Dedicated agrifood tech funds

In December 2016 The Netherlands witnessed the launch of a new seed fund, Future Food Fund, dedicated to early-stage food and agtech startups and backed by the Dutch government. Other European agrifood tech funds include Anterra Capital, CapAgro, and Finistere Ventures, which recently opened a new office in Ireland. US accelerator The Yield Lab also has a presence in Ireland. Aqua-Spark in the Netherlands is focused specifically on seafood and aquaculture technology startups.

But perhaps there’s still not enough going on in Europe as Anterra recently opened an office in Boston, US to ‘export’ European technologies and startup teams to the US, likely to benefit from larger markets and, perhaps, better exit opportunities.

Not yet top of class

While overall investment in agrifood tech startups in Europe is on the rise, it’s slow going. In the first half of 2017, startups raised $770 million across 79 deals, accounting for 17.4% of dollar funding totals globally and 21.4% of deal activity. That compares to H1-2016 when European dollar funding accounted for 6% of global funding ($250m) and 20.8% of deal activity (105 deals).

AgriFood Tech Deal Activity 2014-(H1)2017

AgriFood Tech Funding Levels 2014-(H1)2017

The majority of the activity is at seed stage — 53 out of 79 deals — highlighting the relative immaturity of the space in the region. Further, agrifood tech startups in Europe are raising smaller deals than their global counterparts; the median deal size in the region in H1 was $1.2 million compared to a global median of $3.1 million.

Europe has yet to see any significant agrifood tech exits too, although that could be a function of generally muted exit activity for the sector, even in the US.

Remaining barriers

The challenge for agrifood tech startups in Europe can be summarized as follows:

- Europe is not (yet) a single market

- Available funds and risk-taking behavior in Europe are limiting factors

- The startup ecosystem not as well defined as in the US

- The community of serial entrepreneurs entering the sector has been modest.

While many initiatives promote the idea of Europe as one united market, it remains a continent with many borders, cultures, and market characteristics. In some cases, government regulation on food safety and certification varies too. The dispersed layout means that Europe is not able to compete with countries like the US and Brazil on the sheer scale of production. The US simply has the competitive edge when it comes to square miles of arable land and size of consumer base within one country. Startups with technologies targeting large-scale farming operations will always find a better market in the US.

Another important factor is the availability of funds, although this is a global phenomenon. AgriFood Tech investment still represents just 7% of global VC funding, compared to data from the latest VenturePulse report. This is not representative of its 17%+ contribution to global GDP, highlighting the funding gap for the sector globally.

European investors are also typically more risk-averse than their American counterparts, according to many entrepreneurs. The entrepreneurial experience of the US is also greater than in Europe where there are fewer serial entrepreneurs like Bill Gates making bets in agrifood tech. That mentality needs to rub off in Europe.

The startup ecosystem is not as well defined outside of the US, where US startups follow a well-trodden path from research or idea to commercialization with the support of well-defined early stage resources such as government grants, accelerator programs, and incubators. And they largely conform to raising funding in seed, Series A, B, C rounds and so on. This path does not seem as well trodden in Europe across venture capital industries.

Europe has the expertise, research, and capital to make agrifood tech a serious contender for the region’s venture capital dollars. Trends in agrifood investments in Europe mimic those in the US as the data show and given the potential described above, agrifood tech in Europe could be headed to scale it deserves. However, the next few years will be critical. Much of today’s investment activity is tied up in seed stage deals. The region needs to focus on making resources and opportunities available to entrepreneurs in order to capitalize on these early-stage bets and help them successfully mature.