[Disclosure: AgFunderNews’ parent company is AgFunder.]

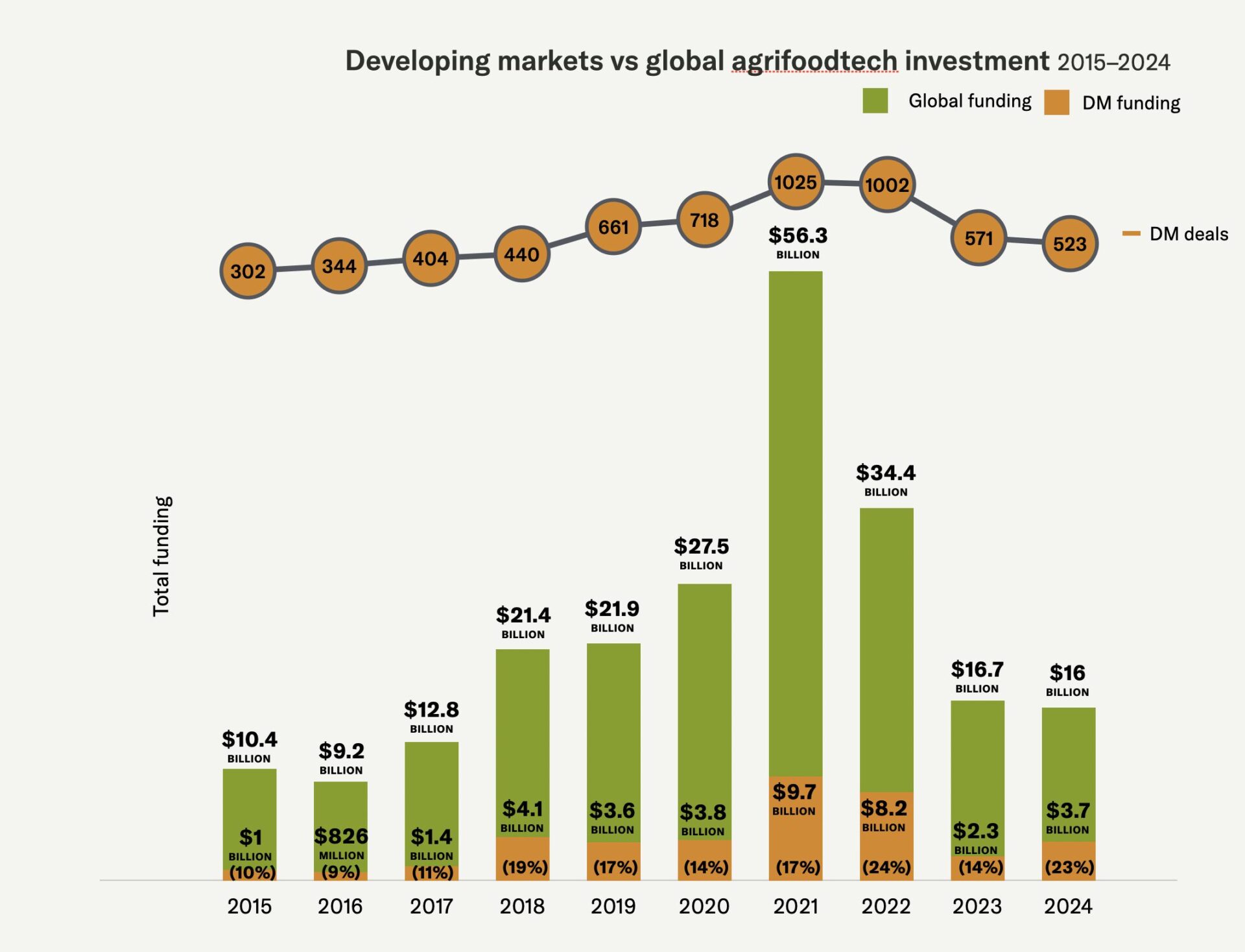

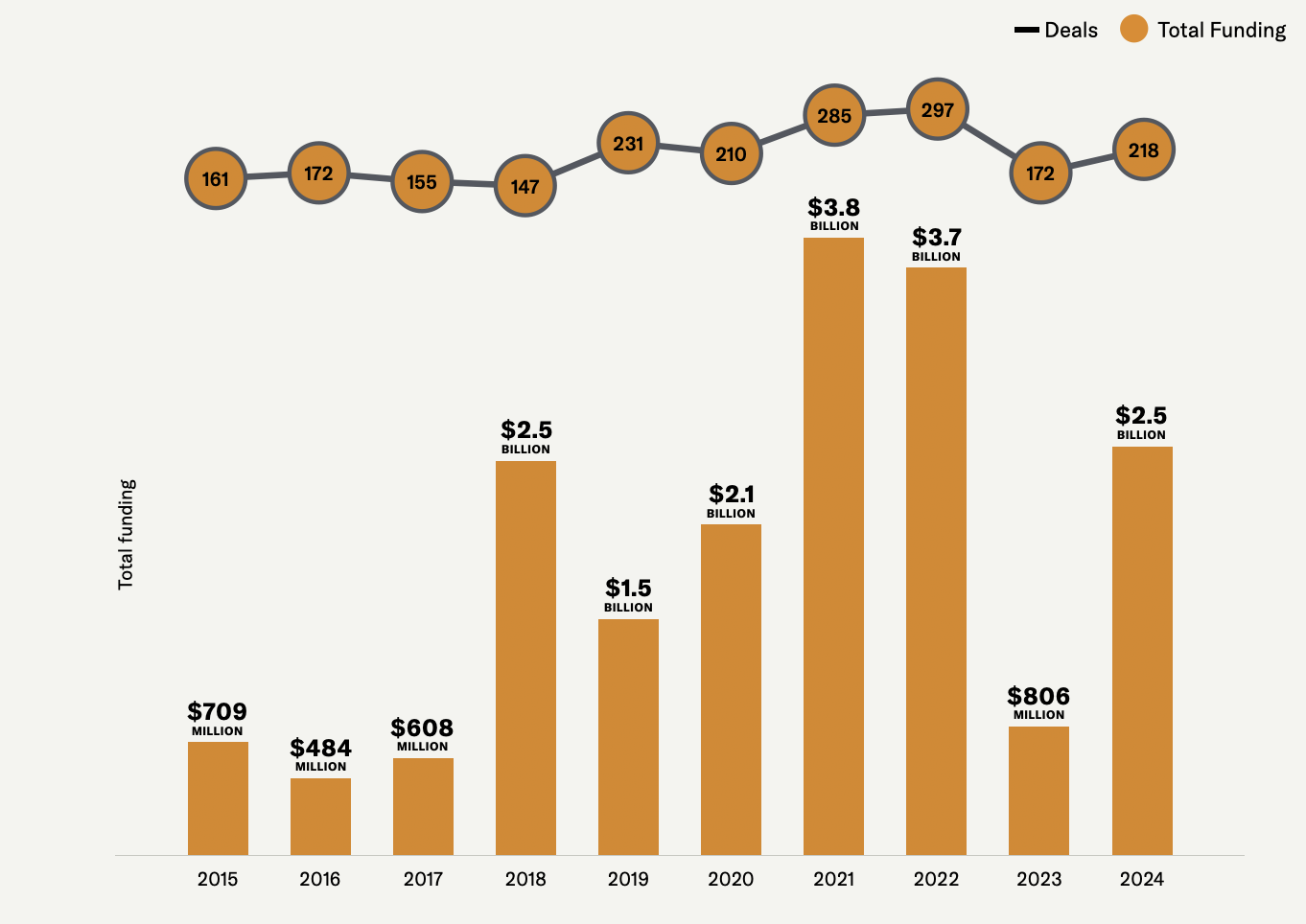

Agrifoodtech investment in developing markets reached $3.7 billion in 2024, surging a remarkable 63% year-over-year (YoY) and bucking the 4% decline observed in the agrifoodtech sector at the global level. Total funding in developing markets accounted for 23% of global agrifoodtech investment, according to AgFunder’s 2025 Developing Markets AgriFoodTech Investment Report.

The funding increase was achieved across 523 deals, showing a 8.4% YoY decline in deal activity, indicating the industry closed fewer and larger deals, according to the new report, which was released in partnership with Indian VC Omnivore, Dutch development bank FMO, and sugar reduction company Blue Tree Technologies.

Developing markets vs global agrifoodtech investment, 2015-2024

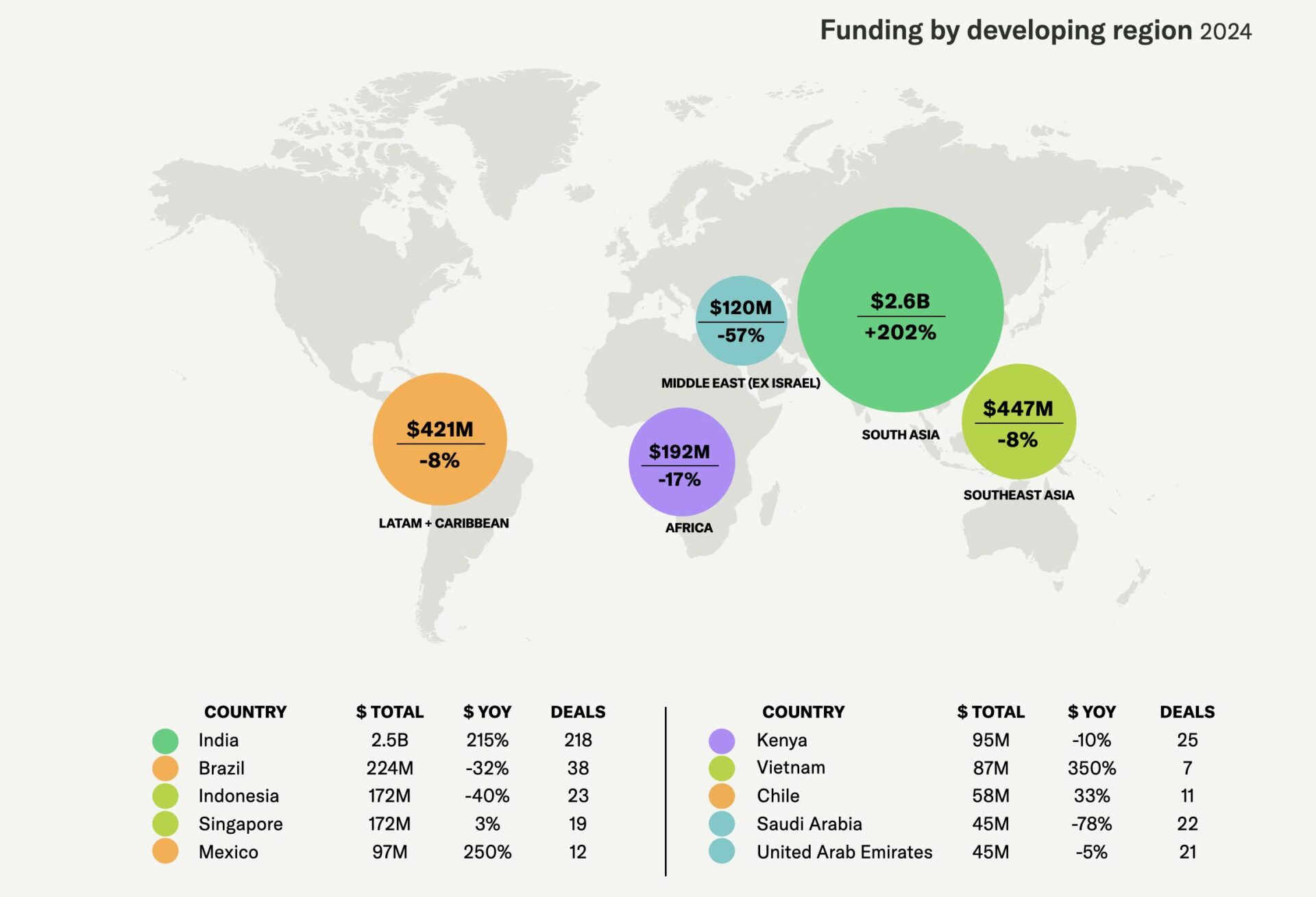

The primary driver of this growth was India’s e-Grocer Zepto, which secured nearly $1.4 billion across three funding rounds in 2024, comprising a third of the total investment in developing markets.

But even without the contribution of this outlier, several developing markets posted gains, starting with India, where total funding without Zepto reached almost $1.2 billion.

Agrifoodtech startups in Mexico, Vietnam, Chile, and Singapore also raised more funding in 2024 than in 2023.

Funding by developing region, 2024

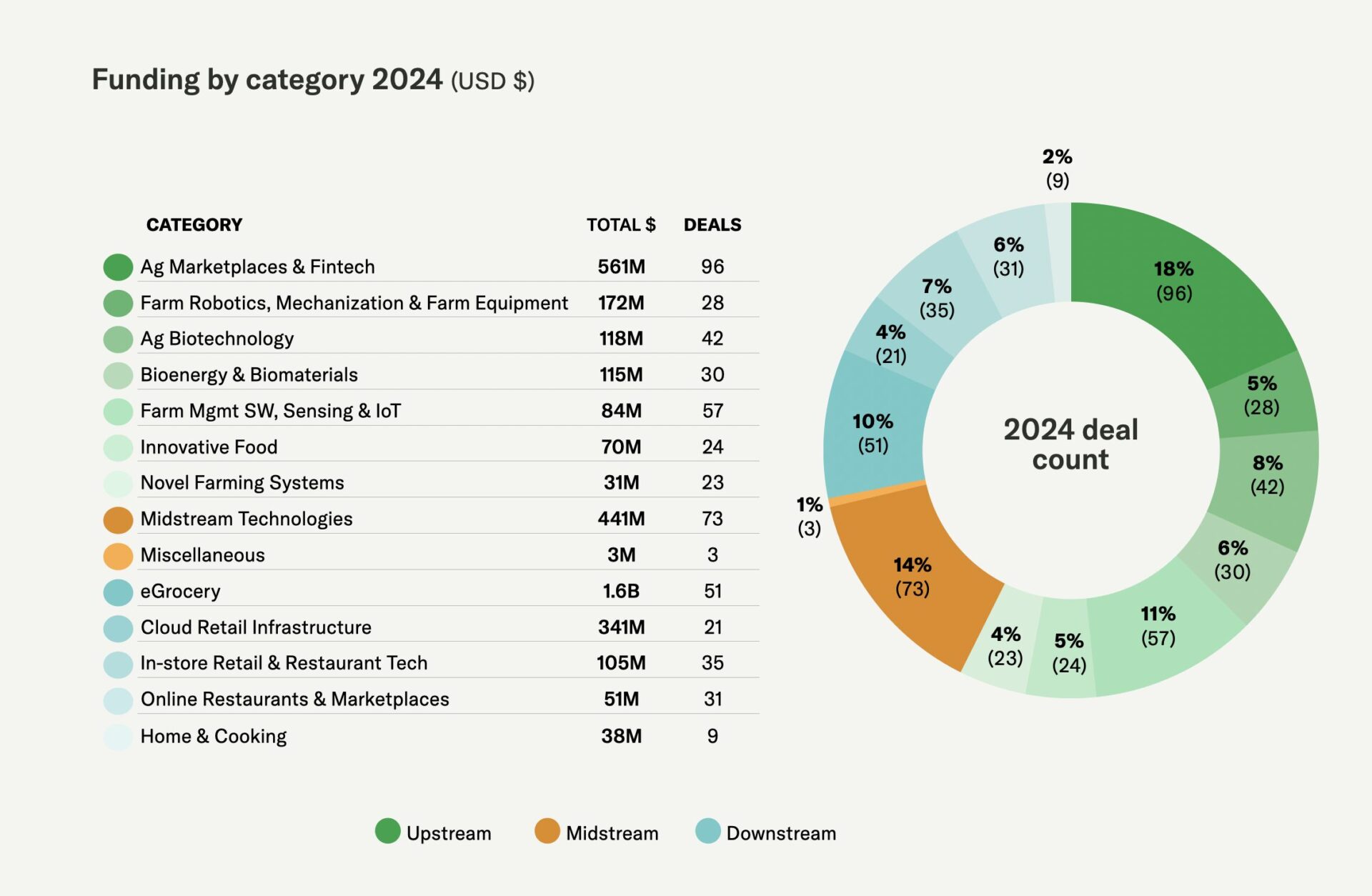

Ag Marketplaces drive upstream funding increase

Funding to upstream startups—those operating before or on the farm—increased 22% YoY to $1.2 billion, taking a 31% share of all developing markets’ funding. Vietnam’s integrated agritech platform Techcoop topped the upstream ranks thanks to four rounds jointly worth $75 million.

Second in the upstream supply chain was Indian distribution platform Sarvagram, raising $67 million in a Series D round. Brazilian ag fintech Agrolend followed with $53 million, while Singaporean ingredient trading platform Valency International raised $50 million.

Six of the 10 top-raising upstream companies, including all four listed above, belong to the same category, Ag Marketplaces and Fintech, which grew 71% YoY and was the best performer in the upstream supply chain.

With a total funding of $561 million across 96 deals, the category represented 49% of all upstream funding in developing markets in 2024.

Ag Marketplaces and Fintech was, in fact, the best-funded upstream category for all developing market regions apart from the Middle East. This is unsurprising given the fragmented nature of most developing nations’ agricultural industries and disaggregated smallholder farmer communities; the category is far less popular in more efficient developed countries, representing just 4% of total funding in 2024.

Funding by category, 2024

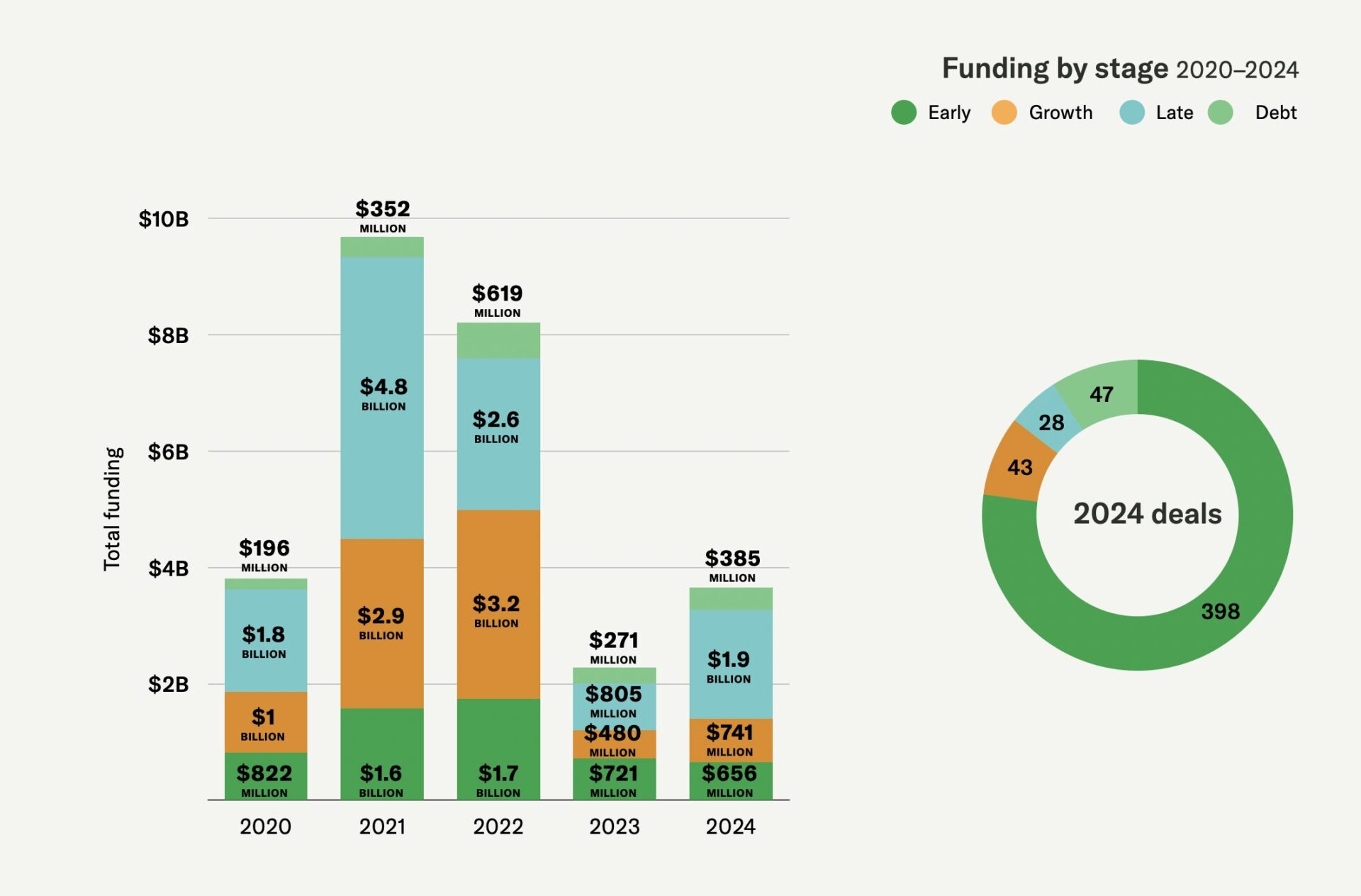

The overall decline in deal count points to larger, later-stage deals. Late-stage rounds raised 133% more capital in 2024 than in 2023, while growth-stage funding was up 54% and early stage (seed and Series A) was up just 1% YoY.

Funding by stage, 2020-2024

India returns to pre-Covid levels

India was the top-funded developing market and the second globally for agrifoodtech investment in 2024, posting spectacular growth of 215% in dollar funding and 27% in deal count.

India is one of the world’s most established agtech ecosystems. Its lead investor, Omnivore–also the sponsor of this report–has been investing in the space since 2010 and invested in 11 deals in 2024, making it by far the top agrifoodtech investor from India.

While eGrocer Zepto somewhat skewed the country’s total, startups there still raised 49% more YoY with Zepto excluded. Ag Marketplaces and Midstream Tech startups raised nearly $500 million alone.

India agrifoodtech investment, 2015-2024

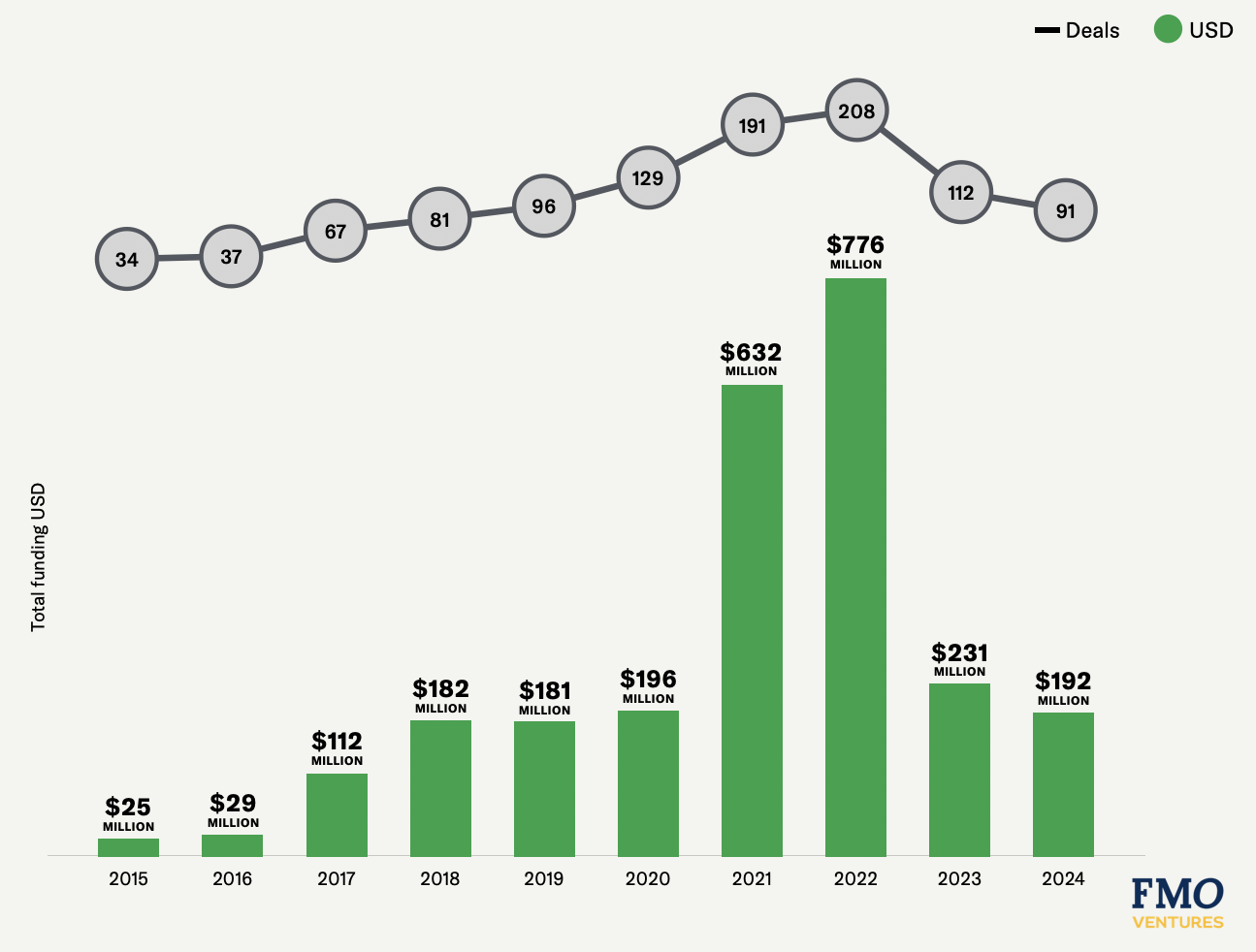

Kenya maintains Africa’s top spot

In 2024, Africa raised $192 million across 91 deals, representing 5% of agrifoodtech funding in developing markets.

Kenya defended its top spot in the region with total funding of $95 million, followed by Nigeria and Egypt with $26 million each.

Kenya was home to the two best-funded companies on the continent, solar-powered irrigation tech and financing startup SunCulture with a $28 million Series B round, and fintech to farmers platform Pula Advisors, which raised a $20 million Series B.

The third spot was secured by Egyptian e-Grocer OneOrder, which closed $16 million in Series A funding.

Africa agrifoodtech investment, 2015-2024

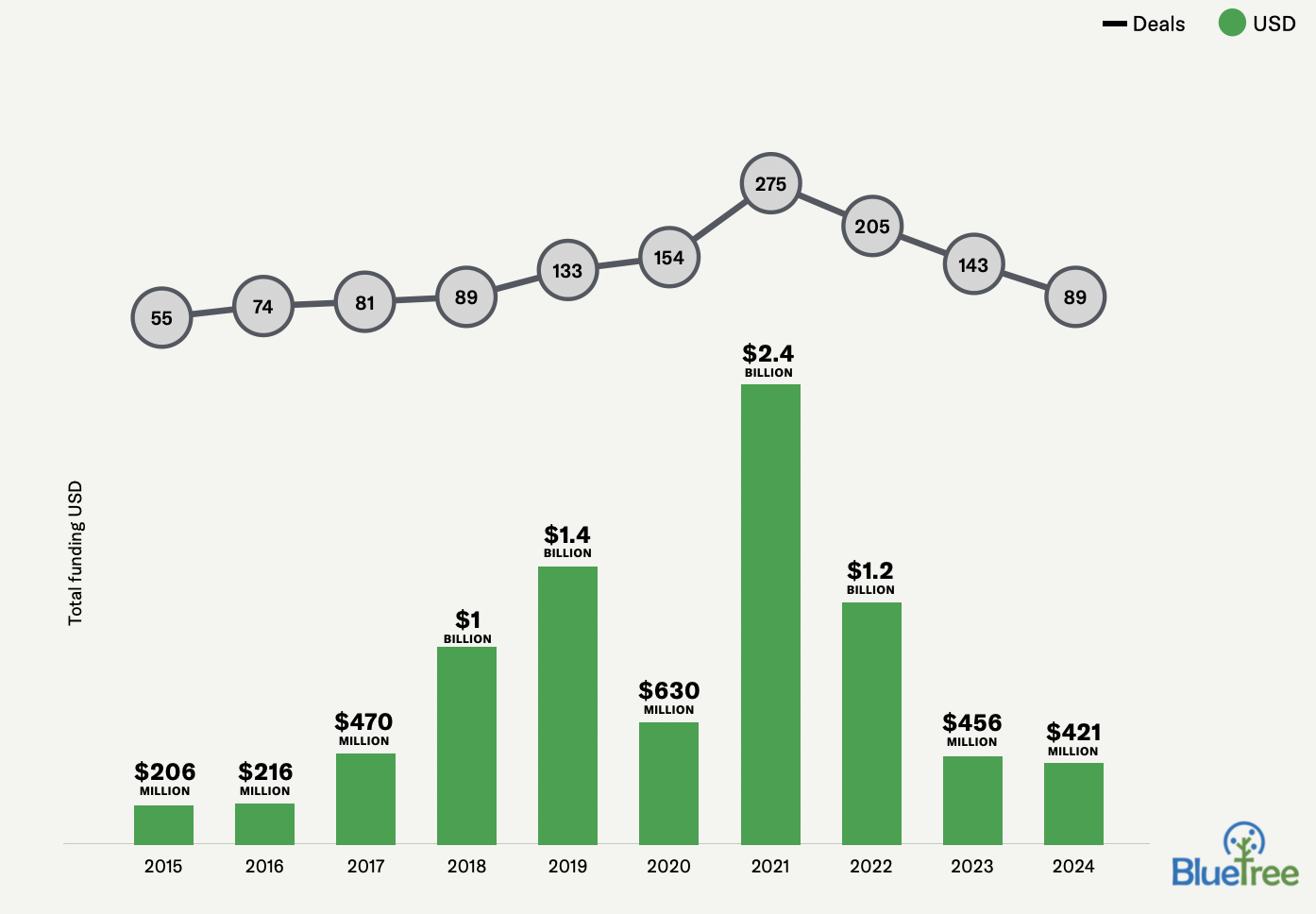

Big foodtech and upstream deals drive funding in Latam & Caribbean

Latin American and Caribbean agrifoodtech startups closed 89 deals worth $421 million in 2024, accounting for 11% of funding in developing markets. Brazil led the region, with $224 million, followed by Mexico with $97 million and Chile with $58 million.

Mexican eGrocery startup Jüsto was the region’s best-funded company in 2024, raising a combined $70 million in Series C and debt funding. [Disclosure: AgFunderNews’ parent company AgFunder is an investor in Jüsto.]

The largest single deal and the second spot for total funding in the region went to Brazilian In-store Retail & Restaurant Tech startup Cayena, which closed a Series B round worth $55 million.

But upstream deals accounted for over half of total funding with $264 million and a 9% YoY increase, with Ag Marketplaces and Farm Robotics leading the charge.

The LATAM & Caribbean section of our report was sponsored by sugar reduction innovator Blue Tree Technologies.

Latin America and Caribbean agrifoodtech investment, 2015-2024

Other key takeaways include:

- Investment increased in five of the top 10 countries: India $2.5 billion (+215%), Singapore $172m (+3%), Mexico $97m (+250%), Vietnam $87m (+350%), and Chile $58m (+33%).

- Other top funded countries were Brazil $224m, Indonesia $172m, Kenya $95m, Saudi Arabia and the United Arab Emirates both $45m each, Nigeria and Egypt both $26m each.

- Downstream investment grew 91% to $2.1bn, representing 57% of all developing markets funding.

- Funding to upstream categories increased 22% to $1.2bn, taking a 31% share.

- Midstream funding increased 94% to $444m, taking a 12% share.

- Cloud Retail Infrastructure posted the highest year-over-year growth, increasing 202% to $341 million in 2024.

- Funding to Novel Farming Systems and In-Store Retail and Restaurant Tech startups declined the most, both down 47% YoY to $31m and $105m, respectively.

DOWNLOAD THE REPORT IN FULL HERE.

Sign up to our newsletter for more analysis from this report in the coming weeks.

![]()

Sign up for our weekly newsletter.