What do you get when capital abundance, regulatory innovation, and high environmental stakes converge?

While venture capital funding is struggling to recover in many global regions, the Middle East and North Africa (MENA) region’s VC industry posted record highs for 2025.

A closer look at the region’s technology and investment trends highlights the rapid development of a global innovation powerhouse across technology categories, especially in AI, according to AgFunder’s intelligence engine Gaia. [Disclosure: AgFunderNews’ parent company is AgFunder.]

The region remains a net importer of food and extremely vulnerable to climate change events like extreme heat, rising sea levels, and water scarcity. (MENA is home to 6.3% of the global population but holds just 1.4% of global freshwater, for example.)

These factors necessitate innovation that could later serve as a blueprint for other regions facing climate challenges.

Meanwhile, geopolitical events, including Covid-19 and the Ukraine War, have elevated food security to a national priority equivalent to energy security, with explicit goals to increase output in nations’ 10-, 20-, and 30-year vision plans, including:

- Saudi Vision 2030 has an explicit target to double agricultural output by 2030.

- The United Arab Emirates (UAE) aims to rank among the top countries in the Global Food Security Index by 2051 through its National Food Security Strategy 2051.

- Egypt’s Sustainable Agricultural Development Strategy 2030 aims, among many things, to double the agricultural productivity of smallholder producers and increase investment in rural infrastructure and technology development.

- Morocco has mobilized and planned investments totaling tens of billions of dollars to transform its agricultural sector from 2020 to 2030, and it continues to plan additional investments.

Tech and infrastructure signals in MENA

Sovereign wealth funds are a foundational component of MENA’s financial landscape. They operate on a different timeframe than traditional venture capital—10 to 20 years versus 5 to 7—and focus on strategic value over purely financial returns. This enables decades-long R&D cycles and infrastructure-scale investments in technologies that inherently take longer to develop. Think quantum computing, clean power, and vertical farming infrastructure.

Since 2023, sovereign funds in the region have pumped hundreds of billions of this “patient” capital into AI and tech, with a focus on domestic deployment.

The UAE has made particular strides in AI infrastructure.

- It is already the second-largest global player for AI infrastructure, with over 188,000 chips and 6.4 gigawatts of power capacity.

- Last year, it announced an AI campus to house Stargate UAE alongside OpenAI.

- Abu Dhabi plans to become the world’s first “fully AI-native government” by 2027.

Saudi Arabia’s sovereign wealth fund PIF is projected to invest a whopping $2 trillion by 2030, unmatched in the region, according to Gaia. Other investments include:

- $40 billion earmarked for an AI fund

- $100 billion for advanced manufacturing via the Alat initiative

- More than $500 billion into the NEOM smart cities project, including The Line urban development project.

- Both projects address the region’s climate vulnerabilities and ongoing need for resources. NEOM and The Line include initiatives around water management and clean power to meet the anticipated 50% surge in demand.

Elsewhere, Qatar has a $1 billion budget for quantum computing R&D in its national strategy and the region’s first quantum lab. Egypt holds an active startup ecosystem, a large domestic market with its 120-million-strong population, and a pathway for startups to access the Gulf Cooperation Council (GCC) region, which includes Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the UAE.

Regulatory innovation as a competitive advantage

Several of the region’s nations have demonstrated a faster, more comprehensive regulatory pathway for new technologies than other parts of the world. These developments could position MENA as a major global competitor in areas like novel foods and nutrition. Examples include:

- Abu Dhabi is developing a regulatory framework for novel foods that reduces the registration period to just six to nine months versus 18 to 36 months in the US and EU. It will also consolidate registration for new food products, halal certification, and production/import permits, thus accelerating market entry.

- It has also updated its halal certification process to align with global standards, strengthening export competitiveness in the Muslim consumer market, estimated at 1.8 billion people.

- Qatar is the second country in the world to approve the sale of cultivated meat following its investment and manufacturing plans into Eat Just’s GOOD Meat, where it led the company’s $200 million round.

- The UAE has several regulatory sandboxes that allow for rapid development and “an agile regulatory environment” for new technologies such as AI.

- In line with global health trends, Saudi Arabia introduced new regulations around food transparency, including front-of-pack labeling and calorie disclosures on menus.

- The region’s gene-editing landscape is becoming increasingly competitive by adopting flexible, product-based frameworks that align more closely with the permissive US model than the traditionally restrictive EU standards, fostering a faster path to commercialization for non-transgenic innovations.

By the numbers:

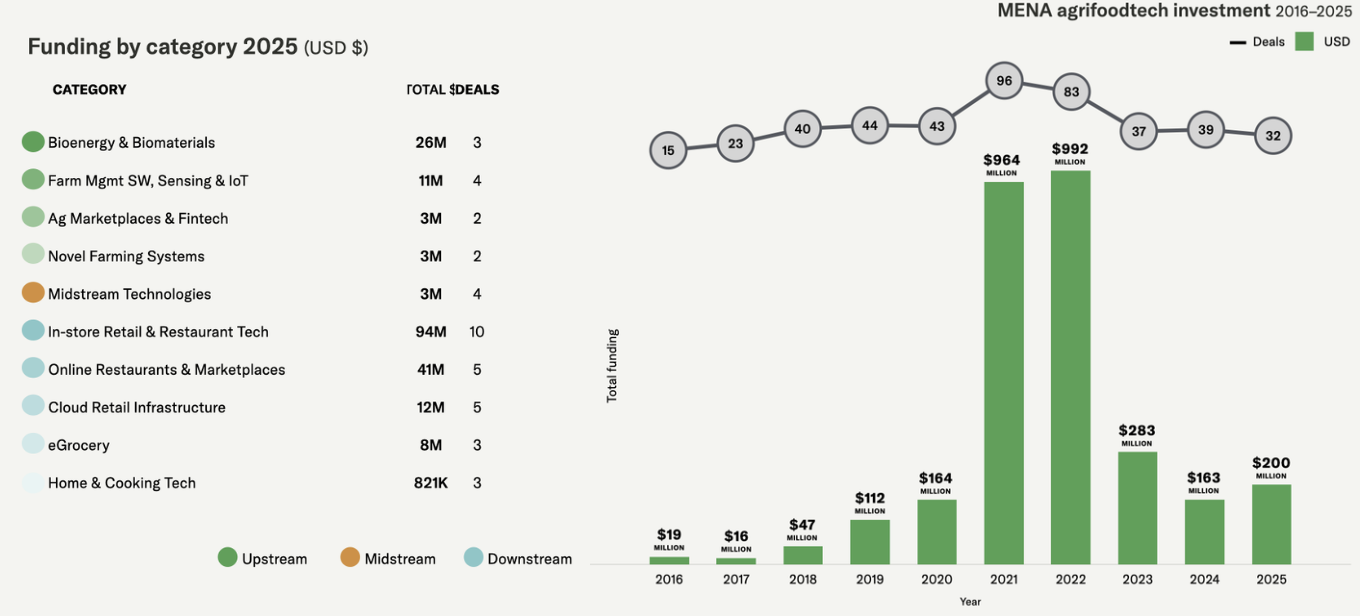

Of the $153.73 billion in total venture capital investment in MENA between 2015 and 2025, just over 5% went to agrifoodtech at nearly $3 billion. This share of GDP is on par with global levels, though lower than the industry’s 13% contribution to regional GDP.

The following companies offer a snapshot of leading regional agrifoodtech companies to-date by funds raised and strongest categories:

- Kitopi: raised $800+ million (largest exit candidate, cloud kitchens)

- Pure Harvest: $330 million (vertical farming infrastructure)

- Acquired Red Sea Farms in 2023 for its saltwater agriculture innovation

- Nana: $210 million (eGrocery regional leader)

- Foodics: $200 million (restaurant SaaS)

Agrifoodtech startups raised 22% more in funding in 2025, albeit over fewer deals than in previous years. Yet the split by categories tells us little of the region’s potential as outlined above. In 2026, the question is whether the above developments and goals will be reflected in MENA’s VC funding totals.