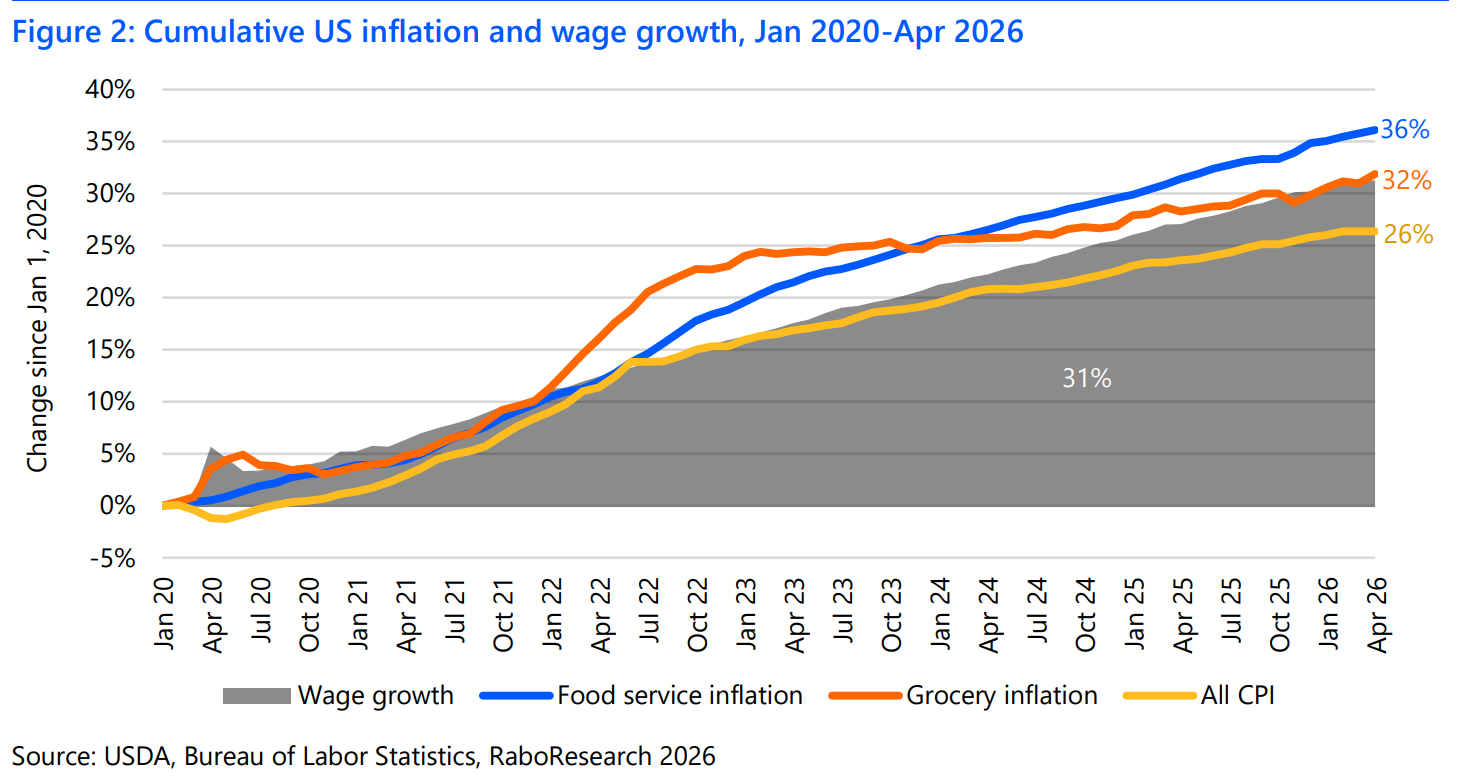

Markets are “underestimating the duration and stickiness of supply-side disruptions” from war in the Persian Gulf, warns Rabobank in a new report, which predicts mid-single-digit food inflation over the next 12-18 months in the US from disrupted oil, diesel, LNG, and fertilizer markets.

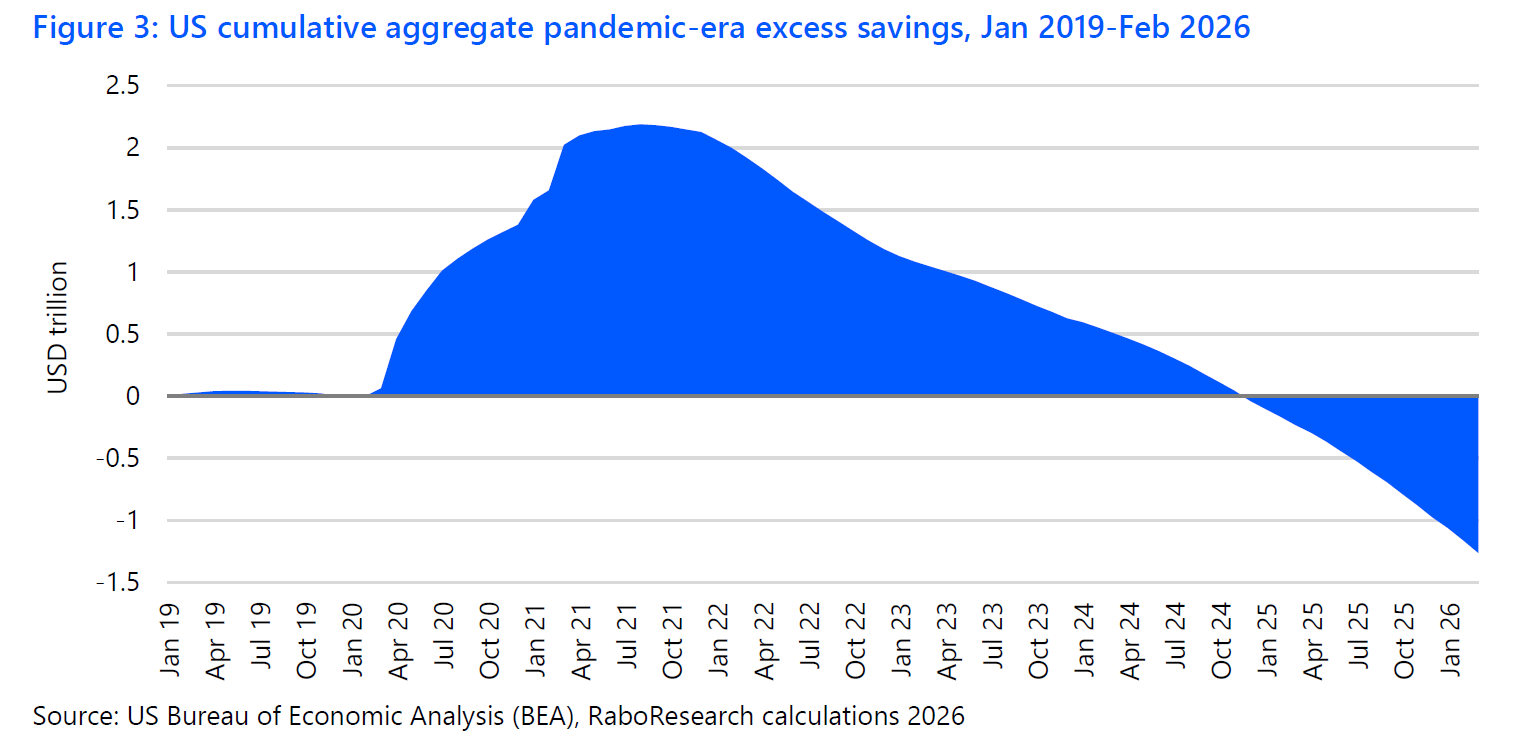

In 2021 and 2022, consumers were more able to absorb price shocks from the Covid-19 pandemic ad Ukraine war, notes Rabobank. “Today, that cushion is largely gone. We expect US food inflation in 2026 and 2027 to be structurally different from the 2021 to 2022 cycle.”

“Our outlook calls for food inflation to reach 4-6% by December 2026, year-over-year, and to continue at 3-5% through 2027.”

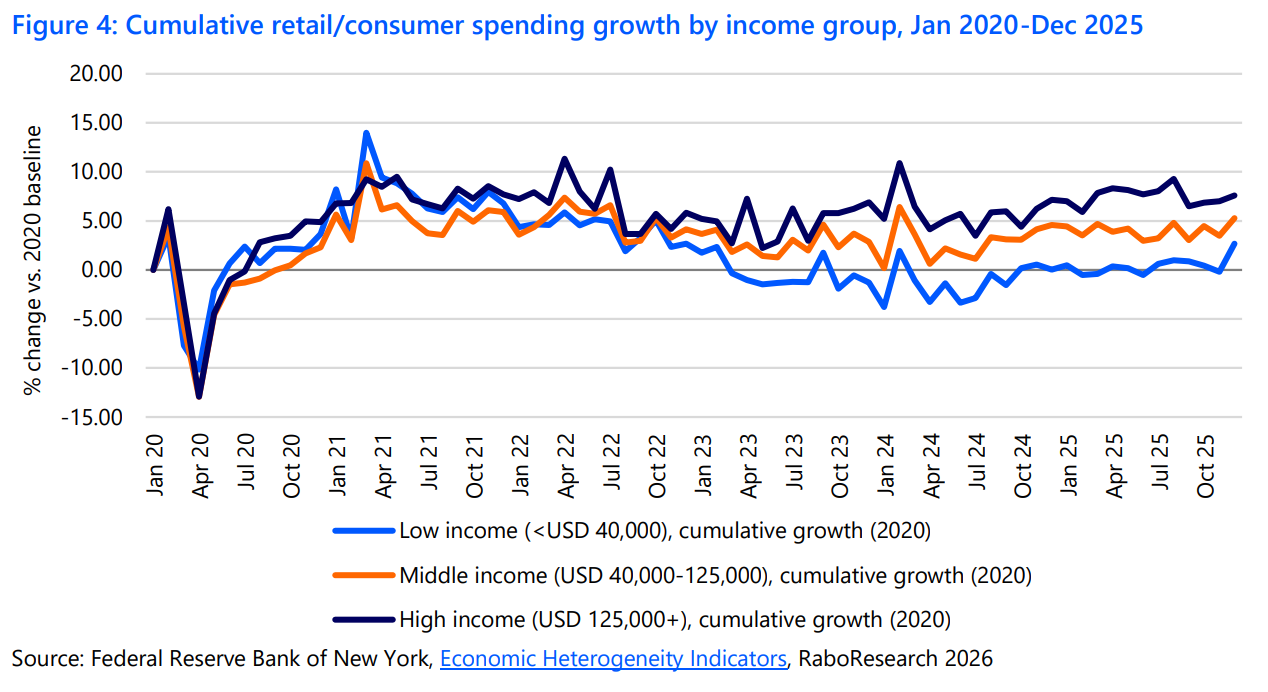

In a “k-shaped” economy, we can expect to see more “trading down, mix shifts, smaller basket sizes, and greater promotion sensitivity” for lower- and middle-income shoppers, while higher‑income consumers often maintain spending.

This is likely to create a “barbell” dynamic, says Rabobank, whereby value segments grow, some premium segments hold where differentiation is clear, but “mid-tier brands face the toughest combination of rising costs and higher elasticity.”

To add to the pressure on low- and middle-income shoppers, rising energy prices—which are raising costs for the food industry—are also directly compressing household budgets via higher heating cooling bills and higher prices at the pump, notes Rabobank.

“This often shows up as fewer trips, stricter adherence to shopping lists, more aggressive deal-seeking, trading down within proteins, and substitution away from convenience formats when price gaps widen.”

The barbell dynamic and the squeezed middle

In foodservice, cash-strapped consumers typically trade down and trim orders rather than stop dining out altogether, often by skipping add-ons such as beverages, desserts, and appetizers, says Rabobank.

Rather than leading to a collapse in spending, as with food retail spending, consumers tend to both:

👉 Trade down: migrate toward cheaper, highly trusted value options.

👉 Trade up (selectively): save discretionary dollars for fewer, premium experiences.

“The middle—where offerings aren’t the cheapest or the most differentiated—gets squeezed first, and the next wave of cost inflation is likely to widen that gap,” predicts Rabobank.

GLP-1s, dietary guidelines, SNAP reductions…

To compound the challenges for the food industry, several structural forces are also at play that could explain why this inflation episode should be “less demand-supported than the last one,” says Rabobank:

👉 GLP‑1 adoption is already reshaping consumption, with pressure in some center‑aisle categories.

👉 Evolving dietary guidance: performance is now more tied to health positioning and protein exposure.

👉 Slowing population growth is reducing baseline volume tailwinds.

👉 SNAP reductions are constraining purchasing power for the most price‑sensitive households, accelerating trading down and value substitution.

A false sense of insulation?

While food inflation numbers are creeping up again after dropping in the past couple of years, consumers are currently somewhat shielded from the Iran conflict’s impact on the agrifood supply chain as many large food companies rely on energy and freight hedges and long-term supply contracts to manage cost volatility, notes Rabobank.

This, it claims, has created a “false sense of insulation”. But as the hedges roll off and contracts reset, “underlying cost pressures tend to emerge more visibly,” warns the bank.

“RaboResearch expects energy to remain elevated for longer, creating a delayed but persistent inflationary effect that is likely to flow through the system into 2027.”

Meat and dairy

While the US is not facing a grain or oilseed shortage, higher fertilizer and fuel costs are raising feed and operating costs that will feed into the animal protein markets says Rabobank, with beef the most exposed because US cattle supplies are already tight.

Dairy should remain well supplied, but feed and energy costs could squeeze margins as hedges and contracts expire, says the bank.

Trucking and ocean freight

After a prolonged market downturn in the trucking market in the US, capacity is tightening and spot rates have been improving, setting up trucking costs to rise faster than inflation in 2026, predicts Rabobank.

“Under current energy assumptions, an approximately 10% average increase in trucking costs, including fuel, would translate to roughly a half‑point lift in food inflation.”

However, structural oversupply in the ocean freight market means that this segment is less likely to experience higher prices, it says.

Packaging

Food and beverage packaging is on relatively strong footing in the US, notes Rabobank. However, as packaging costs are closely tied to the petroleum value chain through energy inputs including fuel, power, and process heat, packaging will move “from a background cost into a more direct contributor to food inflation” over time.

Polyolefin plastics are directly linked to crude- and natural-gas-based feedstocks, while aluminum, glass, and fiber-based packaging are all energy-intensive to produce. Higher energy and fuel costs in turn also raise freight and logistics expenses.