Indoor farming saw some big first-round raises last year. But the successes of AeroFarms, Bowery Farming, and Plenty in attracting venture capital is not necessarily reflective of the fundraising environment for the sector overall.

Twenty-five percent of indoor farmers say that access to capital is their biggest growth hurdle, according to a new report from indoor farming software company Agrilyst. Last year, by comparison, growers reported that the cost of operations was their biggest challenge.

Difficulty fundraising naturally has an impact on revenue growth and ultimately profitability. “With less conventional financial sources available to indoor farmers for both capital and operational expenses, as well as higher operational costs, it takes growers a long time to realize profits,” the report states. It takes indoor farms seven years on average to reach profitability.

Agrilyst’s analysis is based on a survey of 150 indoor farms in eight countries; it paints a picture of the financial health and hurdles of various kinds of indoor farming, which has become a catch-all term for a diverse array of crops, technologies, and operations.

On the whole, indoor farming is maturing, according to Agrilyst CEO Allison Kopf.

“I’m seeing the most maturation in the high-tech, smart greenhouse industry,” Kopf told AgFunderNews. “Growers in greenhouse operations who have been operating for a number of years are perfecting growing methods and reinvesting profits into new technologies, instead of inventing systems and methods from scratch.”

Compared to newer growing methods, like vertical farming, revenues, costs, and profit margins in greenhouse farming are stable.

“Other facility types (like vertical farming) showed large spreads across different size and age facilities,” Kopf said. The report notes that this is likely because vertical farming is new and just beginning to show signs of maturity.

Diversity in the Sector

Agrilyst’s survey features respondents from a range technologies and operation types. Nearly half of respondents represent hydroponic farms, while 24% run soil-based operations, 15% aquaponics, 6% aeroponics, and 6% use a mixture of growing technologies.

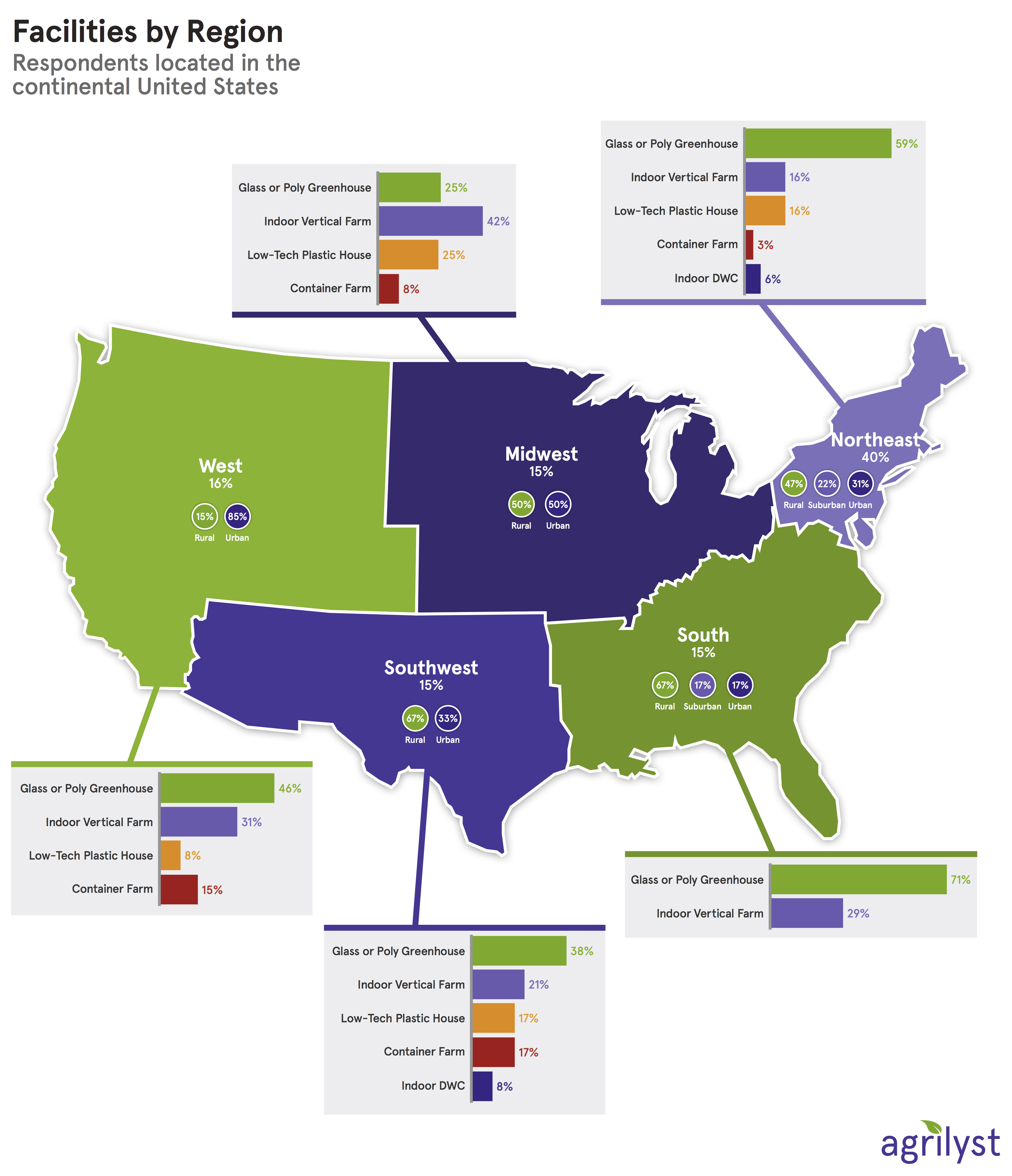

The most dominant type of facility was glass or poly greenhouses (47%) followed by indoor vertical farms (30%), which generally operate in converted industrial buildings. Plastics hoop houses, container farms, and other structure types made up the remaining 23% of respondents.

Geographically, a clear majority (81%) of respondents were US-based, with 12% from Canada, and 7% from other countries.

One myth that the survey seeks to debunk is that indoor farming is an urban phenomenon. Urban farms receive more media attention and seem to draw more venture funding than other types of indoor farming; however, most of Agrilyst’s survey respondents were based in rural locations (47%), while urban farms made up 43% of respondents and the rest were suburban.

“Indoor agriculture isn’t equivalent to urban farming. This is a big misconception,” the report states.

Farms make geographical decisions based on where they can maximize efficiency or near points of sale. A rural site may make the most sense for a tomato grower, for instance, because of lower costs of energy or where distribution centers are based.

It is also a common misconception that indoor farms can only grow tomatoes, greens, and cannabis. Though these are staple crops, the crop assortment among the 150 operations surveyed is highly varied. The main crops are leafy greens, microgreens, herbs, flowers, and tomatoes. Other varieties include: strawberries, herbs, cucumbers, peppers, mushrooms, onions, leeks, hops, figs, sweet corn, eggplant, fish, insects, carrots, and shrimp.

Profitability Depends on Crop and Farm Type, Not Tech

Crop variety, in fact, is an important factor for farm profitability—more so than the type of technology used. Flower-growing operations are the most likely to profitable, with 100% of flower growers reporting operations in the black, Agrilyst’s survey finds. Tomato and microgreen operations were the second and third most profitable crops, at 67% and 60% respectively.

Kopf noted that cannabis is most likely the winner in terms of crop profitability, but it was not included in the report because this year’s survey did not receive enough responses from cannabis growers.

Operations-wise, deep water culture operations are the most likely to be profitable, followed by glass or poly greenhouses with 75% and 67% of respondents reporting profitability, respectively. The third most profitable growing method in the survey is container farms (50%) followed by indoor vertical farms (27%) and low-tech plastic “hoop houses” (25%).

Technology type appears less correlated to profits. Most technology types range from 50-60% of farms reporting profitability with one exception: only 25% of farms that reported using a mix of growing technologies operate profitably.

Costs Rise As Farms Grow Up

In terms of challenges, access to capital is followed by what the report calls “building-related” challenges such as pests and maintaining optimal growing environments, followed by labor, and financial sustainability.

Indoor growers continue to focus on specialty crops to take advantage of high margins since operation expenses remain high, with labor at the top of the list.

In terms of inputs, costs are generally split evenly between seeds, nutrients and grow media, except for vertical farms, where grow media represents half of input costs. The report explains that even in profitable vertical farming operations, the cost per square foot is $37.10 while the cost of a hydroponic operation is $13.86. However, growing in stacked layers may mean that this difference isn’t as dramatic as it appears.

Finally, while labor is a major cost center for all types of indoor farming, vertical farms require the most employees per square foot.

“This makes automation technologies incredibly important as the industry matures,” concludes the report.

To find out more about the costs associated with each farm type and growing method, and the state of indoor farming generally, download the full report.